Theme

It is important to describe current and future Spanish energy policy decisions in order to assess a set of policy pathways for Spain’s energy transition.

Summary

This paper describes and quantifies three different energy policy pathways for Spain’s energy transition: government-centred, represented by the socialist party (Partido Socialista Obrero Español, PSOE); market-centred, represented by the conservative party (Partido Popular, PP); and grassroots, represented by Unidas Podemos.

Analysis

A recent MUSTEC, H2020 report1 describes the Policy pathways for the energy transition in Europe and selected European countries. It analyses current and potential future policy decisions in Germany, France, Spain, Italy, Switzerland and the European Commission, bundling them into sets of policy pathways that describe the energy transition trajectories of countries and the EU as a whole. Each pathway is centred around a certain logic: a worldview, or belief, about the type of policies that are (to its proponents) acceptable and beneficial, leading to a distinct type of electricity (and energy) future.

The paper takes the future as given. Current, past or future policy decisions may or may not be cost-optimal, or even useful, but we assume they are implemented, as the dominant political force in Spain (which, depending on the pathway, is the PSOE, PP or Unidas Podemos, respectively) deems it appropriate at a point in time. These pathways depend both on hard facts and ideological factors which are exogenous to the energy system (eg, fundamental views on market vs state, economic efficiency vs equity, etc). Because there are so many possible decisions, there are theoretically a myriad of decarbonisation pathways that could materialise between today (2019) and 2030, 2040 or 2050. In order to produce a meaningful and manageable analysis, it is key to reduce the number of possible energy-policy pathways.

This paper describes and quantifies three different energy policy pathways for Spain’s energy transition: a government-centred pathway represented by the PSOE, a market-centred pathway represented by the PP and a grassroots pathway represented by Unidas Podemos. There are for sure other political parties in Spain with interesting energy worldviews to analyse, but it could be argued that the selected ones are representative of the energy transition policy space. Additionally, PP, PSOE and Unidas Podemos have prepared law proposals,2 allowing a better specification and quantification of their pathways.

Each of the three decarbonisation pathways (government-centred, market-centred and grassroots) can include elements that would theoretically fall within two other decarbonisation pathways. For instance, the new socialist government’s Climate Change and Energy Transition Law proposal includes bidding and other market mechanisms but, on the whole, it tends to assume energy transition requires tough, mandatory measures such as phase-outs, deadlines, bans and ambitious targets. Similarly, Unidas Podemos sets the most ambitious decarbonisation targets and argues for state (and local) intervention, but its key differentiating factor lies in its grassroots-centred logic, focused on small-scale and local action, seeking decarbonisation through decentralisation of the energy system. Finally, the Popular Party self-stated market-centred logic is based on carbon pricing and letting the market identify the most cost-efficient way to meet energy and climate targets.

Nevertheless, the following pathways represent consistent, clear and the best specified set of alternatives for Spain’s energy transition. Their implicit strategies are presented as ‘narratives’ or ‘scripts’.3 They tell the story from the perspective of 2050, ie, looking back, of how medium and long-term decarbonisation targets were (hypothetically) reached through different means and policy measures, depending on the pathway Spain took (using the past tense, ie, as if they had materialised according to the draft legislative proposals of each of the parties). The three pathways are also presented in a quantitative manner with the support of their respective tables, with the dominant (government-centred) pathway including the key elements of Spain’s draft Integrated National Energy and Climate Plan (INECP) presented to the EC in February 2019.

The State-centred pathway: Partido Socialista Obrero Español(PSOE)

By 2050 Spain had achieved net-zero emissions, both economy-wide and, in particular, in the electricity sector, which was fully renewable. The government’s ‘Target Scenario’ materialised as envisaged in the INECP for 2021-30. The INECP operationalised the long-awaited Climate Change and Energy Transition Law that was finally approved in 2020, along with the development of a Long-Term Strategy and a Just Transition Strategy.

Several international and domestic factors drove Spain’s shift to a lower carbon development model. These included: (1) the entry into force and ambitious implementation of the Paris Agreement; (2) the adoption of increasingly stringent targets for renewables and energy efficiency in the EU; (3) the implementation of the EU’s Long-Term Strategy, that set out to achieve net-zero emissions by 2050; (4) the continued reduction in the cost of renewable energy technologies; (5) the banning (in sales and registration) by 2040 of internal combustion engine (ICE) vehicles in Spain’s main car markets (eg, the UK and France); and (6) an increasing concern for climate-change impacts by Spanish citizens, who ranked climate change as the top foreign-policy priority concern from 2016 onwards.4

A set of laws and policy measures guided the radical decarbonisation of the electricity sector, and of society as a whole, under tight government control. For the power system, this included decisions such as an orderly phase-out of nuclear power between 2025 and 2035, the phase-out of coal by 2030,5 a ban on new fossil fuel subsidies6 from 2020 onwards, the centrally planned phase-out of existing fossil-fuel subsidies, the banning of internal combustion engines in cars, mandatory low-emission zones in municipalities and mandatory renovations and building retrofitting.

By 2030 Spain’s economy had reduced its GHG emissions by 21% compared with 1990 levels. By 2050 Spain’s GHG emissions were 90% lower than 1990 levels, with the remaining 10% being offset by Spain’s carbon sinks, making the Spanish economy carbon neutral by mid-century, in alignment with the INECP and with the Spanish Climate Change and Energy Transition Law.

Overall, Spain’s INECP was initially considered very ambitious, even too ambitious for some energy and emission intensive sectors, as the implementation of Spain’s INECP meant a reduction of over a third of Spain’s 2017 emissions in little over a decade, an unprecedented decarbonisation effort for Spain. The INECP was, however, criticised by other sectors (mainly Civil Society Organisations, CSOs)7 as showing limited ambition compared to other EU countries that adopted more stringent emission reduction targets.8 Although the government initially set out to reduce its GHG emissions by 40% compared with 1990 levels by 2030, which would have aligned its ambition with most EU countries, it scaled down its ambition and settled for a 21% goal in its INECP, arguing it was a fair, achievable and balanced goal.

