Abstract

This paper explores the implications of the survival of the euro for the international monetary system (IMS). Since the outset of the euro zone (EZ) sovereign debt crisis in 2010, a new Berlin-Frankfurt axis is providing leadership in the creation of a banking union, a limited fiscal union and some form of economic and political union, all of which are necessary conditions for the survival of the euro. However, at the same time, this new hegemonic leadership is forcing a germanisation of all EZ peripheral economies (France included) as a prerequisite for granting them financial solidarity. If the process is completed, the EZ would become a more powerful actor in the IMS and its currency would be more attractive for international investors (the euro would no longer be seen as an orphan currency). However, it is unclear if this stronger EZ would be a stabilising or destabilising force for the IMS. On the one hand, a more ‘German’ euro-zone could have a structural current account surplus, and that could be deflationary and problematic, as it could trigger larger macroeconomic imbalances and put more pressure on the US, which will remain the main consumer of last resort unless China dramatically increases its internal demand. On the other hand, this reborn EZ will be much more inclined to regulate financial markets (following the ordoliberal German tradition) and, to some extent, to manage exchange rates, a goal shared by China and other emerging markets. Finally, it is unclear to what extent the EZ would be willing to politically promote the international role of the euro. All these elements will have important implications for the evolution of the IMS.

Introduction

Both the euro zone (EZ) and the International Monetary System (IMS) are in transition. The EZ is undergoing a substantial internal reform to ensure its sustainability, a process that started at the beginning of the sovereign debt crisis in Greece in 2010. This reform, which is proceeding gradually, includes the creation of a banking union, a limited fiscal union, a new role for the European Central Bank (ECB) and some form of economic and political union. The IMS is also facing the need to readjust to ensure that, in an increasingly multi polar world in which the US and the dollar are losing economic influence and political legitimacy, the system can function smoothly and facilitate liquidity, confidence and adjustment. This requires revising the functioning of the current unstable and dysfunctional flexible-dollar-standard (FDS), discussing the role of reserve assets, liquidity provisions and capital controls, reforming the International Monetary Fund’s (IMF) internal governance and designing new mechanisms to deal with global macroeconomic imbalances in order to ensure monetary stability.

Even though both processes run independently, they are closely interconnected because the EZ is, with the US and China, one of the three most influential actors of the IMS (it is the second-largest economic bloc after the US, it issues the second most-widely used reserve currency (the euro) and, when its member states coordinate their positions, it can dominate the decision-making process at the (IMF) and the G-20. Historically, however, the EZ has not played a preponderant role in international monetary and financial issues. It has left the leading role to the US. Since the breakdown of the Bretton Woods regime in the early 1970s until the creation of the euro in 1999, EU countries felt unable to substantially shape the evolution of the IMS. Once the euro was launched, EZ countries gained autonomy in international monetary affairs, but not necessarily influence, partly because the IMS was still dominated by the US and by an Anglo-Saxon approach to capitalism that was not dominant in continental Europe and partly because the EZ choose not to exercise monetary power at the international level (in fact, EZ countries never gave the euro a single voice in the international arena –Meuier & McNamara 2003– and they never used the single currency as a geopolitical instrument). Therefore, for decades, EZ countries have been punching below their weight in international monetary affairs. And none of them felt really uncomfortable with the status quo because their preferences and interests were, to a certain degree, compatible (albeit not coincident) with those of the US.

However, with the global financial crisis, the Great Recession and the subsequent EZ sovereign debt crisis, things are rapidly changing in Europe. And these changes might have profound implications for the functioning of the IMS. The EU, and especially the EZ, has embarked itself on a reform process to complete the ill-designed institutional architecture of the Economic and Monetary Union (EMU). A new Berlin-Frankfurt axis is leading the process and providing leadership in the creation of a banking union, a limited fiscal union and some form of economic and political union, all of which are necessary conditions for the survival of the euro. However, at the same time, this new hegemonic leadership is forcing a germanisation of all EZ peripheral economies (France included) as a prerequisite to granting them financial solidarity. In fact, the EZ has never witnessed a process of coordinated fiscal adjustment and structural reforms as intense as the one that is happening in southern Europe since the beginning of the crisis in 2010. And the process is likely to continue and deepen as austerity and reforms are the bargaining chip used by Germany to accept some sort of a transfer union. So far, the EU has made substantial progress: it has created a European Monetary Fund (the European Stability Mechanism, ESM); it has reformed EZ fiscal and macroeconomic governance with the Fiscal Compact, the ‘Six Pack’, the ‘Two Pack’ and the European Semester; it has set the guidelines to increase competitiveness through the ‘Euro Plus Pact’ and it has created the foundations of a Banking Union, that will start with a single supervisory and eventually include a crisis resolution mechanism and a common deposit insurance mechanism. Finally, since September 2012, the ECB has publicly stated that it will act as a lender of last resort when needed to ensure the survival of the euro and to make sure the transmission mechanism of monetary policy functions correctly.

