Introduction[1]

Digital leadership is acknowledged to be one of the four thematic investment windows within the European Competitiveness Fund (ECF), the new instrument designed to consolidate existing innovation and industrial programmes under a single framework, as a centralised one-stop shop, as part of the proposal for the Multiannual Financial Framework (2028-34). Jointly with digital leadership, the other three investment windows are: Clean Transition and Industrial Decarbonisation; Health, Biotech, Agriculture and Bioeconomy; and Resilience and Security, Defence Industry and Space.

The Digital Leadership window, with an indicative budget of €51.5bn (around five times the combined funding of the current Digital Europe Programme and Connecting Europe Facility-Digital) will support investments in AI, semiconductors, cloud-edge infrastructure, cybersecurity, quantum technologies and digital skills ecosystems. This increase places digital policy at the same strategic level as energy, defence and health. It also reflects a growing concern about Europe’s dependencies on non-EU technologies and the need to build a resilient, sovereign foundation for the next wave of industrial and geopolitical competition.

The inclusion of digital leadership among these top priorities marks a shift in the EU’s strategic approach.

Challenges for digital leadership

However, digital leadership is a very broad concept. It needs to be translated into tangible measures. At the same time, the proposals raised by the Multiannual Financial Framework and ECF frameworks pose policymaking questions related to the practical viability, effectiveness and maturity of this digital leadership goal.

The shift from ‘digital transition’ to ‘digital leadership’

The shift from ‘digital transition’ to ‘digital leadership’ signals a qualitative leap: Europe no longer sees the digital sector merely as a support tool for modernisation, but as core infrastructure for competitiveness and security.

However, leadership is a blurred concept which may be understood in five ways (see section below): leadership across the stack; in strategic bottlenecks or by creating chokepoints in identified technologies within the value chain; as a disruptive innovation (the so-called moonshots); as sovereignty or autonomy; or as technological adoption.

At the same time, the MFF and ECF proposals do not set out a specific threshold on what ‘leadership’ means. ASPI’s Critical Technology Tracker accounts for the number of first-tier monopoly that countries have in specific technologies. More than 85% of critical technologies are first dominated by either China or the US. This ‘leadership’ threshold within the MFF requires setting a bar of expectations, scheduling specific goals and ensuring the long-term planning of investments by assuming failures (moving from a risk-averse culture to a risk-taking approach).

It is not about establishing quantitative targets as the Digital Decade framework does. It is about identifying investments and ecosystem generation in those technologies where still there is no definite leadership, such as quantum sensing or certain chokepoints in the biotechnology value chain. Moreover, in those areas where leadership is no longer attainable, leadership should be becoming the right ‘peer’ for third countries to jointly establish R&D ecosystems, unlock institutional private investment into key design, manufacturing and deployment.

Conditionalities proposed by the European Competitiveness Fund and impact on the effectiveness of digital leadership

EU Preference (Article 10) and Accelerated and Targeted Actions (Article 20).

Article 10 of the European Competitiveness Fund sets out the proposal for an ‘EU preference’. Specifically, it refers to the development, manufacturing and exploitation in the Union of strategic technologies and sectors. Eligibility conditions may take the form of four criteria:

- Participation and performance restrictions requiring participating entities to be established, use facilities or perform activities in the member states and, where appropriate, other eligible countries.

- Transfer restrictions requiring recipients of ECF funding, during or within five calendar years after the end of an action, to not directly or indirectly transfer all or certain operations, results or related access and use rights, including granting of licences, from an eligible member state or associated country to an ineligible third country.

- Supply and content restrictions requiring recipients of ECF funding to ensure a certain minimum use or sourcing of equipment, supplies and materials, or their components, unless those supplies and materials cannot be reasonably sourced from those eligible countries.

- Control restrictions requiring recipients of ECF funding to acquire and/or hold the ability to decide, without restrictions imposed by ineligible countries, on the creation and use of results, including the legal authority and practical capability to modify, substitute, or remove components of results that are subject to restrictions imposed by ineligible entities or third countries.