By 2030, the INECP’s 42% renewable energy target was achieved in Spain’s final energy consumption, supported by an electricity system that was largely renewable (74% of the electricity consumed in Spain). Among other measures, the objective was met through a steady stream of auctions that added at least 3,000 MW of new renewable capacity annually between 2019 and 2030. Throughout the 2021-30 period, 57,000 MW of new renewable capacity was added to the system, supported by auctions. Solar and wind were the bulk of the auctioned power between 2019 and 2030. During this decade, 5 GW of concentrated solar power (CSP) were auctioned and constructed, restarting the expansion of this technology in Europe.

The overall target for renewable capacity installed in Spain was determined by the INECP. The government took a technology-neutral approach to decarbonisation but the ‘Target Scenario’ materialised by 2030. That scenario considered the expected evolution in technologies and costs and strived for a cost-efficient realisation of the decarbonisation pathways. In the ‘Target Scenario’ Spain’s 157 GW of installed power capacity included, among other issues, 50 GW of wind, 44 GW of solar (37 GW of solar PV and 7 GW were CSP),9 27 GW were combined gas cycles, 16 GW were hydro, just under 7 GW of pumped hydro, 2 GW of oil and 3 GW were nuclear.10 The INECP envisaged a very significant uptake of renewables so integrating them into the system was key. In order to achieve integration, demand-side management measures were fostered to change consumption patterns. Additionally, storage capacity was increased, adding 3.5 GW of pumped storage and 2.5 GW of storage capacity in batteries.11

By 2050 Spain’s power sector was fully (100%) renewable. After the Climate Change and Energy Transition Law was approved in 2020, the integration of renewables in the power system continued to be supported by the Spanish government through priority dispatch, subject to the requirements and limitations enshrined in the Energy Union regulations.

Most new fossil fuel subsidies12 were banned by the Spanish government as of 2020. Given, amongst others, energy poverty problems, the government introduced Article 9 in the Climate Change and Energy Transition Law, allowing new fossil subsidies if justified on social grounds, to protect Spain’s economic interests or due to the lack of adequate technological alternatives.13 Initial concerns regarding these exemptions to new fossil fuels were assuaged as a robust control mechanism was put in place by the Spanish government to prevent loopholes through which undue subsidies could have been granted. Existing subsidies (consisting of tax exemptions and deductions) in 2017 (amounting to €2.3 billion for oil, €756 million for gas and €2.9 million for coal)14 were progressively phased out following the government’s calendar to do so. New exploration and extraction of hydrocarbons by conventional and new techniques such as hydraulic fracturing were also banned in Spain as of 2020. Existing permits for exploration and extraction of hydrocarbons were not extended.

Half of Spain’s coal power15 was phased out by 2020, with the rest having been phased out completely by 2030. Nine out of the 15 coal power plants in Spain were already closed in 2021 as the necessary adaptions to limit atmospheric emissions to comply with the Industrial Emissions Directive were not carried out. As regards the remaining coal phase-out, the government took a market-based approach, allowing power plants to burn coal until the drop in the cost of renewables and the price of a tonne of CO2 in the EU-ETS (€35 in 2030) pushed coal power out of Spain’s electricity mix.

The Spanish government furthermore divested (sold its shares and other financial instruments) from companies that extracted, refined or processed fossil fuels, following a divestment plan that was drafted by 2021, in accordance with the Climate Change and Energy Transition Law.16 Government divestment provided incentives for other social agents to follow suit.

The government reached an agreement with utilities so that nuclear phase-out became a reality in Spain by 2035, with nuclear power being phased out when nuclear power plants reached a maximum of 46 years in operation. The government’s initial plans of not extending nuclear power plants’ useful life beyond 40 years were adapted after negotiating with utilities. CSO’s that had historically advocated early closures (calling for nuclear power plants to be decommissioned after 40 years in operation, at most) implicitly accepted the phase-out agreement.

Overall investment needs for the implementation of the INECP in Spain for 2021-30 amounted to €236.12 billion, most of which were disbursed by the private sector. There were initial concerns about whether the private sector would indeed be able and willing to invest 80% of the needs for the INECP, but the private sector recognised the economic opportunity of the low-carbon transition and invested accordingly, meeting the government private-sector investment figures in 2021-30. Investments in energy efficiency amounted to €86.48 billion. Estimated investment in updating power networks and electrification to meet the 2030 decarbonisation goals amounted to €41.84 billion, with an overall investment in renewables of €101.63 billion. Concerns about a potential crowding-out effect were dispelled as empirical data showed large investments in low-carbon transition need not automatically lead to investment reductions in other economic sectors.17

Spain’s interconnections with France, Morocco and Portugal remained very limited until 2020, amounting to <5% of Spain’s generation capacity in 2019, half of which were interconnections to France. This made Spain the only European country that failed the EU target of 10% interconnection capacity in 2020. Hence, Spain developed new interconnections with Portugal (reaching 3,000 MW in 2030) and France (reaching 8,000 MW in 2030, up from 2,800 MW in 2019). A ratchet-up mechanism for interconnections, renewables and energy efficiency goals was included in the INECP for 2023, coinciding with the Global Stocktake enshrined in the Paris Agreement. Spain’s INECP’s target of reaching 15% interconnection of installed capacity in 2030, in alignment with the EU’s interconnection goal, was met. From 2019 Morocco was a net electricity exporter to Spain, but new rules were introduced to prevent coal and gas-generated electricity being exported to the EU. Meanwhile, increasing domestic demand in southern Mediterranean partners continued to put pressure on local installed capacity, including the deployment of renewables.