The long term vision, as established by the paper presented by the President of the European Council Herman Van Rompuy (prepared in cooperation with the President of the Commission, the President of the Eurogroup and the President of the ECB and titled ‘Towards a genuine Economic and Monetary Union’),[2] has a specific sequencing that, starting with the single financial supervisory, would end with an institutional reform that opens the door for political union after 2014.[3] The final goal of the process is twofold. First, to complete the institutional architecture of EMU, which was designed in Maastricht, in order to make it a viable monetary union despite not being an optimal currency area (OCA). Secondly, to allow EZ countries to regain part of the economic sovereignty that they lost to the financial markets, thus making the European integration process more legitimate. As the ECB President Mario Dragi puts it:

‘Countries with high debt and deficits should understand they have lost sovereignty a long time ago over their economic policies in a globalised world. Working together in a stability-oriented union actually means to regain sovereignty at a higher level… sharing common rules for them actually means to regain sovereignty in a shared way rather than pretending to have sovereignty they’ve lost a long time ago. That’s the point’ (FT, 13/XII/2012).

The task will not be easy. Legitimising the process of European monetary integration requires presenting European citizens with a credible narrative about why painful reforms are necessary. Moreover, it requires generating economic growth and sustained prosperity, something that at the time of writing (March 2013) is far from happening. This paper, however, will not discuss this issue. It will assume, based on a number of qualified opinions (Bergsten, 2012; Bergsten & Kirkegaard, 2012; INET, 2012; Cohen, 2012; Butti & Pichelman, 2013), that the euro is too big to fail. This means that, difficult as it may seem, the reform process will move forwards, allowing the euro to survive and, in doing so, EZ fiscal, economic and political institutions will be strengthened. This will clearly make the euro more attractive for international investors because it will no longer be perceived as an orphan currency. However, as we will discuss in detail, the stronger and reborn euro will largely reflect German preferences. And this will have profound implications for the IMS.

This is precisely what this paper explores. It argues that, for the first time in the history of European integration, German economic and geopolitical preferences will dominate the EZ’s (and most likely the EU’s) foreign economic policies. And this change will present substantial challenges to the current IMS, which since the late 1970s has been largely dominated by an Anglo-Saxon approach to capitalism which is not fully shared by the economic and political elites in continental Europe. While it is unlikely that this new situation will trigger big conflicts in the IMS, tensions are likely to arise in the areas where German (and to a less extent French) ideas differ most from liberal Anglo-Saxon views: exchange-rate coordination, macroeconomic adjustment and financial-market regulation. Conversely, a reborn euro might facilitate the governance reform of the IMF because (limited) political union might lead to the consolidation of a single external voice for the euro, which could lead to a single representation for EZ countries at the IMF, and also at the G-20.

In order to understand how this process might came about, we will first analyse how the crisis has shifted the balance of power in the EZ from debtor to creditor countries, disproportionally increasing Germany’s relative influence within Europe. We will argue that Germany has become a regional hegemon, capable of exercising more ‘structural’ power than any other country in the history of the EU. However, Germany does not feel comfortable with this new scenario and it is not willing to provide some of the public goods that the EZ requires. Secondly, we will explore what Germany is trying to do with this newly acquired power. In particular, we will analyse how it is taking advantage of its privileged position to not only obtain short-term economic and financial benefits but also to push for reforms that will incorporate specific features of the German ordoliberal model of capitalism (Bonefeld, 2012) in other EZ countries. The core of the paper will be dedicated to speculate about how this new EZ could try to shape the reform of the IMS.

First, we will argue that if the euro survives, its international use will grow, but that Germany (and thus the EZ) will be reluctant to exercise leadership in the IMS or take full advantage of the monetary power associated to issuing a leading reserve currency. This is due to the fact that a Germanised EZ might adopt a geo-economic and neo-mercantilist economic strategy based primarily on export-led growth which might not be compatible with the high levels of exchange rate volatility associated with issuing the dominant international reserve currency.

Secondly, and connected to the previous point, due to the structural reforms in southern Europe, the EZ could have a structural current-account surplus. This would exacerbate the problem of global macroeconomic imbalances and create deflationary pressures in the world economy, thus putting more pressure on the US, which will remain the principal consumer of last resort unless China dramatically increases its internal demand. Should this happen, the classical political economy question ‘who adjusts?’ could cause significant tensions in the IMS.

Finally, the EZ will be much more inclined than in the past to intervene in the international foreign exchange and financial markets according to the ordoliberal model of capitalism prevailing in German, which exhibits features of a coordinated market economy substantially different from the Anglo-Saxon liberal market economic model (Bonefeld, 2012; Duillen & Guerot, 2012). This could mean that the EZ could be inclined to manage exchange rates (a goal shared by China and other emerging markets but not by the US or the UK) and to strongly regulate the international financial markets, even promoting the establishment of an international financial transaction tax.

