Theme: Spanish outwardinvestment is growing again after a period when disinvestments exceeded investments.

Summary: Spain has the EU’s sixth-largest stock of direct investment abroad. After a period of consolidation following the onset of Spain’s recession in 2009, which led some of the main multinationals to sell assets regarded as non-strategic, particularly those that needed to reduce their debt levels, companies are investing again. Almost two-thirds of the total revenues of the blue chip Ibex-35 companies are generated abroad. At the forefront of Spain’s new wave of internationalisation are the big construction and infrastructure companies.

Analysis

Background

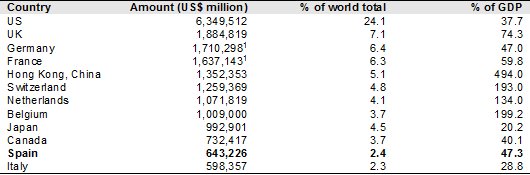

Spain’s stock of outward direct investment stood at US$643.2 billion at the end of 2013, up from US$636.7 billion in 2012 and the 11th largest in the world (the sixth in the EU), according to the 2014 World Investment Report published by UNCTAD on 24 June (see Figure 1). This compares with a stock of inward foreign direct investment of US$715.9 billion. The stock of outward investment is 41 times higher than in 1990.

Figure 1. Stock of Outward Foreign Direct Investment (US$ million and % of world total), 2013

(1) Estimates.

(2) Based on the IMF’s GDP figures (April 2014) for 2013, not UNCTAD’s as not yet released.

Source: World Investment Report 2014, UNCTAD.

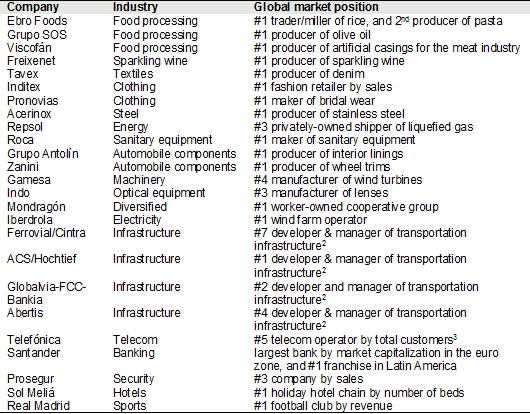

Most of the investment abroad was made in the last 25 years, and with it the creation of a core group of multinationals with significant positions in the global market (see Figure 2). These companies comprise the most dynamic part of the economy and are playing a significant role in helping it to recover. Among the best known is Inditex, the world’s largest fashion retailer, whose flagship store is Zara, one of the group’s eight brands. Inditex has close to 6,400 stores in 88 countries. Santander, the euro zone’s largest bank by market capitalisation, earned a larger slice of its net profits in Brazil (20%) in the first quarter of 2014 than in Spain (14%).

Figure 2. Spanish multinationals with the largest global market positions (1)

(1) Latest available.

(2) Ranked by number of road, bridge, tunnel, rail, port and airport concessions over US$50 million investment value put under construction or operation as of 1 October 2013.

(3) This takes into account approval of Telefónica’s acquisition of the Dutch KPN’s E-Plus German mobile unit.

Source: compiled by William Chislett, Esteban García-Canal and Mauro F. Guillén from Interbrand, Public Works Financing, BrandFinance, Bloomberg New Energy Finance, the Spanish Business Council for Competitiveness and company reports.

Spain has three companies in the world’s top 100 non-financial transnational corporations (see Figure 3).

Figure 3. Spain’s presence in the world’s top 100 Non-financial TNCs, ranked by foreign assets (1)

(1) 2013.

(2) The Transnationality Index is calculated as the average of the following three ratios: foreign assets to total assets, foreign sales to total sales and foreign employment to total employment.

Source: World Investment Report 2014, UNCTAD.

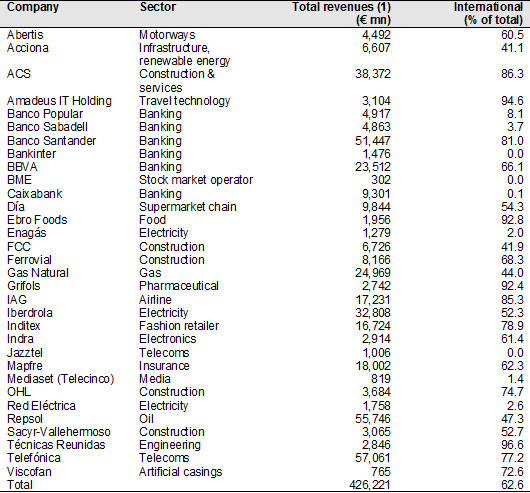

Close to two-thirds of the revenues of the blue-chip Ibex-35 stock market index were generated abroad last year, around double the proportion of a decade ago (see Figure 4). Thanks to their geographic and business diversification, these companies are able, to varying degrees, to offset the decline in business at home.