Negotiations over these four criteria should take into account the definitions that this analysis include, as setting ‘digital leadership’ across the stack would not have the same implications as setting leadership as the creation of a strategic bottleneck or a chokepoint within the value chain. Implications may vary for shareholders of a European company, and for control restrictions. Also, it will be important to effectively define digital leadership, as some restrictions from Article 10 may include more specifications for the security, defence and public order areas.

Also, digital leadership needs to be effectively addressed with a clearer view on what Article 20 on Accelerated and Targeted Actions for Competitiveness refers to in the ECF framework. This article proposes actions of imperative public interest or critical time-sensitivity, which could otherwise not be effectively implemented under the normal rules applicable to the Union budget or sectoral policies. The proposal would ensure flexibility with certain additions, exceptions and derogations from applicable law, during the award procedure or implementation of the supported activities. At the same time, it raises the question of what ‘imperative public interest’ and ‘critical time-sensitivity’ mean and how it would be translated into specific measures.

While it is unclear what these concepts still mean in practical terms, a reflection on the recent White Paper on European Defence and the ReArm Europe Plan/Readiness 2030 may shed some light. The plan aims to release public funding for defence at the national level and invites member states to activate the ‘national escape clause’ under the Stability and Growth Pact for the 2025-28 period, and the possibility to unlock around €650bn of additional defence investment at the national level.

With the proposal for the SAFE instruments, whose guiding principles are ‘Buy more, better, together, European’, it aims to increase up to €150bn the available money raised on capital markets, backed by the EU budget, boost defence procurement in critical areas and provide long-maturity loans to support common procurement.

Although in this case there is no reference to ‘imperative public interest’ and ‘critical time-sensitivity’, the way in which the national escape clause might be activated is an example of how exceptionality may function for Article 20 of the European Competitiveness Fund. Also, the functioning of the defence SAFE instrument on procured products that must have at least 65% of domestic content might be related to the idea of imperative public interest.

Other examples may be the DG GROW’s efforts to create ‘strategic stocking’ frameworks, which are meant to be regulatory frameworks for companies to quickly respond to governments’ requirements on critical supplies, such as medicines. However, the implementation at the member states’ level differs with various speeds, intensities, maturity and also interest in setting out these strategic stocking policies.

However, the challenge comes from the different understanding of ‘imperative public interest’ across the 27 member states, which may differ in what they identify as imperative or critical. Also, it poses the question on how a long-term planning of technological products development, design or manufacturing would match with Horizon Europe’s nature, characterised by its independence and its research nature.

Priority-setting and identification of key technologies

Article 39 of the ECF identifies a list of digital technologies where support should be directed to: Artificial Intelligence (including AI Factories and Gigafactories), high performance computing, quantum technologies, semiconductors and photonics, robotics, large data technologies, telco-edge and cloud technologies, 6G and other wireless technologies, communication networks, advanced connectivity, including 6G and other wireless technologies, sensing technologies, cybersecurity and network resilience, software engineering, augmented reality and virtual worlds, digital twins, Union digital identity and business wallets, trust technologies, and new and emerging digital technologies as well as cross-sectoral digital technologies and applications, including those with dual-use potential, support for data technologies and data spaces, as well as submarine cables and non-terrestrial networks.

While all digital technologies are clearly relevant, there is a need for priority-setting of certain technologies (first, second and third tier); the identification of which stages within the value chain would be much more critical; and the establishment of a calendar, plus contingency plus in cases of failure scenario for the development of the technology.

Coordination and coherence with investment windows other than digital leadership to avoid imbalance

The ECF aims to serve as the single, centralised framework to ensure agility, simplicity and intertwined coordination between investment windows. However, it remains essential for coordination to be effective and dynamic. Based on the budget proposed by the Commission, only €51.5bn of the total of expected investments under the ECF would be directed at digital leadership, while €125bn would be devoted to defence and space, and only €26.2bn to environment and €20.3bn to health. Even if under a centralised framework, the ECF risks largely focusing on defence and security. There is a need to ensure that investment windows interact in a cooperative manner.