In sum, a reborn EZ will have more international monetary power, but it is unclear if it will be a stabilising or a destabilising force for the IMS.

A new Union of creditors and debtors

For half a century, the EU has been a political project underpinned by solidarity and confidence. Rich northern countries were willing to show a remarkable level of solidarity with their less well-off southern neighbours in a combination of perceived self-interest and trust in them. Peripheral countries that had emerged from authoritarian regimes used their EU membership to consolidate their democracies and promote economic growth. This, in turn, gave rise to large and stable markets for the core-countries’ exports. It was a win-win situation. Northern solidarity paid off because the countries in the south generally behaved as expected. It was an EU dominated by a balanced Franco-German axis. There was no hegemonic power, but a division of labour in which France’s strategic vision and Germany’s economic power were compatible and facilitated progress towards deeper integration.

However, the EZ debt crisis has dramatically changed the nature of European integration. The combination of poor financial regulation and an incomplete design of the euro have led the EMU to the brink of collapse, forcing the EZ to move forwards decisively in order to avoid catastrophe. However, the institutional changes that the EZ has been implementing since 2010 to convince the markets that the euro is an irreversible project do not have the same underlying logic as in previous steps towards integration. Northern creditor countries, led by Germany, have increased their bargaining power vis a vis southern countries, creating a new decision-making process in Europe in which creditors set the rules and debtors have little option but to follow what the north dictates. They have become ‘decision takers’. In fact, the ‘community method’ has been weakened and a new asymmetric intergovernmentalism has emerged, in which a hegemonic Germany sets the direction, timing, speed and scope of reforms with little or no counterweights.

This can be seen in the negotiations on the German-sponsored Fiscal Compact (which constitutionalises the German debt brake and reduces the scope for fiscal discretion), the banking union (in which limited supervision has prevailed over a common resolution regime or a common insurance deposit guarantee system, essentially reflecting German interests), the ESFS/ESM (which is arguably too small and too inflexible, again reflecting Germany’s goal of providing only the minimum level of solidarity required to avoid a EZ collapse) and the ‘six pack’ and ‘two pack’ negotiations, in which, for instance, Germany has dictated that the macroeconomic imbalances procedure will not be symmetric (ie, large current account deficits are considered to be ‘more dangerous’ than large current account surpluses).

Similarly, Germany has so far kept out of the negotiating agenda free proposals which would have satisfied the preferences of the Mediterranean countries (France included), such as a partial mutualisation of debt (in the form of Eurobonds or a Redemption Fund), a larger EU budget to deal with asymmetric shocks, a comprehensive growth programme at the EZ level and a strategy to deal with legacy assets in the financial system.

Finally, the ECB’s reluctance to intervene on a continuous basis in the debt markets to reduce financing costs for the EZ’s periphery (at least until September 2011 when it launched its OMT programme) has forced these countries to adopt austerity measures and implement structural reforms in order to be able to raise money in the international markets. In fact, the EZ has never witnessed a process of coordinated fiscal adjustment and structural reforms as intense as the one that is currently taking place in southern Europe since the beginning of the crisis in 2010. And the process is likely to continue and deepen as austerity and reforms are the bargaining chip used by Germany to accept some sort of a transfer union in the long run.

In sum, the old Franco-German axis has been replaced by a Berlin-Frankfurt axis, which is Germanising the south’s economies through austerity and structural reforms and, at the same time, is creating a new governance framework for the EZ, which is essentially an extension of the German view of capitalism. This is not the first time that Germany has tried this. As Fernández-Villaverde, Garicano & Santos (2013) argue, the creation of the euro itself had as one of its goals promoting supply-side structural reforms in southern Europe. By eliminating the possibility of devaluing their currencies to solve competitiveness and growth problems, countries will have more incentives to reform their labour and product markets and to improve their education systems. Unfortunately, and quite unexpectedly, the opposite occurred. Peripheral countries experienced an investment boom that created exactly the wrong incentives for reform.

To underpin, justify and legitimise its actions, Germany has recently created a narrative of the crisis according to which the EZ’s problems are mainly the result of profligacy and competitiveness losses in the south, not of an ill-designed EZ or the global financial crisis. According to this diagnosis, the solution to the crisis, given that it is too risky for the EU to break up the euro and too costly for Germany to exit, is to force the southern European economies to adopt certain features of the German socio-economic model (and to provide them with limited assistance in cases of market turmoil). In particular, Germany’s own reforms in the 2000s, which made its economy more flexible and competitive, appear, combined with austerity, as the blueprint for reforms in the south.

