Executive summary

This Policy Paper analyses the changes in the gas relationship between the EU and Russia since the invasion of Ukraine in February 2022. The analysis starts by setting out how pipeline imports have fallen by 80% due to the requirement to pay for gas in roubles, the suspension of many existing contracts and the sabotage of the Nord Stream pipelines. The reduction has had a significant impact on Gazprom’s influence over the EU, as the Russian state-owned company, which has a monopoly over pipeline exports, has lost its principal and most lucrative market and has been the object of numerous international arbitration proceedings. [1]

In contrast, and despite the sanctions, the Russian private company Novatek has successfully developed the liquefied natural gas (LNG) sector, gaining market share in the EU and maintaining deliveries since the invasion. However, there are doubts as to Novatek’s capacity to sustain its projects in a context of increased international pressure and the loss of important western commercial and technological partners, which means it is unlikely to be able to replace Gazprom in terms of volume and income, and thus does not constitute a geopolitical risk for the EU.

The main conclusions of this paper are that, while the EU has experienced a profound energy crisis, Russia has not achieved the prime objective of its gas blockade: to break the EU’s support for Ukraine. The EU has discovered that it can ensure its energy supply without depending on Moscow, and it now has to define a strategy that will establish the role of Russian natural gas in the European energy mix in the future.

The EU’s political architecture means that the impossibility of achieving unanimity among Member States will hamper its development of a joint policy and its ability to achieve the objective established in REPowerEU of ending of Russian hydrocarbon imports by 2027. Faced with stalemate in the Council of the EU, Member States must design and implement their own policies of energy diversification and uncoupling from Russia, and this will incentivise fragmentation, and, in practice, prevent a clean break in the gas relationship. It is likely that Russian gas will continue to be delivered either via pipeline or in the form of LNG to many EU Member States who decide not to impose strict measures, even after 2027. However, the volumes will be far lower than Russian exports to the EU prior to the invasion, as Russia will be competing with other suppliers (primarily North American and Qatari LNG) in a context of decarbonisation and the likely fall in demand in Europe.