A clear example is STEP, which will be phased out and will be integrated under the ECF. The Strategic Technologies for Europe Platform under the DG BUDGET was created to focus on serving as the one-stop shop for all types of investments related to creating technologies which would reduce or prevent strategic dependencies of the Union, and maturing an innovative, cutting-edge element with significant economic potential to the Single Market in three areas: clean and resource-efficient technologies; biotechnologies; and digital and deep technologies. STEP has managed 11 EU-funded programmes. However, the 2025 Annual Report showcases that, during its one-year existence, the STEP Seal awarded to this kind of projects has been given to 401 projects. However, 51% of them have been awarded to one single track (clean and resource-efficient technologies, with 202 awards), while only 12 projects have been awarded to biotechnologies and 187 to digital technologies.

This thematic imbalance is accompanied by a concentration of financed projects in a limited set of member states: Spain, France, Germany, Greece, Netherlands and Sweden have concentrated more than half of all projects, while countries such as Slovakia and Slovenia have been granted limited projects.

STEP serves as a testing ground for the next MFF 2028-34. While the STEP framework remains a useful tool to centralise investments, it is relevant to avoid these dual imbalances in the upcoming ECF framework. This is particularly important in the MFF proposal, which reduces the number of programmes from 52 to 16 and adds up –under the centralised framework– the fourth layer of defence, security and dual use applications.

Potential policy approaches to digital leadership

The negotiations for the EU’s next MFF have entered what could be described as their political phase. Institutions and member states start defining the size of each budgetary window and, with so little information available at the moment, one of the only ways that can be done is by shaping the language (and therefore political meaning) that will frame the next cycle of investment. ‘Digital Leadership’ is now the name of one of the major budgetary windows of the next MFF.

The most heard of term in the last budgetary phase was ‘Digital Transition’. The fact that Europe aims to ‘Lead’ and no longer ‘Transition’ is a political statement worth analysing. This phase offers an opportunity to reflect on the following question: what do we mean when we say that Europe should be a ‘leader’ in digital?

The term will shape how Europe invests public resources in its technological landscape. In current debates, at least five interpretations coexist.

(5.1) Leadership as capabilities across the stack

This view sees leadership as building strength in all layers of the digital economy: semiconductors, cloud infrastructure, software and applications. The goal is to reduce dependency at every step of the value chain and to ensure that Europe maintains technological continuity from hardware to services. The European Parliament has explicitly called for sovereign digital infrastructures ‘from semiconductors and connectivity to cloud and artificial intelligence’.