As for the transport sector and electric mobility,18 Spain banned the registration and sale of internal combustion engine (ICE) vehicles in 2040 as stated in the Climate and Energy Transition Law, despite initial resistance from the car manufacturers’ association. By 2050 only zero-emission privately-owned vehicles were allowed to circulate. By 2030, 5 million Electric Vehicles (EVs) were in use in Spain, with a significant impact on electricity demand. Charging infrastructure for EVs in Spain was small in 2018, but from 2020 onwards the Spanish Climate Change and Energy Transition Law required petrol stations across the country selling more than 5 million litres of fuel annually to present a project to install charging stations of ≥22 kW, reaching 9% of petrol stations across Spain. The Ministry for Ecological Transition regulated which petrol stations had to have charging points and when they had to be operational. For smaller petrol stations the deadlines for projects and operation of charging points was more flexible. Additionally, municipalities of ≥50,000 inhabitants established by law low-emission zones by 2023 (at the latest) and fostered the deployment of public and private EV charging points.

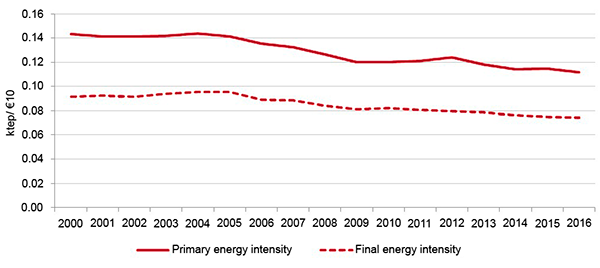

Spain’s INECP included a 32.5% energy efficiency goal vs. a trend scenario, in alignment with the EU goal for 2030. However, Spain achieved its ‘Target Scenario’ energy efficiency goal of 39.6% primary-energy intensity improvement in 2030 (3.6% primary-energy efficiency gains per annum from 2021 to 2030). Energy efficiency goals were achieved through reductions in both primary and final energy consumption (-16.16% and -6.22%, respectively) in 2030 compared with 2015 levels. Electricity consumption in final energy consumption increased 8,16% from 2015 to 2030 (from 19.951 ktoe to 21,579 ktoe), but electricity consumption in final energy consumption was reduced in the residential sector by 12% (from 6,025 ktoe in 2015 to 5,301 ktoe in 2030), essentially through improvements in the thermal envelope of buildings and improvements in district heating and domestic hot water (DHW). Energy efficiency goals achieved, in line with the government’s ‘Target Scenario’, were highly ambitious, as Spain’s energy efficiency improvements in 2000-16 period showed (see Figure 1 below).

In accordance with the updated Energy Efficiency Directive of 2018 the Spanish government increased energy efficiency in buildings by improving the thermal envelope of 1.2 million homes from 2021 to 2030, renovated heating, water heating and air conditioning in 300,000 buildings per year and renovated 3% of publicly-owned buildings. The government also promoted an increase in the use of renewable electricity sources in retrofitted buildings and new buildings. Demand-side response policies were actively developed by the government to nudge consumers into lower carbon consumption patterns that would allow a greater penetration of renewables and greater stability in the power system. Smart metering allowed raising awareness of energy consumption, helping consumers shift energy use in heating, cooling and domestic hot water. Financing mechanisms were fostered by the government to ensure retrofitting of the existing building stock and the construction of near-zero energy buildings. Subsidies were also given to low-income families to allow for retrofitting investments, based on energy savings audits and performance. Public-private partnerships were established to reach retrofitting goals.Figure 2. Spanish State-centred dominant policy pathway according to Spain’s INECP ‘Target Scenario’ according to the PSOE government, 2016-50

| ES: Dominant | 2016 | 2020 | 2030 | 2040 | 2050 |

|---|---|---|---|---|---|

| GHG reduction targets. Economy-wide (baseline year) | 283 Mt CO2eq | 327 Mt CO2eq | -21% (1990) | -90% (1990) | |

| ETS sector reduction targets | 229 Mt CO2eq (European annual emission allocation) | 219 Mt CO2eq (European annual emission allocation)-21% | -60% | ||

| Non-ETS sectors emission reduction targets (baseline year) | -10% (2005) | -38% (2005) | |||

| GHG reduction targets (electricity sector) | |||||

| Renewables targets (energy; % of final energy consumption) | 20% | 42% | |||

| Renewables targets (electricity; % of final energy consumption) | 39%; 108 TWh; 49 GW | 74% | 100% | ||

| Intermittent renewables | 57 TWh; 28 GW | 36.3 GW | 87.3 GW | ≥ 2030 | ≥ 2040 |

| Wind onshore | 49 TWh; 23 GW | 27.9 GW | 50.3 GW | ||

| Wind offshore | Included above | Included above | Included above | ||

| Solar PV | 8 TWh; 5 GW | 8.4 GW | 37 GW | > 2030 | > 2040 |

| Dispatchable renewables | 51 TWh; 21 GW | ≥ 2030 | ≥ 2040 | ||

| Biomass | 5 TWh; 1 GW | 1.6 GW | 2.4 GW | ||

| Hydro | 40 TWh; 14 GW | 15.8 GW | 16.3 GW | ||

| CSP | 6 TWh; 2 GW | 2.3 GW | 7.3 GW | ≥ 2030 | ≥ 2040 |

| Other renewables (year of data when different to column heading) | 1 TWh; 0.2 GW (2015 | 0.2 GW | 0.3 GW | ||

| Net traded renewables (year of data when different to column heading) | -3 TWh (2015) | 11 TWh | 6.7 TWh | ||

| Nuclear | 59 TWh; 7.4 GW | 7.4 GW | 3.2 GW | 0 | 0 |

| Fossil fuels | 108 TWh; 48GW | 45.1 GW | 32.5 GW | ||

| CCS | 0 | 0 | 0 | 0 | 0 |

| Lignite | 0 TWh | 0 | 0 | 0 | 0 |

| Hard coal | 36 TWh | 10.6 GW | 0 | 0 | 0 |

| Gas | 54 TWh | 31.2 GW | 30.2 GW | ||

| Petroleum | 16 TWh | 3.4 GW | 2.3 GW | ||

| Other non-renewables | 1 TWh | 0 | 0 | ||

| Storage | |||||

| Battery | 2.5 GW | ||||

| Pumped Hydropower | 3.3 GW | 4.4 GW | 7.9 GW | ||

| Other storage | |||||

| Cross-border interconnection NTC | < 5% of installed capacity | 10% of installed capacity | 15% of installed capacity | ||