Therefore, not only is Germany more powerful in relational terms than any other country has been in Europe since World War II, it is also acquiring structural power, as defined by Strange (1988), by disseminating its own ideas about what is the best strategy to exit the crisis.[4] So far, it has not completely succeeded. Alternative narratives of the crisis still exist (European Commission, 2012; INET, 2012; Moravcsik, 2012). However, once Germany has realised that it is trapped in the euro (which has also benefited its export-oriented sector enormously), it has been trying to use the crisis as an opportunity to radically transform the economic structure of southern EZ members by forcing the adoption of rules that will reduce the policy space for implementing policies that are divergent from the Coordinated Market Economy/Ordoliberal model predominant in Germany.[5] Therefore, austerity, limited solidarity, reluctance to accept higher levels of inflation and labour market reforms are instruments to attain its goals and consolidate its incipient structural power.

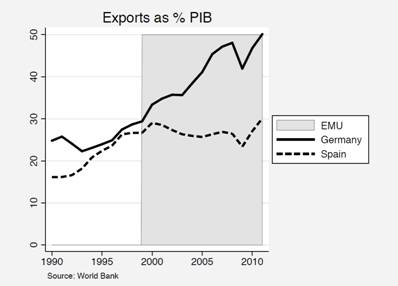

In fact, as Vermeiren (2012) shows, the original design of EMU allowed Germany to increase its monetary power because of the nature of its CME even before the EZ crisis started. In particular, German’s flexible labour market and export-oriented economy (with a comparative advantage in goods and services that do not compete primarily in price), allowed Berlin to reap more gains from EMU than southern European countries. As Graph 1 shows, German exports (as a percentage of GDP) grew dramatically with the introduction of the euro, while Spanish exports fell.

Graph 1. German and Spanish trade openness before and after the EMU

This, in turn generated large intra EZ macroeconomic imbalances, with Germany emerging as the main creditor country and Spain, Greece, Ireland and Portugal as debtors (Graph 2). When the debt crisis started, southern European countries realised that they were in a week bargaining position and Germany was able to increase its influence.

Graph 2. Net international investment position as a % of GDP

In addition, besides this long term strategy, Germany has tactically used the economic problems of the periphery to obtain short-term advantages and to preserve its financial interests. First, financial instability in southern Europe has reduced Germany’s own financing costs because of the capital flight from the periphery to the core (Merler & Pisani-Ferry, 2012). In fact, Germany, just like the US, is now enjoying the ‘exorbitant privilege’ of issuing the safest debt of the EZ, but, unlike the US, is unwilling to provide sufficient public goods for Europe. Secondly, Germany, as the largest creditor country, has consistently refused to accept inflation to facilitate deleveraging and has set the timing and the conditions of the Greek debt restructuring, thus preserving its financial interests. Finally, and related to the previous point, it has not tried to reverse the appreciation of the euro despite the damage that the strong currency does to southern European countries’ exports (especially Italy, Portugal and France), because an appreciated euro does not damage the competitiveness of German exports due to the high value-added nature of the goods and services it sells outside the EZ.

How would a Germanised Europe affect the IMS?

Although every EZ country will maintain its idiosyncratic characteristics, if the structural reforms across Europe continue (particularly in the labour markets, product markets, financial markets, taxation and pensions) and if the EZ manages to increase its level of financial, fiscal, economic and political integration, there would be important implications for the IMS. We will devote the rest of the paper to speculate on them.

A strong and more attractive euro, but not a reserve currency

So far, the euro has been no rival for the dollar. Despite having emerged as the second most used international currency worldwide, it has a number of structural limitations: economic factors such as insufficient financial integration and lack of liquidity in its debt markets, political shortcomings related to having a monetary union without a fiscal and political union, and limited European military ambitions (Cohen, 2010; Eichengreen, 2011, Otero-Iglesias & Steinberg, 2012).

The ‘military’ factor is unlikely to change in the foreseeable future. Budget cuts in Europe are undermining military spending and the EU still relies on the US and NATO for its basic security. However, as mentioned above, the EZ debt crisis has triggered a radical transformation in the governance institutions that underpin the euro. It has also opened the door for the creation of some sort of Eurobonds/euro bills, which could eventually make the European financial markets deeper, wider, and more liquid.[6] In fact, as Otero-Iglesias & Steinberg (2012) show, financial elites in key dollar-holding countries would be willing to buy large quantities of euro-denominated assets to diversify away from the dollar if the EZ were to issue a debt instrument comparable to the US 10-year T-bill and if the euro had a fiscal and economic union to ensure its long-term sustainability.

Therefore, it could be argued that, from a purely economic perspective, the euro could increase its role as a reserve currency if it consolidates its banking and fiscal union and ends up issuing some sort of common debt instrument. And it will most likely do so, as these reforms are deemed necessary for its survival.