Conclusions

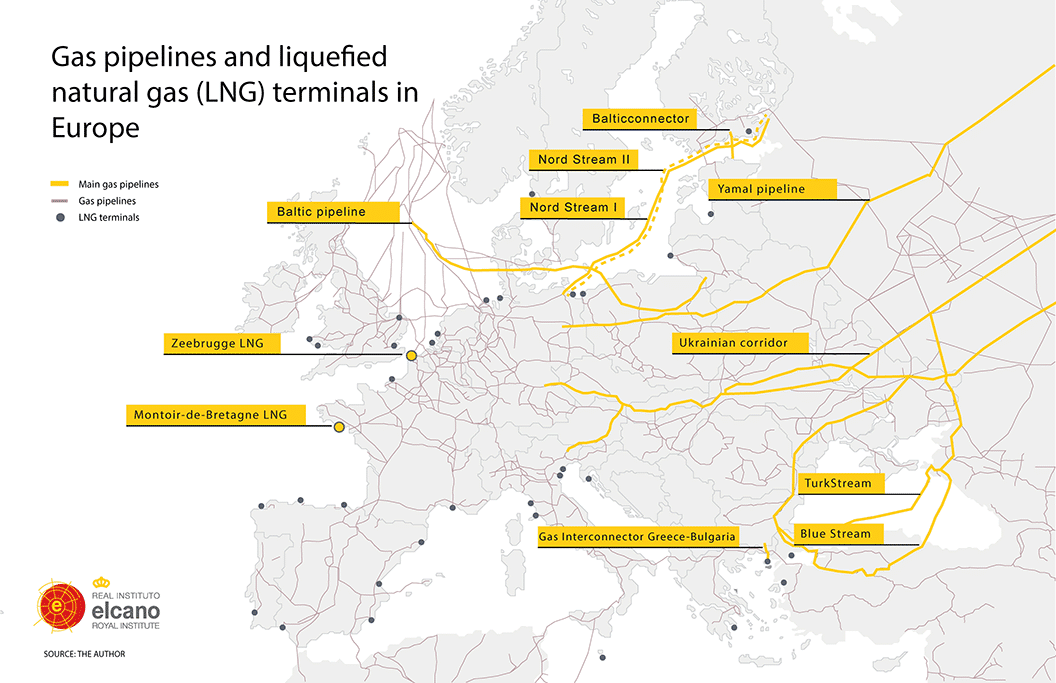

The EU has achieved an 80% reduction in deliveries of Russian natural gas by pipeline without having recourse to energy rationing or renouncing its political, economic and military support for Ukraine. While Russia accounted for 42% of European imports of natural gas in 2021, this percentage had fallen to 14% by 2023 (5.3% LNG and 8.7% pipeline gas). Thanks to the development of new capacities to import LNG and the construction of interconnections, the EU has entered a new phase in its decoupling from Russian gas, allaying fears of fuel shortages. The objective now is to develop a strategy to determine the future of Russian natural gas until 2027, the date established in REPowerEU for the end of the purchase of hydrocarbons from Russia.

In the case of pipeline imports, the operational return of Nord Stream can be ruled out, while for political reasons a resumption of flows via Poland (the Yamal pipeline) seems unlikely. The Ukraine transit contract will expire on 31 December 2024 and Kyiv has announced its intention not to negotiate a renewal agreement with Gazprom. Although in recent months, as part of its conversations with Hungary and Slovakia, Ukraine has opened the door to occasional deliveries of Russian gas continuing after 2024, it seems clear that these flows will be smaller than at present and would be of a provisional nature. This situation would mean that only TurkStream would be operational for deliveries of natural gas to Gazprom’s few remaining clients in the EU. TurkStream is expected to be able to absorb a marginal element of the volumes diverted from Ukraine from 2025 onwards, principally to supply Slovakia and Hungary, provoking the suspension of the remaining long-term contracts not served by Gazprom, such as those with Austria and Italy. While European countries are implementing diversification plans and remain aligned with the 2027 objective, Hungary has demonstrated its intention to continue importing Russian gas by signing new long-term contracts after the invasion. Although the position of Viktor Orbán’s government with respect to Moscow remains the exception in the EU, it sets a precedent that could undermine the will of those Member States that have the option of continuing to receive Russian gas via TurkStream.

In the case of LNG from Yamal, EU countries continue to comply with their long-term contracts while sanctions are technologically strangling Novatek’s new projects (Arctic and Murmansk) and preventing it from acquiring logistical and technological capacities. If the purchase of ice-breakers and trans-shipment services in European ports is restricted, a large part of Yamal’s production destined for Asia will face logistical difficulties during the winter, while restricting access to western technology would delay or even paralyse new projects in the Arctic. Given the growing liquidity and flexibility of the global LNG market, EU gas importers should not have any problem finding alternative suppliers to Russia, and will now be able to benefit from the new joint gas purchasing platform to negotiate these additional volumes on an aggregate basis. It will be harder to reconcile the EU’s commercial interests in Novatek projects (such as the participation of TotalEnergies, engineering and services suppliers, or utility providers with long-term contracts) with the elimination of Russian gas imports and the implementation of sanctions on LNG and the associated value chain.

Any decision to impose sanctions requires the unanimity of Member States in the Council of the EU. The capacity to achieve such consensus in Brussels with respect to sanctions on Russia has clearly weakened in recent months, due to the Hungarian veto in particular but also because of the stagnation of the conflict. This blockage has given rise to a new phase in European energy policy towards Russia, in which binding decisions will depend on the willingness of each individual Member State. In this scenario of ‘soft rules’ it is likely that Gazprom and Novatek will seek to exploit potential European divisions, offering beneficial conditions to those buyers who decline to go along with the Commission’s calls, in practice limiting the possibility of completely ending the gas relationship by 2027.

Despite this fragmentation at the EU policy level, Russian gas will play an increasingly marginal role in Europe, competing with other suppliers (primarily LNG from the US and Qatar) in a context of decarbonisation and with demand forecast to fall. In conclusion, then, Russia’s gas blockade has failed, sacrificing the country’s most lucrative energy market without breaking European support for Ukraine.

[1] The author would like to acknowledge the contributions of Gonzalo Escribano and Luís María González Sánchez.

Image: Natural gas production plant near Novy Urengoi, Russia. Photo: Vostok / Getty Images.