Theme: Spanish civil engineering, construction and infrastructure companies are winning more big contracts abroad.

Summary: A spate of major contracts won over the last month in Australia, Brazil and the US has strengthened Spain’s already commanding position in the global infrastructure market. The potentially most interesting development is Ferrovial’s take-over bid for Australia’s Transfield Services, as it is a stepping stone to China.

Analysis

Background

Anyone who has been coming to Spain over the last 30 years can testify to the striking transformation of the country’s infrastructure, with the building of a network of world-class motorways, airports and a high-speed railway line, the second largest in the world after China. If any criticism can be made it is that excessive emphasis was placed on improving infrastructure and not enough on enhancing human capital, as the country’s long economic crisis and an unemployment rate of 23.7% continues to reveal.

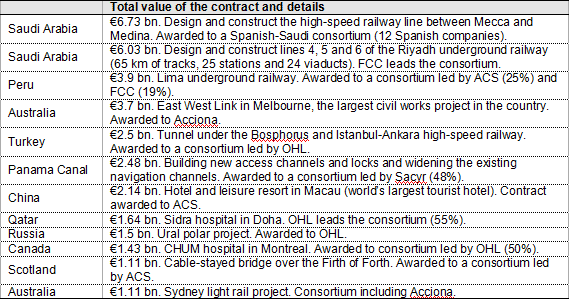

What is generally less well known is the success of Spanish companies in winning flagship infrastructure contracts abroad, including the building of the high-speed railway line between Mecca and Medina in Saudi Arabia and the widening of the Panama Canal, to name just a few (see Figure 1).

Such contracts, together with acquisitions by Spanish companies and banks, are enhancing the country’s global presence. Spain is currently ranked fifth in the world in terms of its degree of internationalisation, with an exposure to overseas countries (measured as trade plus direct investments over GDP) of 166%, similar to Germany and higher than France, according to a recent report by PricewaterhouseCoopers (pwc).[1]

Figure 1. Major infrastructure works led by Spanish companies

Source: Ministry of Foreign Affairs and Co-operation and companies.

The origin of this extraordinary success, which has helped the companies weather the severe downturn in Spain’s once booming construction and infrastructure sector, can be dated back to the late 1960s and 1970s when the process of using toll roads to build infrastructure began as the country’s mass tourism industry was in the throes of being established. Unlike France and Italy, however, Spain did not choose the model of having state-owned companies develop roads and opted for a mainly private sector model.

Another factor was that the roads began to be open to the public in the early 1970s before energy-dependent Spain was dealt a blow by the oil crisis. The government offered to buy back the shares in the under-used toll roads from companies, but they decided to hang on as the contracts for the concessions were long-term. When the crisis ended and the market improved, the roads proved to be profitable.

All of this was valuable experience, particularly after Spain joined the EU in 1986 and the euro zone in 1999 and the country felt the full blast of competition. This led companies to expand abroad. The domestic market had also become too small.

Latin America was a natural first choice for Spanish companies wishing to expand. As well as the companies’ own push factors, there were several pull factors. Two of them were purely economic: liberalisation and privatisation opened up sectors of the Latin American economy that were hitherto off limits, and there was an ongoing need for capital to develop the region’s generally poor infrastructure. Two are cultural: the first is the common language and the ease, therefore, with which management styles can be transferred. Another attraction is the sheer size of the Latin American market and its degree of underdevelopment. Spanish executives were ideally suited to handling new businesses in Latin America, as they had gained a lot of experience of how to compete in industries under deregulation in their own country. Lastly, financing for these companies became much cheaper after Spain joined the euro.

The first toll-road concession in North America was gained by Cintra, a subsidiary of Ferrovial, in 1999 in conjunction with Australia’s Macquaire Bank when it won the tender for Toronto’s Highway 407 –a 99-year-contract and the largest privatisation in Canada’s history–. The contract eased Cintra’s path into the US where in 2004 it purchased the rights to improve and operate the Chicago Skyway, the city’s only toll road, for US$1.83 billion, for the next 99 years.

Spanish companies have gradually gained contracts in many other areas of infrastructure apart from toll roads. In 2013 they won contracts abroad worth more than €35 billion; their portfolio of international projects tops €75 billion. More than 80% of the big companies’ portfolios comprise contracts abroad. This compares with spending on public works in Spain, which plummeted from €39.8 billion in 2008 to €6 billion in 2012.