The question, however, is, to what extent European authorities would be willing to politically promote the international role of the euro. This is relevant because a currency can only become the top international currency if there is an active political commitment by the issuing authorities (Eichengreen, 2011). And, so far, only the US in the 20th Century and the UK (in the previous century) had been willing to do so. Using Cohen’s (2006) definition of monetary power, it is clear that the consolidation of the euro has (and will) give the EZ more autonomy in international monetary affairs. But will it give it more influence? That largely depends on the balance of power within the EZ and thus on German political preferences.

Issuing an international reserve currency has both costs and benefits (Cohen 2010). The benefits include flexibility in macroeconomic policy, increased revenues from seigniorage and greater political influence in the international arena. Costs, however, are related to the fact that the issuer of an international currency faces the risks of imported inflation and competitiveness losses due to currency revaluation. This means that countries may choose not to promote the internationalisation of their monies. This was the case with the Deutschmark (Marsh, 1992) and the Japanese Yen (Grimes, 2003), and, to a certain extent, is also the case with the euro today. The ECB remains officially agnostic on the internationalisation of the euro and European leaders have traditionally had different views. French officials have often expressed their interest in consolidating the euro as a serious rival to the dollar, while Germany has tended to have a lower profile, rarely including geopolitical considerations in its currency discourse, which stresses above all macroeconomic stability and low inflation.[7]

Therefore, if a stronger Berlin allows the German positions to prevail, it is unlikely that the EZ engages in a strategy to politically promote the internationalisation of the euro. Market forces may well increase the appeal of the European currency, especially if the ECB maintains its anti-inflationary stance and if Eurobonds markets are created (and also if the US continues implementing ultra expansionary monetary policies that exert a structural pressure towards the depreciation of the dollar). However, without German willingness to exercise monetary power internationally, the euro will, most likely, remain a secondary international currency, probably competing with the RMB in the medium term.

The EZ in structural current account surplus

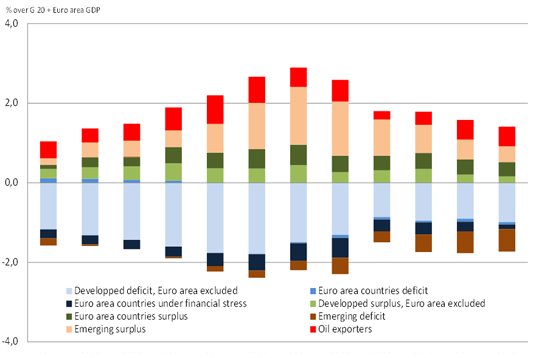

Global macroeconomic imbalances have been a persistent problem of the IMS in the last decade. Excess savings in China, Japan, Germany, oil-exporting countries and some other emerging powers in Asia and excess spending in the US, the UK and the peripheral EZ countries were, together with financial deregulation, key causes of the global financial crisis (Wolf, 2010; Rajan, 2010).[8]

The 2008-09 Great Recession helped to correct global imbalances mainly by reducing imports in deficit countries. However, since 2010, these imbalances have reappeared (Graph 3). Although China is rapidly reducing its current account surplus and most advanced countries that used to have large deficits are cutting them, the IMF still projects that imbalances will be between 1.5% and 2% of world GDP by 2016 (IMF, 2012, p. 25). The US and China have been the most vocal powers in criticising the status quo, sometimes called Bretton Woods II, but for different reasons. The US complains about China’s exchange rate policy and China claims that irresponsible expansionary monetary and fiscal US policies represent a risk to global stability and to their dollar-denominated assets. Nevertheless, both countries seem to be comfortable with the current situation and have not taken rhetorical confrontation further (the US has not introduced unilateral protectionist measures and China has not sold its dollar-denominated assets).

Graph 3. Global Macroeconomic Imbalances

So far, the EZ has not participated in this debate. At the G-20 meetings it has insisted that China should revalue the RMB, but with much less emphasis than the US. Since its creation, the EZ has had a balanced current account because the external surplus of ‘northern’ countries was compensated by the external financing needs of the countries in the periphery (in fact, Germany is the only large country in the world that has not contributed to global rebalancing). EZ countries have always resisted a discussion in the G-20 about intra EZ macroeconomic imbalances because they consider this issue internal (just like healthcare reform in the US) and have defended that the EZ has not contributed to global imbalances. This, however, is rapidly changing. While Germany and its northern neighbours are expected to maintain large surpluses, structural reforms in southern countries are likely to generate external surpluses in these traditional deficit countries as well.

For instance, Spain, which ran a current account deficit of over 10% of GDP in 2007, is expected to move to a surplus in 2013. Overall, the European Commission projects a current account surplus for the EZ of more than €250 billion (around 2% of the EZ’s GDP), a surplus larger than China’s.