Figure 4. International revenues of Ibex-35 companies, 2013 (€ million and % of total revenues)

(1) Figures rounded to nearest whole number.

Source: National Securities Market Commission.

Spanish companies began to invest abroad in the 1960s, but it was not until the country joined the European Community in 1986 and adopted the euro as its currency in 1999, which enabled companies to raise funds for their acquisitions at rates unimaginable just a few years back, that outward investment took off. EU membership changed the strategic focus of corporate Spain from one of defending the relatively mature home market –much more open to other EU countries– to aggressively expanding abroad. The liberalisation of the domestic market as European single market directives began to unfold made the big Spanish companies, especially the state-run companies in oligopolistic sectors such as telecommunications (Telefónica), oil and natural gas (Repsol and Gas natural) and electricity (Endesa) –all of which were to be privatised and become cash rich– and the big private sector banks, Santander and BBVA, conscious of the need to reposition themselves in the more competitive environment.

Outward investment surged from an annual average of US$2.3 billion in 1985-95 to US$30.4 billion in 1995-2004 and US$94.3 billion in 2005-07 before dropping sharply to an average of US$31.4 billion in 2008-2013 during Spain’s economic crisis.

Latin America was a natural first choice for companies wishing to invest abroad. In the words of the Spanish economist Mauro Guillén, an expert on Spain’s multinationals, it was the ‘path of least resistance’. The shift away from Latin America as of the early 2000s, after Argentina’s financial meltdown, and into Europe, particularly the UK, and the US and Asia, to a lesser extent, was marked by several emblematic investments –Santander’s €11.5 billion purchase of the UK bank Abbey in 2004, Iberdrola’s €17.2 billion purchase of Scottish Power in 2007, the acquisition by Banco Bilbao Vizcaya Argentaria (BBVA) of two small banks in California and Texas and Telefónica’s purchase in 2005 of a stake in China Netcom and in 2006 its €26 billion acquisition of the O2 mobile telephony operator in the UK, Germany and Ireland–.

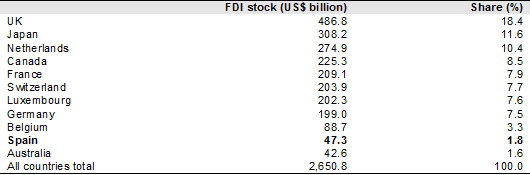

Spain has built up a significant presence in the UK (see Figure 5). Its stock of investment in the UK increased from a mere US$879 million in 2001 to US$66.2 billion in 2012 (latest year available).

Figure 5. FDI stock in the UK, by major source economy, 2012 (US$ billion)

Source: World Investment Report, 2014, UNCTAD.

Telefónica was one of the five winners last year of Ofcom’s 4G mobile spectrum auction, and will invest €640 million. Ofcom attached a coverage obligation to Telefónica, obliging it to provide broadband service for indoor reception to at least 98% of the UK population and at least 95% of the population of each of the UK nations by the end of 2017 at the latest.

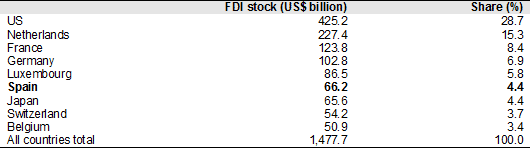

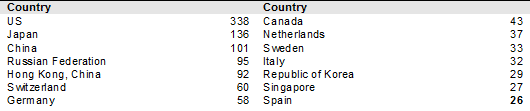

The stock of Spanish investment in the US, a market that the country has found difficult to break into (exports to the US only account for around 4% of Spain’s total, roughly the same as those to tiny neighbouring Portugal) grew 10-fold over the last decade to US$47.3 billion in 2012, the latest year available (see Figure 6). Spanish companies generated about 10,000 new jobs in the US in 2012.

Figure 6. FDI stock in the US, by major source economy, 2012 (US$ billion)

Source: World Investment Report 2014, UNCTAD.

The government is an enthusiastic supporter of free trade and investment agreement between the EU and the US, known as the Transatlantic Trade and Investment Partnership (TTIP), which began to be negotiated last July. On the investment side, Spanish officials see enhanced possibilities in public procurement where some Spanish companies are already successful in winning contracts for transport infrastructure.