| Electrification of additional sectors | |||||

| Total heating demand incl. non-electric heating | |||||

| Heating with electricity (energy supplied by heat pumps) | 4.1 TWh 353 ktoe | 7.6 TWh 651 ktoe | 47 TWh 4,076ktoe | ||

| Total cooling demand incl. non-electric cooling | |||||

| Cooling with electricity | |||||

| Electric mobility | 22% RES (electrification & biofuels) 5 million EV | >> 2030 Ban on ICE sales & registrations | >> Ban on ICE circulation | ||

| EV chargers (year of data when different to column heading) | 4,974 (2017) | > 2017 | >> 2020 | >> 2030 | >> 2040 |

| Gross electricity consumption (year of data when different to column heading) | 232 TWh (2015) | 234 TWh | 251 TWh | ||

| Final energy consumption (year of data when different to column heading) | 84,542 ktoe (2015) | 88,994 ktoe | 79,279 ktoe |

Source: the authors

Market-centred pathway: Partido Popular19

By 2050 Spain had achieved an 80% decarbonisation of its economy in a manner that was economically efficient, hence not only meeting international commitments but also in a way that was ‘beneficial to our families and companies’. To achieve this, the government, to the extent possible, avoided interfering with market rules except where necessary to correct market failures associated with environmental externalities and where international climate commitments were at stake. Hence, the few measures taken were market-based, such as a carbon tax (for the non-trading sector), the EU emission trading scheme and auctions for renewable power, leading to efficient levels of decarbonisation.

While all types of actors were enabled to carry out the transition, the private sector and particularly large corporations remained important players over the entire period given their ability to engage in large and cost-efficient investments. Besides renewable generators (especially utility-scale plants with lower specific generation costs), nuclear and fossil fuels with CCS played an important role in the energy transition towards a decarbonised economy. Increasing the interconnection capacity always ranked high in the agenda as a pre-requisite for a cost-optimal exchange of electricity and balancing in the internal European electricity market.

Spain has always followed the trajectory prescribed by the EU, neither lagging behind nor rushing ahead, in order to achieve a coordinated, cost-efficient decarbonisation of Europe together with the other EU Member States. Hence, the Spanish economy is expected to be 80% decarbonised by 2050 (compared with 1990), following the accomplishment of a 26% reduction of emissions in the non-trading sector by 2030. The key enabler to this was the implementation of the National Strategy for a Low-Emission Economy by 2050, which guided the transition to a low-carbon economy. Among other measures, this strategy was based on cost-efficient measures to increase energy efficiency and deploy a mix of low-carbon technologies leading to a cost-optimal mix of renewables, nuclear power and fossil fuels with CCS.

In order to make use of the most cost-efficient decarbonisation measures, the Spanish government did not define specific renewable energy or electricity targets beyond the 2030 renewable energy target (32% renewable energy); in the electricity sector, this led to the deployment of the renewables with the lowest system cost both in Spain and abroad (to the extent allowed by the interconnectors). Already in the period before 2018, renewable electricity deployment was promoted through technology-neutral auctions and the relative increase in competitiveness through carbon price measures.

While there was no specific target for intermittent renewables, PV and onshore wind power became the main pillars of the Spanish system given the lower cost compared to other renewables and the technology-neutral design element of the renewable auctions. Similarly, dispatchable renewables-biomass (with and without CCS) hydropower and CSP never had explicit targets and their expansion occurred at the time and location where they proved cost-efficient from a system perspective as a way to balance PV and wind power.

Similarly, both physical imports or statistical transfers of renewables (through cooperation) were important measures both for balancing the Spanish power system and to meet the EU-mandated renewables targets in a cost-optimal manner. This was further supported by the expansion of new interconnectors. The latter was one of the key Spanish priorities, both to facilitate the completion of the internal electricity market and to allow increased electricity trade, including cross-border renewables trade under the cooperation mechanism. To this end, the government both met and exceeded the EU-mandated interconnector targets.

Nuclear power continued to play a non-trivial role in the Spanish power system, as the old reactors extended their economic lifetime provided their technical characteristics allowed operation in safety conditions. Yet fossil-fuelled CCS and renewables were expanded to become the main pillars of decarbonising the Spanish power system . Consistent with the focus on cost-efficiency, there was no mandated closure of any power station, including coal power; however, the increasing carbon price (within the EU ETS) gradually forced older coal/lignite power stations off the market from the 2020s onwards. The government also promoted gas interconnections in order to strengthen the European internal gas market through access to the gas pipelines from North Africa and LNG.

Several measures were aimed at promoting the deployment of distributed generation and electric self-consumption. As a result, an increased use of decentralised batteries followed. The increased penetration of renewable energies required an increase in the use of electricity storage technologies in the form of grid-scale batteries and pumped hydropower installations.