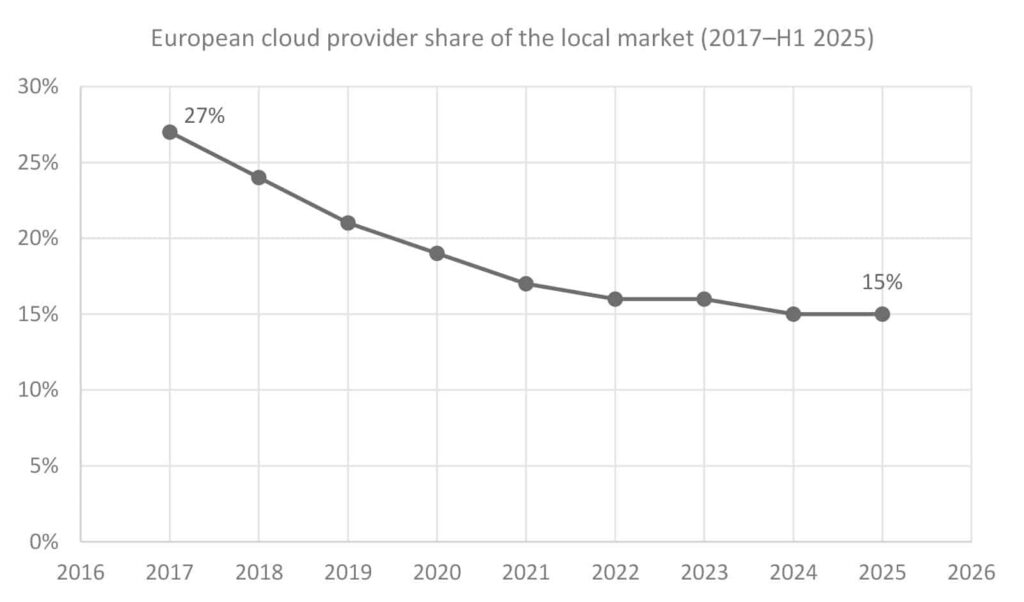

Europe currently produces around a 10th of the world’s chips and has no manufacturing plants below the 10-nanometre process, while the EU Chips Act aims to double this share by 2030 through €43bn in coordinated investment. In cloud computing, US hyperscalers (mainly AWS, Microsoft and Google) still dominate roughly two-thirds of the European cloud market, and most Western data is physically hosted on US servers.

Figure 1. European cloud providers’ share of the local market (2017-1H25)

Leadership in bottlenecks

A second interpretation focuses on a narrower set of critical nodes whose disruption could paralyse the entire digital system. In this view, Europe’s vulnerability lies less in its lack of broad capability than in its dependence on a few external chokepoints: advanced chips, high-performance computing, AI hardware and cloud infrastructure.

The experience of the global semiconductor shortage revealed how Europe’s automotive and electronics sectors depend on a handful of Asian foundries, particularly Taiwan’s TSMC, which alone produces more than half of the world’s leading-edge chips. To mitigate this exposure, the EU is concentrating resources on the most fragile points of the chain:

- The EuroHPC Joint Undertaking now coordinates one of the largest supercomputing networks in the world, built to provide domestic computing power for scientific research and AI model training.

- Europe’s ASML is often cited as an example of successful control of a bottleneck. By monopolising the production of extreme-ultraviolet lithography equipment, ASML gives Europe leverage in one of the most strategic points of the global semiconductor chain.

Leadership as sovereignty or autonomy

Another interpretation links leadership to Europe’s capacity to remain secure and operational. The goal here is to be protected from coercion in a context where major powers such as the US and China increasingly weaponise interdependencies in terms of access to technologies, supply chains and infrastructure. In this respect, digital sovereignty is about ensuring that Europe’s critical systems cannot be disrupted or manipulated from abroad.

Many voices are pushing Europe to use the current geopolitical situation as a motivation to build the strategic autonomy required to resist external pressure, safeguard economic continuity and maintain decision-making freedom.

Leadership as disruptive innovation (or moonshots)

Under this view, Europe can lead only by producing technologies that change the frontier itself. When you are the first to produce or master a new technology, then you are undoubtedly a leader, under this understanding of leadership.

For example, the European Commission’s new Quantum Strategy, backed by the €1bn Quantum Technologies Flagship, aims to establish pilot production lines for quantum chips and to launch a quantum-Internet prototype by 2030.

Similar ambitions are visible in the space domain, where the upcoming IRIS² constellation and new reusable-launcher programmes are meant to secure Europe’s place in the space-digital economy.

The ‘moonshot’ logic behind quantum computing, foundation AI models and the integration of space and digital technologies follows this idea: to secure Europe a first-mover advantage in the next technological revolution.

Leadership as adoption

In 2023 over 90% of people in the EU used the Internet weekly, though only 56% had basic or above-basic digital skills. By year-end 2024, 74% of EU firms had reached a basic level of digital intensity (SMEs ~73 %), and, in 2022, 69% of European firms had adopted advanced technologies such as AI or robotics, only slightly behind the 71% rate in the US.