Graph 4. Current account imbalances in the euro area

The implications for the IMS of an EZ in structural external surplus would be remarkable. Should that happen, and if China and Japan do not begin to run current account deficits (something that is not likely to happen soon), the global economy will have all of its major economic blocs except the US trying to lend to the rest of the world. So the question will inevitably become: who is the buyer? Either the US consumer re-emerges once again as the world’s consumer of last resort, or the world economy would have to accept slower economic growth and deflationary tensions. But as the Great Depression of the 1930s and the long deflation in Japan in the 1990s show, declining prices in an environment of high debt could increase the problems of the financial sector in advanced countries and drag down economic growth even more. In that scenario geopolitical tensions are likely to increase, with currency wars, rising protectionism and redistributive conflicts between debtor and creditor countries becoming more acute. In particular, there could be growing tensions between the US and the EZ, which have traditionally cooperated in international monetary issues. Finally, a EZ behaving more ‘like China’ could open the door to more exchange rate and regulatory cooperation between the EZ, China and the other BRICS countries. We explore these issues in the following section.

A more interventionist EZ in the IMS?

One of the key philosophical differences between the Anglo-Saxon model of capitalism and that prevalent in continental Europe is its trust in markets. Both views agree that the free market economy is the best way to generate innovation and growth. However, for liberal Anglo-Saxons, markets tend to be self-stabilising and relatively well self-regulated, requiring only small doses of government intervention (domestically, these views correspond to the liberal market economies of the varieties of capitalism literature –Hall & Soskice 2001–). To the contrary, continental Europeans tend to believe that markets should be more heavily regulated in order to generate adequate (and legitimate) outcomes. Specifically, in the German ordoliberal tradition, the free market economy requires the existence of a ‘strong state’ (‘a state that restrains competition and secures the social and ideological preconditions of economic liberty’ –Bonefeld, 2012, p. 1–). Thus, there is an emphasis on the need for rules and coordination to avoid adverse market outcomes that could eventually delegitimise the system, which correspond to the Coordinated Market Economies within the varieties of capitalism literature. This view, to a certain extent, is shared by other continental European countries (especially France) and with a number of varieties of so-called State Capitalism that prevail in some emerging powers.

Before the global financial crisis, the Anglo-Saxon view of capitalism was dominant, especially in the western world. However, the severity of the crisis and of the Great Recession (2008-10) has triggered an ideological shift in favour of more regulated markets (Rodrik, 2011). As a result, the international community has been trying to establish new rules and enhanced coordination mechanisms to improve the functioning of the international markets, especially in the areas of money and finance. Besides the financial reform implemented in the US and in some European countries (which aim to improve and extend regulation), the IMF has accepted the use of some forms of capital controls, the EU has established an international financial transactions tax and has banned short-selling temporarily, and the Bassel III accord has increased capital requirements for banks. In emerging markets, neo-mercantilist strategies are becoming more common and they even seem to have gained legitimacy because of their capacity to generate relatively successful economic outcomes. It is still early to know to what extent these new forms of regulation are moving the world economy towards deglobalisation. What is clear, however, is that in the realm of ideas the German view of Capitalism is gaining influence vis à vis the Anglo-Saxon model, and this could have important implications for the IMS in the coming decades.

First, in the area of exchange-rate coordination, the world economy could witness a higher degree of cooperation to manage exchange rates. There have been numerous recent proposals to introduce some level of exchange rate coordination (Mundell, 2005; Padoa-Schioppa, 2010; Camdessus et al., 2011; United Nations, 2009). However, they have usually been rejected by the US, which is comfortable with the current regime, where the status of the dollar and the flexibility of exchange rates allow it to use its monetary power. Emerging markets from China to Brazil, on the other hand, have repeatedly called for more coordination to avoid the adverse externalities of American macroeconomic policies (Zhou, 2009). In Europe (and especially in France) there has been remarkable sympathy for the idea of coordinating exchange rates (Otero-Iglesias & Zhang, 2012), a view not always shared by Germany, which considers that coordination should not undermine the independence of the ECB. However, as discussed earlier, the EZ has never had a strong position on the issue, in part due to the EZ’s institutional weaknesses. Should this change in the future, the EZ could come closer to the position of the emerging markets, thus leaving the US with limited allies (only the UK) to resist changes in the IMS that include more monetary cooperation. And even if the EZ does not align itself with the emerging markets on this issue, the eventual creation of an EZ chair at the IMF (something that could well happen in the foreseeable future should the EZ move towards some form of political union) could greatly increase European influence in shaping the future IMS.

Secondly, in the area of financial regulation, EZ countries have repeatedly shown their intention of curtailing the markets. In fact, after failing to convince the other members of the G-20 to pass an international financial transactions tax, they decided to implement it on the European Continent in 2012. And in the broader area of financial regulation, EZ cooperation with some emerging markets that also seem to distrust the risks involved in sophisticated financial derivates or excessively lax forms of control for portfolio investments, could improve. This could also trigger confrontation with the US and the UK.