In the residential, institutional and commercial sectors, various measures were put in place to improve and promote energy efficiency, zero emission buildings, distributed generation, electricity self-consumption, low emission heating and cooling systems, and smart metering. A sustainable transport sector was promoted with a special boost to rail transport. The promotion of the use of electric vehicles was limited by the expansion of a network of charging points, enabling but not directly supporting an expansion of the EV fleet. When it comes to public procurement, public tenders for new vehicles only allowed for alternative-fuel vehicles, except for those vehicles that could not perform public duties or for unjustified economic costs. Electrification of other sectors was pursued to the extent that it supported a cost-optimal decarbonisation of society as a whole, but no specific targets or support measures for heating were introduced.Figure 3. Quantification of the Spanish market-centred minority policy pathway as described by the Partido Popular, 2016-50

| ES: Market | 2016 | 2020 | 2030 | 2040 | 2050 |

|---|---|---|---|---|---|

| GHG reduction targets (economy-wide) | 283 Mt CO2eq | 10% (GHG-2005) | Non-ETS 26% (GHG-2005) | > 2030 | 80% (GHG-1990) |

| ETS sector reduction targets | 229 Mt CO2eq (European annual emission allocation) | 219 Mt CO2eq (European annual emission allocation) | |||

| Non-ETS sectors emission reduction targets | 10% (GHG-2005) | 26% (GHG-2005) | |||

| GHG reduction targets (electricity sector) | |||||

| Renewables targets (energy; % of final energy consumption) | 20% | 32% | |||

| Renewables targets (electricity; % of final energy consumption) | 39%; 108 TWh; 49 GW | > 2016 | > 2020 | > 2030 | > 2040 |

| Intermittent renewables | 57 TWh; 28 GW | ||||

| Wind onshore | 49 TWh; 23 GW | > 2016 | > 2 020 | > 2030 | > 2040 |

| Wind offshore | Included above | > 2016 | > 2020 | > 2030 | > 2 040 |

| Solar PV | 8 TWh; 5 GW | > 2016 (mainly centralised) | > 2020 (mainly centralised) | > 2030 (mainly centralised) | > 2040 (mainly centralised) |

| Dispatchable renewables | 51 TWh; 21 GW | > 2016 | > 2020 | > 2030 | > 2040 |

| Biomass | 5 TWh; 1 GW | ||||

| Hydro | 40 TWh; 14 GW | ||||

| CSP | 6 TWh; 2 GW | ||||

| Other renewables | 1 TWh | ||||

| Traded renewables | |||||

| Physical import of renewables (cooperation) | > 2016 | > 2020 | > 2030 | > 2040 | |

| Statistical transfer of renewables (cooperation) | = 2016 | ≥ 2016 | ≥ 2016 | ≥ 2016 | |

| Explicit trade of CSP or hydropower | |||||

| Nuclear | 59 TWh 7 GW | = 2016 | = 2016 | = 2016 | = 2016 |

| Fossil fuels | 108 TWh; 48 GW | ||||

| CCS | 0 | > 2016 | > 2030 | > 2040 | |

| Lignite | 0 TWh | ≤ 2016 | ≤ 2016 | ||

| Hard coal | 36 TWh | ≤ 2016 | ≤ 2016 | ||

| Gas | 54 TWh | ≥ 2016 | ≥ 2016 | ≥ 2016 | ≥ 2016 |

| Petroleum | 16 TWh | ||||

| Other non-renewables | 1 TWh | ||||

| Storage | |||||

| Battery | > 2016 | > 2020 | ≥ 2030 | ≥ 2040 | |

| Pumped Hydropower | > 2016 | > 2020 | ≥ 2030 | ≥ 2040 | |

| Other storage | |||||

| Cross-border interconnection NTC | ≥ 10%of yearly power production | ≥ 15%of yearly power production | ≥ 2030 | 2030 | |

| Electrification of additional sectors | |||||

| Total heating demand incl. non-electric heating | |||||

| Heating with electricity | |||||

| Total cooling demand incl. non-electric cooling | |||||

| Cooling with electricity | |||||

| Electric mobility | |||||

| EV chargers | > 2016 | > 2020 | > 2030 | > 2040 | |

| Gross electricity consumption | 275 TWh | ||||

| Final energy consumption |

Source: the authors.

Grass-roots-centred pathway: Unidas Podemos 20

Spain almost achieved a full decarbonisation of the entire economy by 2050. In the electricity sector, this was achieved through strict phase-out policies for fossil-fuel power and emphasising the role of citizens and communities in building up a new and renewable power system. The needs of the citizens were at the core of all climate and energy policies, supported by institutions such as the State Climate Change Agency and the Citizen Climate Change Commission. Through active policy, citizens were empowered to have a more pro-active role by supporting the decentralisation of the energy system and encouraged to become prosumers. The re-communalisation of electricity provision was approved in subsequent local referendums following the example of Barcelona Energy in 2018, when a public metropolitan electricity operator started supplying renewable electricity to the city so that, over time, control over the entire system became communal.

Regarding interconnections and EU cooperation mechanisms, the emphasis is on decentralisation and re-communalisation instead of cross-border mega-projects and further market integration. As a consequence, by 2050 interconnections remain at the 2030 15% goal or slightly higher while virtual and physical cooperation mechanisms remain marginal: the maxim was and remains ‘Spanish renewables for and by Spanish citizens’. Another key aspect of the Unidas Podemos strategy was an emphasis on energy efficiency: the targets of 40% less primary energy demand by 2030 and 50% less by 2050 (compared to 1990) were achieved in part with efficiency measures and in part through electrification of additional sectors, primarily transport.

When it comes to greenhouse emissions, compared with 1990 levels, in 2030 emissions had fallen by 35%, by 70% in 2040 and by 95% in 2050. This was accomplished through the combination of reducing primary energy consumption (40% less energy consumed by 2030 and a 45% reduction of energy consumption by 2040 compared with 1990 levels) as well as the strong deployment of renewables to fill the gap of the phased-out fossil and nuclear generators. The transition was facilitated by two broad energy programmes: (a) the Energy Efficiency National Plan that targeted the housing, transport and industrial sectors; and (b) the Renewable Energies National plan that focused on deployment of renewable power generation (solar, wind, geothermal, small hydropower and low-emitting biomass).