The onset of recession in Spain as of 2009, after bumper investment abroad of US$74.7 billion in 2008, led some of the main multinationals to either consolidate their positions or disinvest, particularly those that needed to reduce their debt levels. This was the case, for example, of Iberdrola, the world’s largest operator of wind farms, which sold farms in France, Germany and Poland, and Telefónica, which sold the broad band business of O2, its UK subsidiary, and its Irish mobile phone operator.

In the case of the oil major Repsol, the Argentine government expropriated in 2012 its majority stake in energy firm YPF, in its day (1999) Spain’s largest acquisition (US$14.9 billion and 20% of Spain’s total investment in Latin America between 1992 and 2001). The two sides came to a compensation agreement in February 2014 after a protected legal and political battle under which Repsol received US$5 billion in sovereign bonds, half of what it had initially demanded. Repsol also sold in May its remaining 12% stake in YPF.

The latest situation

Spain’s net investment outflows last year of US$26 billion were the fifth largest in the EU and the 14th globally (see Figures 7 and 8). This figure represented a significant turnaround on 2012 (US$3.9 billion negative as disinvestments exceeded investments).

Figure 7. Outflows of Spanish direct investment 2008-13 (US$ billion)

Source: World Investment Report 2014, UNCTAD.

Figure 8. FDI outflows: top home countries in 2013 (US$ billion)

Source: World Investment Report 2014, UNCTAD.

Among last year’s investments, Santander acquired an 8% stake in China’s Bank of Shanghai for €470 million, and Prosegur, one of the world’s largest security firms, bought Chubb’s cash-in-transit armoured vehicles unit in Australia for €95 million. Santander agreed this month to acquire GE Capital’s consumer finance unit in Sweden, Denmark and Norway for around €700 million. The bank is already the largest provider of loans to buy cars in the Nordic region.

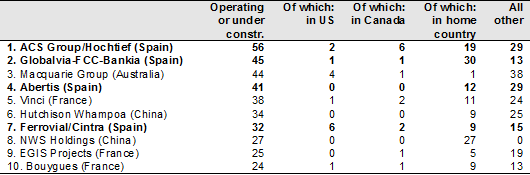

The most promising area for Spanish investment continues to be in the infrastructure sector. Spain has gained an international reputation for its participation in mega projects, most notably the widening of the Panama Canal by a consortium led by Sacyr and Italy’s Impregilo. The country already has five companies among the world’stop-10 global transport developers (see Figure 9). Another four Spanish companies make the list of the top 37.

Figure 9. Ranking of the world’s largest transport developers

(1) Ranked by number of road, bridge, tunnel, rail, airport concessions over US$50 million in investment value and under construction/operation as of 1 October, 2013.

Source: Public Works Financing.

This canal project threatened to damage Spain’s reputation when a dispute over cost overruns earlier this year delayed work. The row was resolved, however, when the consortium and the Panama Canal Authority agreed to invest an extra US$100 million in the project.

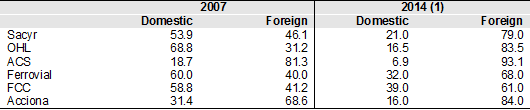

Over last year, OHL has won an €800 million contract in partnership with Samsung C&T to build two stations for Doha’s underground railway network, which followed the award in 2011 of a €6.7 billion contract to a Spanish-Saudi consortium including OHL to build and operate the high-speed rail track between Mecca and Medina; a consortium led by FCC, the Citizen Services Group, landed a €6 billion contract to build three lines of the Riyadh subway system, the longest in the world and the largest international contract in the history of Spain’s construction industry, and Técnicas Reunidas won a €750 million contract to design and build natural gas processing plant in Algeria. The international share of construction backlog of the largest companies has risen considerably since 2007 (see Figure 10).

Figure 10. Construction backlog of main Spanish infrastructure companies (% share of domestic and foreign business)

(1) Latest data, as published in El País, 19 May, 2014.

Source: Companies and National Securities Market Commission.

A Spanish consortium has been prequalified to bid for the US$12 billion project to build the Grand Inga hydroelectric power station in the Democratic Republic of the Congo. This project was stalled in 2012 and revived in May 2013. The winner will be selected in the summer, and if it is Spain it would be an extra feather in its internationalisation cap.

Conclusion: The rebound in investment abroad is enhancing corporate Spain’s position on the global stage and enabling it to better weather its still weak domestic market.

William Chislett

Associate Analyst at the Elcano Royal Institute and author of three books on Spain published by the Institute. Oxford University Press published his latest book on Spain last September