Conclusions

This paper has argued that the transformation that the EZ is experiencing as a result of the debt crisis could radically transform the balance of power in the IMS. The European debt crisis has created a new EU of debtors and creditors in which a new Berlin-Frankfurt axis has partially replaced the old (and more balanced) Paris-Berlin axis. Germany has thus emerged as a hegemonic power in the EZ, and it is using its newly acquired power to establish a new rules-based system of European economic governance that, if fully implemented, would Germanise the economies of southern Europe. Germany, however, does not feel fully comfortable with its new role. Since the creation of the European Economic Community in the late 1950s Germany has always preferred to ‘hide’ behind Europe than to lead it. But it has realised that the current financial instability in the EZ provides an opportunity to force politically difficult reforms onto southern Europe, reforms that it thinks are indispensable to ensure the success of the EZ in a global economy in which emerging markets exert a greater competition in a declining west. Therefore, it has assumed a (temporarily) new leadership role whose main goal is to establish a set of (irreversible) new governance rules that restrict the political space of EZ governments to pursue policies which Germany considers damaging for the strength of the European economy in the world. These rules, which have been proposed by the European Commission and in which the European Parliament has also been involved, reflect –however– the new balance of power within the EZ: southern European countries have not been able to shape them as much as creditor countries. As a result, the Fiscal Compact, the Six Pack and the Two Pack, the intergovernmental ESM and the timing and sequencing of the Banking Union all reflect mainly German preferences. It remains to be seen if –after these new rules are in place, the EZ moves towards deeper economic integration in the fiscal, financial and economic spheres, and the deep recession in southern Europe ends– Germany decides to take a step back and abandons its attitude of explicit leadership or not. However, even if it does, it would still be able to exercise structural power if its economic ideas become embedded in new EZ rules and institutions.

The second part of this paper has been devoted to speculating about the implications of a reborn and Germanised EZ in the IMS. We have argued that it is unclear whether the role of the EZ would provide more or less stability. On the one hand, a greater internationalisation of the euro (which would be based on market decisions and not on an explicitly political support of the European currencies by European authorities) could facilitate the emergence of a competitive multicurrency IMS, which could provide more stability than the current flexible-dollar standard. On the other hand, a Germanised EZ could have a structural current account surplus that could exert a deflationary pressure in the global economy. This, in turn, could trigger transatlantic confrontation and open the door for cooperation between the EZ and some emerging markets in specific issues, like global financial regulation or some sort of exchange-rate coordination.

Federico Steinberg, Senior Analyst for International Economics, Elcano Royal Institute.

References

Bergsten, Fred (2012), ‘Why the euro will survive’, Foreign Affairs, Sept/Oct.

Bergsten, Fred, & Jacob Funk Kirkegaard (2012), ‘The Coming Resolution of the European Crisis’, Petersen Institute for International Economics Policy Brief, PB 12-1.

Blyth, Mark (2013), Austerity. The History of a Dangerous Idea, Oxford University Press.

Bonefeld, Werner (2012), ‘Freedom and the Strong State: On German Ordoliberalism’, New Political Economy, vol. 17, nr 5.

Butti, Marco, & Karl Pichelman (2013), ‘European prosperity reloaded: an optimistic glance at EMU@20’, ECFIN Economic Brief, nr 19, European Commission.

Camdessus, Michel, et al. (2011), Reform of the International Monetary System: A Cooperative Approach for the Twenty First Century, Palais Royal Initiative, Paris, 18/I/2011.

Cohen, Benjamin (2012), ‘The future of the euro: Let’s get real’, Review of International Political Economy.

Cohen, Benjamin (2010), The Future of Global Currency: The Euro Versus the Dollar, Routledge, London.

Cohen, Benjamin (2006), ‘The Macrofoundations of Monetary Power’, in D.M. Andrews (Ed.), International Monetary Power,Cornell University Press, p. 31-50.

Dullien, Sebastian, & José Ignacio Torreblanca (2012), ‘What is the Political Union?’, ECFR, Policy Brief, nr 70, December.

Duillen, Sebastian, & Ulrike Guerot (2012), ‘The Long Shadow of Ordoliberalism’, ECFR, Policy Brief, nr 49.

Eichengreen, Barry (2011), Exorbitant Privilege: The Rise and Fall of the Dollar, Oxford University Press, Oxford and New York.

Fernández Villaverde, Jesús, Luis Garicano & Tano Santos (2013), ‘Political Credit Cycles: The Case of the Eurozone’, Journal of Economic Perspectives, forthcoming.