To implement these plans, 1.5% of GDP was mobilised annually over 20 years, comprising both public and private resources, to drive the necessary investments in generation and infrastructure. For example, a Green Finance Fund for mitigation and adaptation was created and the Law for Energy Transition also provided funds for a fair transition in part raised through new environmental taxes and the abolishment of subsidies and tax exemptions for the fossil-fuel industry and for consumption. New measures to prevent oligopolistic practices (including vertical integration) in the electricity market were implemented to prevent large energy corporations concentrating too much power and to support the small-scale actors entering the system. Finally, measures were put in place to decouple the ownership and management of the distribution system. Aligned with a grassroots political party ideal, both plans were implemented in a way that ensured most electricity generation and distribution phases remained in the hands of public entities (especially municipalities), consumers or small enterprises and not large corporations.

With respect to renewable power, the power system has been 100% renewable since 2045, following the achievement of the interim renewable power target of 80% in 2030. Besides targeted support measures for small renewable power plants, the municipalities granted soft loans through the Green Finance Fund (Fondo de Financiación Verde). Furthermore, there was a green procurement strategy by which all public administrations were obliged to consume 100% renewables on their premises so as to reduce the life-cycle environmental impacts of energy use. Finally, the government divested funds from fossil-fuel related companies to incentivise private consumers to invest in renewable energy through subsidies.

Intermittent renewables, especially PV, experienced a great expansion as a result of the support measures included in the Renewable National Plan, including dedicated support for onshore wind power (> 6 MW). A special emphasis was put on special support mechanisms for investments in renewable generators smaller than 1 MW. Furthermore, a new regulatory framework was implemented already in 2018 and maintained since, to support self-consumption, which included the following features: (a) self-consumption was not taxed; (b) electricity fed into the electricity system was remunerated in a fair manner by the distributor company; and (c) quick and simple administrative procedures were established. Consequentially, all renewables grew continuously from 2018 onwards, but decentralised PV grew particularly fast.

As for dispatchable renewables, research, development and innovation plans were specifically designed for the development of new dispatchable technologies, including measures to improve the flexibility of renewables. As the performance of these technologies improved, their deployment grew from 2020 on. As a result, a diverse fleet of dispatchable renewables was deployed over time, including both CSP, hydropower and biomass. When large hydropower plants private ownership came to an end, they became state-owned. As a result, the role of large hydropower plants changed from providing bulk power to being providers of back-up capacity to complement variable solar PV and wind-power generation. Similarly, the growing biomass power fleet was used mainly to balance the system, and not merely to generate bulk energy.

Accompanying the rise of renewables was the decline of nuclear and fossil power. Following the phase-out decisions in 2019, all nuclear and coal power plants were shut down progressively until the last power plants were closed in 2025. The existing gas power stations were allowed to continue operating beyond 2025 insofar as they provided back-up capacity to the system and contributed to guarantee supply. Throughout the whole period, fracking was forbidden and natural gas production in Spain was practically banned; further, as CCS was not supported, there was no expansion of CCS stations at any time. In all these phase-out cases (especially nuclear and coal plants), the abandonment of the plants followed a fair transition approach for workers so that they have found new employment opportunities.

Given its focus on small-scale, local and distributed electricity, Unidas Podemos limited the development of new interconnection capacity to the minimum necessary to support the further deployment of renewables in Spain (in accordance with EU targets). Instead of developing new transmission infrastructures, Unidas Podemos supported the development of micro- and other local networks, minimising the need for transmission. Consequently, there was no explicit trade with renewables, dispatchable or fluctuating, and Spain has not made use of cooperation mechanisms.

In order to support the balancing of fluctuating renewables, and to minimise the need for further electricity grids, the government supported early on the development and deployment of new storage technologies. This included both batteries and hydrogen, initially through R&D support and later on through deployment support, so as to keep the power system stable and minimise the need for new national and cross-border grid infrastructure. Through various support measures (such as the provision of special tariffs), the law for the energy transition and climate change supported the electrification of certain consumptions such as industrial, heating and transport.

As to the decarbonisation of the transport sector, Unidas Podemos: (a) promoted the use of bicycles in many ways (for example, by facilitating bicycle access to other public transport modes); (b) revised public transport services provision contracts; and (c) promoted electric vehicles. Thanks to the various support measures in place, Spain achieved a 25% share of EV in sales of new cars by 2025, 70% of new cars were EV by 2030 and all new vehicles were EVs by 2040. Furthermore, a programme was developed to promote the use of electric vehicle chargers.Figure 4. Quantification of the Spanish grassroots-centred minority policy pathway as described by Unidas Podemos, 2016-50

| ES: Grassroots | 2016 | 2020 | 2030 | 2040 | 2050 |

|---|---|---|---|---|---|

| GHG reduction targets (economy-wide) | 283 Mt CO2eq | 35% (1990) | 70% (1990) | 95% (1990) | |

| ETS sector reduction targets | 229 Mt CO2eq (European annual emission allocation) | 219 Mt CO2eq (European annual emission allocation) | |||

| Non-ETS sectors emission reduction targets | 10% (GHG-2005) | 26% (GHG-2005) | |||

| GHG reduction targets (electricity sector) | > 2016 | 45% | 60% | 100% | |

| Renewables targets (energy; % of final energy consumption) | > 2016 | ||||

| Renewables targets (electricity; % of final energy consumption) | 39%; 108 TWh; 49 GW | > 2016 | 80% | 100% (by 2045) | |

| Intermittent renewables | 57 TWh; 28 GW | > 2016 | > 2020 | > 2030 | > 2040 |

| Wind onshore | 49 TWh; 23 GW | > 2016 | > 2020 | > 2030 | > 2040 |

| Wind offshore | Included above | = 2016 | = 2016 | = 2016 | = 2016 |

| Solar PV | 8 TWh; 5 GW | >> 2016 (mainly decentralised) | >> 2020 (mainly decentralised) | >> 2030 (mainly decentralised) | >> 2040 (mainly decentralised) |