Still, many small firms and less connected regions remain behind. The AI Continent Action Plan aims to close this gap by helping companies apply AI in practice and by launching an AI Skills Academy to train workers in data and digital competences.

Concentration, diversification and the role of enabling infrastructure

All these interpretations of digital leadership are valid and to a large extent complementary. Europe needs capabilities across the stack, control over bottlenecks, technological sovereignty, adoption and innovation. There is a certain level of ambiguity that could be a strategic disadvantage and could lead to a bad alignment between stakeholders, which is precisely a sine qua non condition for competitiveness.

The report The European Way – A Blueprint for Reclaiming our Digital Future can offer a way out of this ambiguity. It argues that leadership should be measured by the capacity to create shared systems that endure while serving a long-term vision of human-centric progress, thus shifting the focus from a domination paradigm.

One of the very few certain future trends in tech consumption is that there will be an increasing interest in reliable, transparent and explainable technologies. The demand for such systems is growing fast: global spending on AI transparency tools is projected to exceed US$2.5bn by 2027, with annual growth above 25%. It would be a realistic bet for Europe to aim to gain leadership in this growing niche.

From competing to designing

Therefore, Europe’s digital strength will not come from out-scaling the US or China but could come, in some parts of the stack, from out-designing them: developing enabling infrastructures and software architectures that are transparent, auditable and trusted, and that can therefore compete in the markets.

Europe should not compete in a race for digital capabilities just for the sake of competing in the race. The goal should be to protect European security and economic security, and to lead in human-centric technology. That requires clarity on priorities and discipline on where Europe must be strong. It also requires the enabling conditions that let firms and public services adopt technology at scale. The question is not ‘how to spend more’, but how to spend so that Europe is safer, freer and more productive.

For the next MFF, should it concentrate its resources or diversify them? Concentration allows for critical mass and visible champions but also risks rigidity and capture. Diversification encourages competition and experimentation yet may dilute impact. The wisest approach would be to concentrate resources in sectors where dependencies are clear and diversify where there is a high degree of uncertainty.

The tension is re-emerging as industrial policy returns to the EU agenda. On the one hand, concentration could accelerate Europe’s presence in strategic nodes (chips, cloud and AI factories). On the other hand, diversification protects the innovation base across sectors and regions, knowing the political fragmentation between member states and regions that exists in the EU.

Betting too narrowly on one set of technologies may help close today’s gap, but it risks losing traction in the next innovation wave. Japan’s experience in the 1990s illustrates this: a few decades of state-backed focus on electronics and automotive created global champions, yet the same focus left the country less prepared for the software and Internet revolutions that followed. Europe faces a similar risk if the current AI and semiconductor drive turns into a closed corridor rather than a bridge to future technologies.

Promoting enabling infrastructure

Enabling infrastructure refers to the set of shared assets and systems that make technological progress possible across sectors and over time. It comprises three main layers:

- Technical infrastructure such as connectivity networks, cloud and edge computing, data storage and processing facilities, testing and certification environments, access to high-performance computing, etc. These elements would allow the EU to maintain the physical and digital capacity needed for research, experimentation, and deployment.

- Financial and regulatory infrastructure such as funding mechanisms, procurement frameworks, and investment tools. The long-term goal here should be that this financial and regulatory infrastructure strengthens private investment, mainly by lowering risk and lower risk and coordinating private and public incentives.

- Human-capital and institutional infrastructure such as education and reskilling systems, research institutions that ensure knowledge transfer and interoperability between sectors and member states.

Enabling infrastructure is a long-term policy commitment to flexibility and interoperability and should be the core of this MFF’s digital leadership funding.

Southern Europe in this equilibrium

In the past funding cycles, Southern Europe has consolidated its position in the EU’s digital landscape through NextGenEU and Horizon Europe. Yet, as Enrico Letta warns, the reliance on extraordinary funds cannot last. The region must attract private investment and align national priorities within a shared European strategy.