Grimes, W.W. (2003), ‘Internationalization of the Yen and the New politics of Monetary Insulation’, in J. Kirshner (Ed.), Monetary Orders. Ambiguous Economics, Ubiquitous Politics, Cornell University Press, Ithaca and London, p. 174-195.

Hall, Peter, & David Soskice (Eds.) (2001), Varieties of Capitalism, Oxford University Press, Oxford.

Hancke, Bob, Martik Rhodes & Mark Thatcher (Eds.) (2007), Beyond Varieties of Capitalism: Conflict, Contradictions, and Complementarities in the European Economy, Oxford University Press, Oxford.

IMF (2012), World Economic Outlook, Washington DC.

INET COUNCIL ON THE EURO ZONE CRISIS (2012), Breaking the Deadlock: A Path Out of the Crisis, Institute For New Economic Thinking.

Kirshner, J. (Ed.) (2003), Monetary Orders. Ambiguous Economics, Ubiquitous Politics, Cornell University Press, Ithaca and London.

McNamara, K.R., & S. Meunier (2002), “Between national sovereignty and international power: what external voice for the euro?’, International Affairs, vol. 78, nr 4, p. 849-868.

Marsh, D. (1992), The Bundesbank – The Bank that Rules Europe, Heinemann, London.

Merler, Silvia, & Jean Pisani-Ferry (2012), ‘Sudden Stops in the Euro Area’, Bruegel Policy Contribution, nr 2012/06, March.

Moravcsik, Andrew (2012), ‘Europe After the Crisis. How to Sustain a Common Currency’, Foreign Affairs, May/June.

Mundell, R. (2005), ‘The case for a world currency’, Journal of Policy Modelling, nr 27, p. 465-475.

Otero-Iglesias, M., & M. Zhang (2012), ‘EU-China Collaboration in the Reform of the International Monetary System: Much Ado About Nothing?’, Working Paper, nr 2012W07, Research Center for International Finance, Chinese Academy of Social Sciences, Beijing, 27/IV/2012.

Padoa-Schioppa, T. (2010), ‘The Ghost of Bancor: The Economic Crisis and Global Monetary Disorder’, Louvain-la-Neuve, 25/II/2010.

Rajan, Raghuram, G. (2010), Fault Lines: How Hidden Fractures Still Threaten the World Economy, Princeton University Press.

Rodrik, Dani (2011), The Globalization Paradox Democracy and the Future of the World Economy, Oxford University Press.

Steinberg, Federico, & Miguel Otero-Iglesias (2013), ‘Reframing the Euro vs. Dollar Debate through the Perceptions of Financial Elites in Key Dollar-Holding Countries’, Review of International Political Economy, vol. 20, nr 1, February, p. 180-214.

Sapir, André, et al. (2011), ‘What Kind of Fiscal Union’, Bruegel Policy Brief, November.

Strange, Susan (1996), The Retreat of the State: The Diffusion of Power in the World Economy, Continuum, New York.

United Nations (2009), Preliminary Report of the Commission of Experts on Reforms of the International Monetary and Financial System, New York, United Nations, May.

Wolf, Martin (2010), Fixing Global Finance, 2nd Edition, Johns Hopkins University Press & Yale University Press, Washington DC and London.

Zhou, X. (2009), ‘Reform of the International Monetary System’, People’s Bank of China, Beijing, 23/III/2009.

[1] This paper was prepared for the Workshop ‘The future of the International Monetary System’, Ghent, Belgium, March 2013.

[2] Available at: www.consilium.europa.eu/uedocs/cms_data/docs/pressdata/en/ec/134069.pdf.

[3] For a debate on the problems of this process, especially with the issue of political union see Dullien & Torreblanca (2012).

[4] ‘Structural power in short confers the power to decide how things shall be done, the power to shape frameworks within which states relate to each other, relate to people, or relate to corporate enterprises’ (Strange, 1988).

[5] For a discussion of the different models of capitalism see Hall & Soskice (2001) and Hanke et al. (2007). See Vermeiren (2012) for an application of this literature to the distribution of power within Europe after the creation of the euro. For an updated version of the peculiarities of the German-Ordoliberal model of capitalism and its implications for the EZ crisis see Bonefeld (2012) and Duillen & Guerot (2012).

[6] Debt issued by the ESM can be considered pseudo eurobonds. However, so far the ESM has issued relatively small quantities of assets and some doubts about ESM governance and guarantees preclude it from becoming a liquid and well-understood instrument.

[7] There is also an ongoing debate regarding the value of the euro’s Exchange rate, in which France (and Italy) tend to complain about the strength of the euro in the context of current currency wars, while Germany maintains silence and tries to protect the ECB’s Independence.

[8] Low interest rates in the US and excess savings in emerging countries gave rise to a glut of liquidity that ended up generating a bubble in the asset markets, which was also fed by financial deregulation and the creation of new financial instruments.