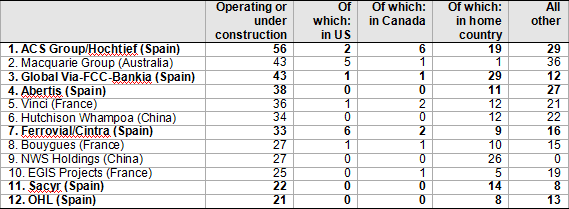

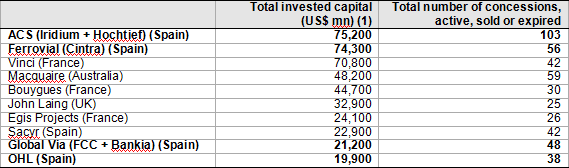

For several years there have been more Spanish companies in the annual ranking of the world’s top transportation developers by the US publication Public Works Financing than any other country. The latest ranking, released on 4 November, has six Spanish companies in the top 12 and another three make the top 39 (see Figures 2 and 3).

Figure 2. Ranking of the world’s 12 largest transportation developers

(1) Developers are ranked by the number of road, rail, port and airport concessions over US$50 million in investment value that they have developed worldwide, alone or in joint venture, and are currently operating or have under construction as of 1 October 2014.

Source: Public Works Financing.

Figure 3. Developers ranked by invested capital (1985-2014)

(1) The sum of the original investment, in nominal dollars, of all of a company’s transportation P3 projects that it has financed and put under construction and/or operation, or acquired and improved, from 1985 to 1 October 2014. The invested capital number represents the total amount of public funds and privately managed capital assembled by an equity developer to deliver public services from publicly owned transportation projects. May large P3 projects are developed by a consortium of companies, which results in some double counting of projects between the firms listed here. It includes Ferrovial’s 2006 acquisition, upgrade and management of BAA’s UK airports, using a US$24.3 billion enterprise value.

Source: Public Works Financing.

The latest successes

The latest companies to do well abroad are Somague, a subsidiary of Sacyr, which is part of the consortium that won a €490 million contract to build part of the metro in São Paulo. This is Somague’s fourth contract for the city’s metro network. ACS, the world’s fourth-largest construction company, is to build and operate for 35 years a toll road in Portsmouth, Ohio. It beat off a US company and Spain’s Ferrovial to win the €435 million contract.ACS entered the US in 2006 and has projects worth around €7 billion. In Colombia, OHL was awarded the first toll road concession contract, and in Australia Acciona is part of the consortium for the Sydney light rail project.

The potentially most interesting development is that of Ferrovial, which launched this month a €680 million take-over bid for Transfield Services, the Australian outsourcing and construction services company that runs offshore immigration centres.Transfield rejected the offer, saying it did not reflect the underlying value of its shares.

The offer came a week after Ferrovial joined Macquarie of Australia to take over Glasgow, Aberdeen and Southampton airports in the UK from its partners in Heathrow Airport Holdings (HAH), previously called British Airports Authority (BAA). Ferrovial took control of BAA in 2006 and later reduced its stake to 25% in order to lower its debt load and strengthen its financial position at a time of recession in Spain. It is now on the acquisition trail again.

The move by Ferrovial, which previously held stakes in Sydney Airport, is part of an even more ambitious strategy to gain a foothold in China. Its bold venture, assuming it is successful, follows the acquisition by Spain’s ACS of Leighton Holdings, Australia’s biggest construction company, with a major share of the country’s market, covering commercial building and public and private infrastructure from desalination plants to road, rail and port projects. Ferrovial was part of one of the unsuccessful consortiums that tendered for Melbourne’s East West Link project, which was won by the one including Spain’s Acciona.

The Australian government appears keen to attract foreign companies to build projects, although its tender processes are longer and more expensive than European ones.

Conclusion: Spain has consolidated a notable and leading position in the world infrastructure market and there is every reason to believe it will go from strength to strength.

William Chislett

Associate Analyst at the Elcano Royal Institute and author of three books on Spain published by the Institute. Oxford University Press published his latest book on Spain in 2013 | @WilliamChislet3

[1] See España ‘goes global’.