| Dispatchable renewables | 51 TWh; 21 GW | > 2016 | > 2020 | > 2030 | > 2040 |

| Biomass | 5 TWh; 1 GW | > 2016 | > 2020 | > 2030 | > 2040 |

| Hydro | 40 TWh; 14 GW | > 2016 | > 2020 | > 2030 | > 2040 |

| CSP | 6 TWh; 2 GW | > 2016 | > 2020 | > 2030 | > 2040 |

| Other renewables | 1 TWh | ||||

| Traded renewables | |||||

| Physical import of renewables (cooperation) | |||||

| Statistical transfer of renewables (cooperation) | |||||

| Explicit trade of CSP or hydropower | |||||

| Nuclear | 59 TWh 7 GW | 0 (by 2025) | 0 | 0 | |

| Fossil fuels | 108 TWh; 48 GW | ||||

| CCS | 0 | ||||

| Lignite | 0 TWh | << 2016 | 0 (by 2025 | 0 | 0 |

| Hard coal | 36 TWh | << 2016 | 0 (by 2025 | 0 | 0 |

| Gas | 54 TWh | < 2016 | < 2020 | < 2030 | < 2040 |

| Petroleum | 16 TWh | < 2016 | < 2020 | < 2030 | 0 |

| Other non-renewables | 1 TWh | ≥ 2016 (Waste) | ≥ 2016 (Waste) | ||

| Storage | |||||

| Battery | > 2016 | > 2020 | > 2030 | > 2040 | |

| Pumped Hydropower | |||||

| Other storage | > 2016 | > 2020 | > 2030 | > 2040 | |

| Cross-border interconnection NTC | ≥ 10% of yearly power production | ≥ 15% of yearly power production | = 2030 | = 2040 | |

| Electrification of additional sectors | |||||

| Total heating demand incl. non-electric heating | |||||

| Heating with electricity | |||||

| Total cooling demand incl. non-electric cooling | > 2016 | > 2020 | > 2030 | > 2040 | |

| Cooling with electricity | > 2016 | > 2020 | > 2030 | > 2040 | |

| Electric mobility | 3% EV (by 2020), 25% EV (by 2025) | 70% (EV) | 100% (EV) | ||

| EV chargers | >> 2016 | > 2020 | > 2030 | > 2040 | |

| Gross electricity consumption | 275 TWh | ||||

| Final energy consumption |

Source: the authors.

Conclusions

The pathways described, depicted in this paper as if they had materialised, are not the only ones proposed by political parties for Spain’s energy transition. However, they illustrate the continuum of options in the energy transition policy space and constitute the best-specified set of energy transition alternatives for Spain. As expected, they do not represent ‘pure’ State, market or grassroots-centred closed models, but rather ‘scripts’ for energy transition with different combinations of elements present in other logics. For instance, the socialists’ State-centred logic includes auctions, the Popular Party’s market approach includes some command and control measures, and the Unidas Podemos’ grass-roots approach comes with significant State intervention. Nevertheless, they constitute coherent, all-encompassing alternative stories on how to achieve the energy transition in three different ways, following three distinct decarbonisation logics and leading to three very different (more or less) climate-friendly energy futures.

For the Socialist Party, the decarbonisation of the Spanish power system is driven by targeted measures enacted by the government, in addition to having economy-wide decarbonisation targets for 2030 and 2050. Some of the key measures included a mandatory and gradual nuclear phase-out between 2025 and 2035, a largely market-driven coal phase-out ahead of 2030 (fostered by EU regulation), banning internal combustion engines and (most) new fossil fuel subsidies, a gradual phase out of existing fossil-fuel subsidies, mandatory deployment of recharging infrastructure for EVs and mandatory retrofitting of buildings, among others. Interconnections were promoted by the government in this pathway, in line with EU requirements, to prevent blackouts during dry years and to support the expansion of renewables.

Under the Popular Party’s market-centred logic, the Spanish energy transition is mostly driven by private actors under an economy-wide decarbonisation target. The government took a few high-level, strategic decisions to ensure the alignment with EU energy and climate objectives and ambition and, whenever needed, the government used market-based instruments (carbon tax, technology neutral auctions for renewables, etc) to correct market failures and get the transition going. The government also put a special emphasis on increasing interconnections as a way to transition to an integrated and cost-efficient EU electricity market.

Unidas Podemos is aligned with the grassroots logics. The key for enabling the Spanish energy transition is empowering citizens and local communities as the main actors of the transition strategy, while progressively abandoning fossil and nuclear technologies. As a result, a highly decentralised small-scale and smart local community-owned power system was achieved. New technologies were developed as a result of R&D programmes (technology push) as well as market pull policies (support policies in the form of subsidies and other incentives). Regarding interconnections and cooperation mechanisms, the local and community logic has limit interconnections to compulsory EU targets and intra-EU renewable exchange remains small.

Despite the differences across energy transition pathways Spain embraced a low(er) carbon development model from 2020 to 2050. The acrimonious political debate that had stalled the drafting and passing of the Climate Change and Energy Transition Law between 2011 and 2019 was finally resolved in 2020. The response from the EC, and from civil society, to Spain’s draft INECP made its content the benchmark across political parties that avoided defaulting on Spain’s energy and climate commitments, albeit relying on different policy instruments to ensure targets were met. This meant a more command-and-control (CAC) based approach from socialist governments, more use of market-based instruments (MBIs) by conservative governments and greater emphasis on both CAC and moral suasion, coupled with bottom-up initiatives, from left-wing governments.

However, the INECP had to be strengthened over time to align Spain’s targets to the goals of the Paris Agreement. Key elements in robust climate laws were gradually included in Spain’s climate actions by governments from across the political spectrum. Among these elements were an independent committee on climate change à la UK, national and sectoral carbon budgets, parliamentary oversight of climate and energy goals, transparent and regular stakeholder engagement, and the requirement to disclose exposure to climate risks by investors and asset managers, following France’s lead.