The balance between concentration and diversification should lie in the development of enabling infrastructure, serving multiple policy goals at once, linking competitiveness with cohesion and defence. For example, investments in cloud-edge networks or cybersecurity capacity can simultaneously improve industrial performance and protect critical systems, not to mention job creation.

Enabling infrastructure must reflect the specific assets and needs of all European countries, including Southern European ones. Each of the member-state economies has developed distinct capabilities that can form part of a coordinated European base for competitiveness and resilience:

- Greece has become one of the most effective EU members in capturing and aligning research funding, especially through Horizon Europe. Greek institutions occupy six of the 10 top positions among widening countries by funds won, and research centres such as CERTH (Centre for Research and Technology Hellas) have secured more than €100mn in Horizon grants. The next step is to transform this project participation into industrial capacity through new laboratories, digital innovation hubs and technology transfer centres. Strengthening the interface between research and industry would allow Greece to embed its EU-funded research base into the wider enabling infrastructure of AI, clean tech and energy.

- Italy combines a large domestic market with one of Europe’s most diversified industrial fabrics. It ranks as the EU’s second-largest manufacturing power and the world’s seventh. Future EU support should target national cloud and IoT platforms, 5G connectivity, and sectoral innovation hubs linking SMEs, startups and traditional industries. There is potential for this existing industrial base to gain digital maturity and become the source of new European champions.

- Spain’s strength lies in its highly educated workforce: 46.4% of workers hold tertiary education, compared with a eurozone average of 39% and its position as Europe’s bridge to Latin America. Spanish companies have invested nearly €150bn across the region. Building on this, Spain can become a hub for AI development in Spanish, leveraging HPC infrastructure such as the Barcelona Supercomputing Centre and new EU-funded AI factories. European funds should also support retention of technical talent and partnerships with Latin American research ecosystems. Spain’s enabling contribution would therefore link computational capacity with linguistic diversity and knowledge diffusion. Spain has confirmed two AI factories: one for computing power access via the Barcelona Supercomputing Centre, and another one focused on AI and health in the region of Galicia. Spain has applied, by November 2025, to one of the AI Gigafactories, still waiting for a decision.

- Portugal stands out as a fast-growing innovation hub, with more than 4,700 active start-ups, and now achieves 90.7% of the EU average in the European Innovation Scoreboard. Its policies for attracting global talent (favourable taxation, start-up visas and an open innovation culture) have made it an ideal testing ground for Europe’s next generation of entrepreneurs, but have also generated internal tensions, due to the gentrification of some neighbourhoods in Lisbon and Porto and have become very attractive for ‘digital nomads’ and expats. EU funding should reinforce this foundation by extending innovation infrastructure beyond Lisbon and Porto, improving connectivity, and financing venture co-investment mechanisms that allow start-ups to scale within Europe.

These are some of the assets Southern Europe can bring to the table. However, if they were sufficient, the region would already be a technological powerhouse without the need for public intervention, and that is clearly not the case. The EU (and all the stakeholders involved) need to define the enabling infrastructure we still need to achieve digital leadership under Europe’s preferred goals and to remain competitive in future technological revolutions.

This requires designing enabling infrastructure as a territorial system, not a zero-sum race. Each member state should contribute according to its comparative strengths (research capacity, industrial base, talent or connectivity) so that together they form an integrated and interoperable set of capacities capable of sustaining Europe’s technological development over time.

[1] This paper was originally published as a chapter of the PromethEUs’ joint publication Making the EU’s 2028-2034 Multiannual Financial Framework Work for Southern Europe, published on 9/XII/2025. PromethEUs was a network bringing together four think tanks from southern EU countries: I-Com, Institute for Competitiveness (Italy), IPP Lisbon (Portugal), the Laboratory of Industrial and Energy Economics at the National Technical University of Athens (Greece) and the Elcano Royal Institute (Spain). Each partner authored one of the chapters in this joint publication.