Even before its large-scale invasion of Ukraine, Russia had already consolidated itself as an energy superpower in Europe and as the dominant player in the global fertiliser market between 2014 and 2022, displaying especially pronounced primacy from 2021 onwards. This structural position now shapes its ability to capitalise on geopolitical disruptions.

The global market is by no means diversified, but rather segmented, and Moscow dominates precisely the critical segments.

Iran’s strategy of blockading the Strait of Hormuz by means of naval mines, coastal missile batteries and swarms of drones has placed the global economy in a state of utmost vulnerability. Soaring energy prices have been the most immediate manifestation of this. Here, the US decision to temporarily lift certain sanctions to enable Russian energy exports to resume has created an unexpected windfall for Moscow. The crisis in Iran threatens to set back Western efforts to curb Russia’s ability to finance its war, by driving up the prices of oil and gas and increasing dependence on its exports. It effectively constitutes the greatest challenge to the sanctions regime since the start of the full-blown war in Ukraine.

The consequences for energy have been widely analysed. Far less attention has been paid to an equally critical dimension, however: the risk of an acute crisis in the fertiliser and food markets. In this regard, Russia is not only well placed to extract economic benefits but also to strengthen its geopolitical influence. Its ambition of becoming an indispensable supplier of food security to the global south, or what the Kremlin refers to as the ‘world majority’, finds a strategic opportunity in this particular set of circumstances.

This goal is not new. In 2022, Russia oversaw the Black Sea Grain Initiative with the United Nations, Turkey and Ukraine. The agreement enabled the safe export of millions of tonnes of Ukrainian grain from ports such as Odessa, relying on protected sea lanes and international inspection measures, while also facilitating Russian agricultural exports. Although the agreement held for almost a year, Russia backed out in 2023 alleging acts of non-compliance, thereby demonstrating its willingness to instrumentalise such mechanisms as tools of political pressure.

Even before the escalation in Iran, the global food system had already been under significant structural strain. Over the past five years, acute food insecurity has undergone a threefold increase and almost 400 million people face the prospect of severe hunger, according to the World Food Programme. Countries such as Sudan, Somalia and Afghanistan were already on the brink of famine.

The war in Iran has had a direct effect on the fertiliser market, with profound implications for global agricultural output. Around half the world’s trade in urea, the main component of nitrogenous fertiliser, passes through the Strait of Hormuz. Meanwhile the production of ammonia, which is essential for these fertilisers, relies on natural gas, hence the importance of the Gulf states in this market. In total, almost a third of the global maritime trade in fertilisers uses this strategic shipping lane. It is a corridor that has been virtually paralysed since the end of February. Shipping has been cut by almost 90%, according to figures from Lloyd’s List Intelligence. As a consequence, urea prices have risen almost 40%, reaching their highest level since 2023.

During the 2022 food crisis, created by the war in Ukraine, sanctions and the suspension of exports through the Black Sea, food prices reached historic highs. In the current scenario, Russia and Belarus once again emerge as key suppliers. Both countries account for a substantial share of global fertiliser supplies and, unlike the Gulf producers, are unaffected by the disruptions in the Strait of Hormuz.

Russia and Belarus taken together account for around 40% of world potash exports, 23% of ammonia and 14%-16% of urea. Their productive capabilities, access to cheap gas, subsidised infrastructure and diversified logistical routes provide them with a structural competitive advantage that remains intact.

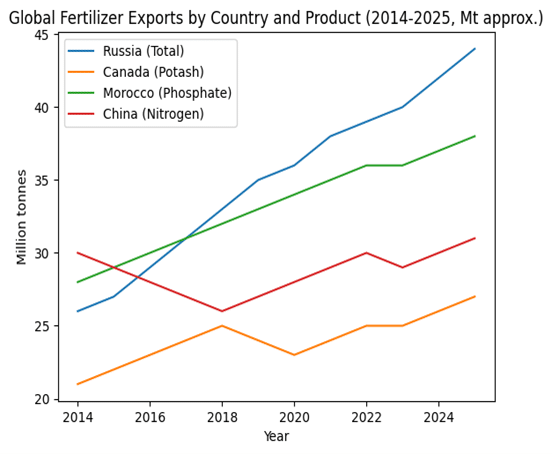

The fact that Russian fertilisers and agricultural products have largely remained outside the scope of the sanctions regime, owing to the strategic role they play in global food security, has enabled Russia to maintain and even increase its market share since 2022, as shown in Figure 1. Unlike other exporters, which specialise in specific sectors, Russia is the only actor with an across-the-board presence in the main types of fertiliser. The global market is by no means diversified, but rather segmented, and Moscow dominates precisely the critical segments.

Figure 1. World fertiliser exports by country and by product, 2014-25 (tonnes mn approx.)

In this context, importers who have lost access to supplies originating from the Gulf are turning to Russia as an alternative. Countries such as Nigeria and Ghana are already increasing their orders in anticipation of prolonged disruption. This reaction reflects the clear logic of the market, but also strengthens a structural dependence with political implications.

The prospect of food inflation in the coming years seems almost inevitable and its effect will be uneven. Whereas in the West it will translate into an increase in the cost of living, in vulnerable regions such as the Sahel and southern Asia it could unleash large-scale humanitarian crises. Against such a backdrop, Russia finds itself in a position that bolsters its long-term strategic interests: a structural indispensability in the global food chain that combines sustained economic benefits with significant political capital. By taking advantage of the disruptions to fertiliser and food supplies, Moscow strengthens its ability to exert influence beyond its immediate neighbourhood, especially in the Global South. This dynamic not only weakens the efficacy of the sanctions regime but also reveals a fundamental drawback of Western strategies: the difficulty of isolating a power that controls critical hubs in the global network of interdependence.

More than just an economic windfall, what is at stake is the prospect of Russia becoming an indispensable systemic supplier. In a world characterised by overlapping crises, this ability to supply essential resources could prove more decisive than military or energy power by themselves. The war in the Middle East, far from isolating Russia, could be contributing to strengthening its centrality in the emerging global order and thus fit with the Kremlin’s strategic ambitions of becoming the leader of an upcoming multipolar world.