Natalia Caldés

CIEMAT

Gonzalo Escribano

Elcano Royal Institute | @g_escribano

Lara Lázaro

Elcano Royal Institute | @lazarotouza

Yolanda Lechón

CIEMAT | @YLechon

Christoph Kiefer

CSIC

Pablo del Río

CSIC

Richard Thonig

Institute for Advanced Sustainability Studies | @RThonig

Johan Lilliestam

Institute for Advanced Sustainability Studies | @JLilliestam

Legal Notice

The sole responsibility for the content of this publication lies with the authors. It does not necessarily reflect the opinion of the European Union. Neither the INEA nor the European Commission is responsible for any use that may be made of the information contained therein.

All rights reserved; no part of this publication may be translated, reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, re-cording or otherwise, without the written permission of the publisher.

Many of the designations used by manufacturers and sellers to distinguish their products are claimed as trademarks. The quotation of those designations in whatever way does not imply the conclusion that the use of those designations is legal without the content of the owner of the trademark.

1 Lilliestam, J., R. Thonig, L. Späth, N. Caldés, Y. Lechón, P. del Río, C. Kiefer, G. Escribano & L. Lázaro Touza (2019), Policy pathways for the energy transition in Europe and selected European countries, Deliverable 7.2 MUSTEC project, Deliverable 1 SCCER JA IDEA, ETH Zürich, Zürich.

2 Grupo Parlamentario Popular en el Congreso (2019), “Proposición de Ley de Cambio Climático y Transición Energética”; Ministerio para la Transición Ecológica (2019), “Anteproyecto de Ley de Cambio Climático y Transición Energética”; Grupo Parlamentario Confederal de Unidos Podemos-En Comú Podem-En Marea (2018), “Proposición de Ley sobre Cambio Climático y Transición Energética”.

3 Lawrence Freedman (2013), Strategy: a History, Oxford University Press, chapter 38.

4 It should be noted that increasing concern about climate change affected policies and implementation across the three decarbonisation pathways (State-centred, market-centred and grassroots).

5 It should be noted, however, that the socialist government did not mandate a coal phase-out by 2030 but rather relied on EU legislation and on market factors (continued cost reductions in renewables, price of the tonne of CO2 of €35 in 2030) that forced coal out of the Spanish electricity mix. The INECP, however, stated that phasing out coal was key to achieve the decarbonisation goals. Hence the Spanish government reserved the right to undertake ‘any appropriate measures deemed necessary’ to meet the RES electricity target (74% by 2030).

6 Article 9 of the current draft proposal for the Climate Change and Energy Transition Law presented by the socialist government states that new fiscal benefits for fossil fuel products will only be allowed under special circumstances detailed below.

7 ‘[CSOs] can be defined to include all non-market and nonstate organizations outside of the family in which people organise themselves to pursue shared interests in the public domain. Examples include community-based organisations and village associations, environmental groups, women’s rights groups, farmers’ associations, faith-based organisations, labour unions, co-operatives, professional associations, chambers of commerce, independent research institutes and the not-for-profit media’ (UNDP, undated).

8 Czech Republic (-30%), Germany (-55%), Ireland (-40%), France (-40%), Latvia (-40%), Lithuania (-40%), Hungary (-40%), the Netherlands (-49%), Portugal (-45%), Romania (-50%) and Sweden (-63%).

9 Most of the new CSP capacity (5 GW) had nine hours of storage capacity as modelled in Spain’s PNIEC.

10 Note that nuclear phaseout took place in 2025-35, which explains the 3GW of nuclear in 2030.

11 See page 42 of the INECP.

12 Defined in Article 9 of the draft Climate Change and Energy Transition Law as fiscal benefits and other support mechanisms or measures that foster the use of fossil fuels.

13 The potential loophole in the drafting of Article 9 (effectively allowing fossil fuel subsidies to continue) gave rise to several comments in the public consultation process prior to the passing of the Climate Change and Energy Transition Law. These comments were taken into consideration by the government to ensure appropriate monitoring of subsides, effectively restricting new fossil fuel subsidies to vulnerable families and small-scale farmers whose livelihoods could be significantly affected by higher fuel prices.

14 These figures are available from page 206 of the INECP and are based on information provided by Spain’s tax agency.

15 Which amounted to 10,4 GW of installed capacity in 2018. See IIDMA (2019), ‘Un oscuro panorama. Las secuelas del carbón’, (accessed 18/V/2019).

16 See the second additional provision of the draft Climate Change and Energy Transition Law for further details.

17 Pollit & Mercure (2018) argue that Computable General Equilibrium (CGE) models assume crowding-out effects as a result of climate policies. The authors argue that macro-econometric models based on non-equilibrium economic theory do not necessarily lead to crowding out effects and can even serve as an economic stimulus.

18 Whose emissions amounted to 25% of total emissions in 2015 and 48% of of diffuse sector emissions in 2017.

19 Partido Popular (2015), ‘Seguir avanzando. Programa electoral para las elecciones generales de 2015’, Partido Popular, Madrid; Partido Popular (2018), ‘Proposición de Ley sobre Cambio Climático y Transición Energética’, Grupo Parlamentario Popular en el Congreso, Boletín Oficial de las Cortes Generales, Madrid; Público (2018), ‘El PP es el único partido que está a favor del “fracking”, del almacén nuclear y del “impuesto al sol”,(accessed 07/V/2019); SNE (2015) ‘El Partido Popular promete mantener las centrales nucleares y terminar el ATC’, Sociedad Nuclear Española (SNE), (accessed 07/V/2019); Partido Popular (2019), ‘Elecciones generales, autonómicas y municipales 2019. Programa electoral’, Partido Popular, Madrid.

20 Podemos (2018), ‘Proposición de Ley sobre Cambio Climático y Transición Energética’, Grupo Parlamentario Confederal de Unidos Podemos-En Comú Podem-En Marea, Boletín Oficial de las Cortes Generales, Madrid; Podemos (2019), ‘Programa de Podemos para un nuevo pais. Programa Electoral elecciones 2019’.