Raw materials are the great overlooked in the global technological competition.

In 1992 the father of China’s economic revolution, Deng Xiaoping, said that ‘the Middle East has the oil, but China has the rare earths’. Rare earths, and critical raw materials in general, have been the great forgotten commodities in the geopolitical competition of recent years, which has largely focused on which country dominates certain technologies –artificial intelligence, semiconductors and so many others– and not so much on what means were necessary to achieve dominance.

China controls 36.7% of global rare earth reserves. Brazil and Vietnam, the next countries on the list, together stockpile as much as China does alone (18.3% each). They are followed by Russia, with 10% of the world’s total rare earths, and India, which supplies 5.8%. The remaining 10.9% is unevenly distributed.

Raw materials are the basic resources indispensable for producing key technologies of the green transition –such as wind turbines, solar panels and batteries for electric vehicles– and the digital transition. However, they have become a vector of dependency, geopolitical risk and a hugely important trade weapon. A raw material is critical when it is of high importance to a country’s economy, but also when it has a high risk associated with its supply.

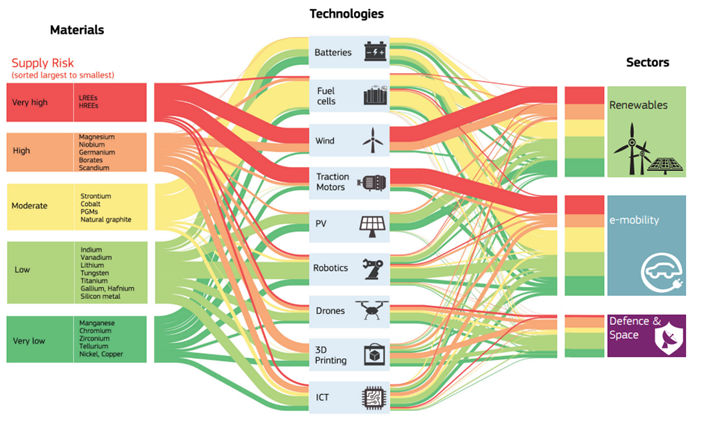

Figure 1. Semi-quantitative representation of raw material flows and their current supply risks in nine technologies and three selected sectors

A clear case in point is the crisis in semiconductor, smartphone and electric vehicle manufacturing. Ukraine and Russia are major producers of the gases and heavy metals used to manufacture these products. When Russia invaded Crimea in 2014, neon prices shot up by at least 600%, leading to market shocks. Since the war started in 2022, chip production has been largely affected by the reliance on Ukrainian factories. Ukraine produces more than 90% of the neon that the US needs for chipmaking.

Dependence on China

However, dependence is not only generated by who owns the largest reserves. It also depends on who dominates the mining, refining and processing stages of these raw materials. After being shut down for years, the only rare earth mine in the US, located in Mountain Pass, California, was taken over by new owners in 2017 and resumed production. However, the mined material it produces is still being shipped to China for processing. At the same time, in 2020 the US Department of Defense approved funding a joint venture between the Australian firm Lynas Corporation and the US firm Blue Line Corporation to build a processing plant in Texas. If carried out, the aim is for the rare earths that the Australian company collects in Malaysia to be brought to the US for processing instead of China, as has been the case until now. Japan has sought to participate in this joint project modality as well.

The goal of reducing China’s centrality in critical raw materials has been growing over the years for many countries.

Between 2008 and 2018, 42.3% of all rare earth exports in the world came from China. And the vast majority of these exports went to four of the world’s leading technological powers: Japan received 36% of the volume, the US imported 33.4%, the Netherlands 9.6% and Korea 5.4%. However, the attempt to reduce dependence has not been successful for the time being, except in the case of Japan. The Land of the Rising Sun has managed to reduce China’s rare earth imports from 91% in 2008 to 58% in 2018. The EU and Korea have managed to diversify some materials but are still almost entirely dependent on China for many of them.

The initiatives are not trivial. China has been able to make rare earths a ‘strategic resource’ and has used its exports as a trade weapon. In the mid-1980s, the Chinese government supported the nascent rare earth industry with export tax breaks. In 1990 China applied a protectionist approach by banning foreign firms from mining rare earths within China and restricting foreign participation in processing projects, except in consortiums with Chinese companies. In the late 1990s the government began applying ‘tiered quotas’ to discourage the export of raw materials used in high-value products and to incentivise the shipment of materials in downstream products.

This export quota policy was the most effective tool for China. In 2010 the government cut off all rare earth exports to Japan due to a maritime incident in the waters off the Senkaku/Diaoyu Islands. This explains Japan’s shift towards Australia to reduce China’s dependence. A few years later, in 2012, the EU, Japan and the US filed litigation against China at the WTO over the quota policy. The WTO ruled against China in 2014, which had to end the system a year later. However, since the late 1990s China had already developed an extensive ecosystem around commodities that had enriched the country.

The transatlantic relationship amid the geopolitics of critical raw materials

The European Commission has included critical raw materials on its agenda since 2008, when it launched a first initiative. The EU’s concern about this issue has been growing: the number of critical raw materials has increased from 14 in 2011, to 20 in 2014, to 27 in 2017 and to 30 in 2020. In 2017 the EU formed the Raw Materials Alliance to diversify the importation of raw materials and their better access within the internal market. The following years have been marked by the attempt to devise a strategy, promoted by the European Parliament, the European Commission and the Council of the EU.

It was on 14 March 2023 that the strategy was transformed into a legislative proposal, which presents both opportunities and challenges. First, it seeks greater coordination and coherence between member states to avoid market distortion and fragmentation. It also raises the possibility of using state aid –subsidies– to develop raw material projects within the EU. Secondly, it seeks to reduce technological centrality and external dependence: it aims to set a benchmark not to depend on a single third country for more than 70% of imports of all strategic raw materials by 2030.

To do so, international cooperation with other countries is needed. Just days before the legislative proposal, the White House and the EU announced a transatlantic agreement to deepen their cooperation in the diversification of critical minerals and raw material supply chains, and to collaborate in defining export control and foreign investment mechanisms. The objective is two-fold: on the one hand, to alleviate the uncertainty that the Inflation Reduction Act (IRA) was generating in EU companies; on the other, to bring visions closer together in the face of global dependence on raw materials.

In this respect, it is most likely that the EU seeks to bring visions closer together, albeit with two differences: in the same way as the Council for Trade and Technology, Ursula von der Leyen aims to de-risk, but not decouple from China. If in 2018 raw materials were critical for US national security and economic security, a year later Trump added that they were also critical for national defence. This three-pronged approach differs from the European one as well.

It will also be crucial to follow how Sweden can become a rare earths hub, as Europe’s recently discovered largest deposit, for the manufacture of turbines and electric vehicles, and which may influence transatlantic relations vis-à-vis the IRA.

On the other hand, EU action in commodity geopolitics must look beyond the transatlantic lens: the role of other producers, such as Chile, must be at the centre of the European policy agenda. In December 2022 the agreement that has secured non-discriminatory access to Chilean raw materials was updated: no exclusive trading rights will be granted to any specific company, as had been the case, nor will the current policy of dual pricing that benefits locally established companies be continued. The Netherlands has been one of the few member states to highlight the importance of Latin America and Africa in this matter.

In conclusion, critical raw materials are a major geopolitical vector for the digital and green transitions. The EU, in its efforts to reduce dependence and diversify its relations, will need to address a multi-level approach to achieve its objectives.

Image: Aerial view of an open pit mine. Photo: YouraPechkin.