Theme

In the context of slow growth, destabilising capital flows and currency wars, the G20 must develop joint solutions to overcome common problems.

Summary

Growth and commerce are slowing down, financial markets are increasingly panicky, the thesis of secular stagnation is gaining strength, and huge capital flows and exchange rate misalignments are creating instability and uncertainty. Given this worrying outlook, and the huge interdependences that exist in the global economy, multilateral cooperation should be the highest priority. The problem is that the new threats are not punctual and clearly visible. Rather, they are protracted, structural and not easy to explain. This has dampened the sensation of urgency and discouraged bold joint action from the G20. This inactivity has fed two intertwined dangers: the return of protectionist and nationalist policies and the formation of rivalling blocs. Spain, as a country that believes firmly in the need for multilateralism, is keen to tackle these risks and be a responsible and reliable partner in finding common solutions. The truth is that major agreements to solve the huge structural problems mentioned above are unlikely, but concrete steps are certainly possible. A new global recession needs to be avoided.

Analysis

The consolidation of the G20 as the main international forum to discuss issues related to global economic governance is without doubt the most important institutional innovation since the creation of the G7 in 1975. Now, for the first time in history, leaders from both developed and developing countries meet on an annual basis to debate the short and long-term challenges of the world economy. This is a very positive development. In fact, the forum was critical in overcoming the global financial crisis in 2008-09. The first G20 meetings in Washington DC (2008) and London (2009) showed great unity, coordination and determination in using aggressive monetary and fiscal policy to avoid a further collapse in global finance and trade. Fortunately, through the G20-infused dialogue and experience-sharing, world leaders identified early on in the unfolding of the crisis the mistakes of the past and resisted the temptation to embrace protectionist measures, as occurred in the 1930s after the 1929 crash. Thus, a second great depression was avoided.

However, while certainly crucial in establishing a platform for joint action and continuous dialogue, we should not overestimate the importance of the G20 forum in fighting the crisis (Helleiner, 2014). Effective multilateral coordination is always easier to develop when the global economy is at the brink and the main stakeholders are staring into the abyss. Even without the existence of the G20, given the dramatic state the world economy was in after the collapse of Lehman Brothers, it is reasonable to believe that the biggest economies would have had developed similar Keynesian programmes as they eventually did. It was in their national short-term interest to do so. Multilateral cooperation is more difficult to craft when the dangers of a global recession are not that imminent, when both short- (and perceivably) long-term interests are not aligned and when there is no clear leadership (Cohen, 2013). This is precisely the scenario we are witnessing since 2010. Over the past five years the G20 meetings have increasingly lost momentum. The final communiqués start always with the sentence that the G20 leaders are jointly committed to achieve “strong, sustainable and balanced growth” and then there is a long list of important problems that need to be addressed, but substantial agreements and actions have been missing.

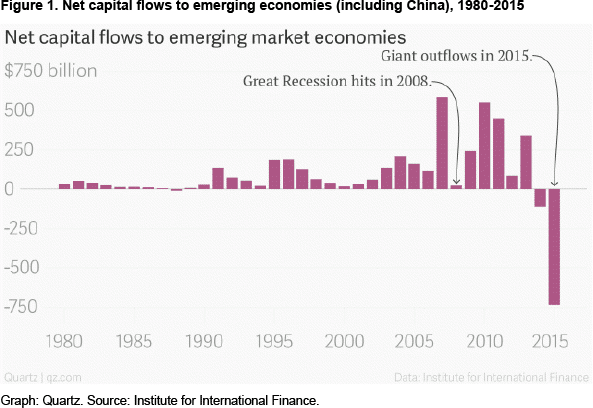

Despite this apparent complacency, the fact is that global growth remains unbalanced and subdued. The IMF is constantly revising its growth projections downwards. While many predicted we would be out of the woods by now, 2015 turned out to be the worst year in growth performance since the global financial crisis (GFC). At the apparently very successful 2014 G20 summit in Brisbane (Australia) world leaders agreed to increase global growth by 2 percentage points by 2018. In 2015 overall growth has declined 2%, which means that the gap to meet the agreed goal has already increased to 4%. 2016 has just started and looks bleak. Whispers of a possible global recession are getting louder. There are several reasons that explain this downturn, but perhaps the two most important ones are the slowdown in the Chinese economy, which has triggered a fall in commodity prices that is negatively affecting many emerging markets in Latin America and Africa, and has triggered unexpected spillover effects in Europe and the US. And the December 2015 interest rate hike by the US FED, which has triggered a massive outflow of capital away from the emerging markets (see Figure 1), and increased uncertainty on whether the timing of the tightening was right. At the time of writing, the global market sentiment has become again extremely bearish.

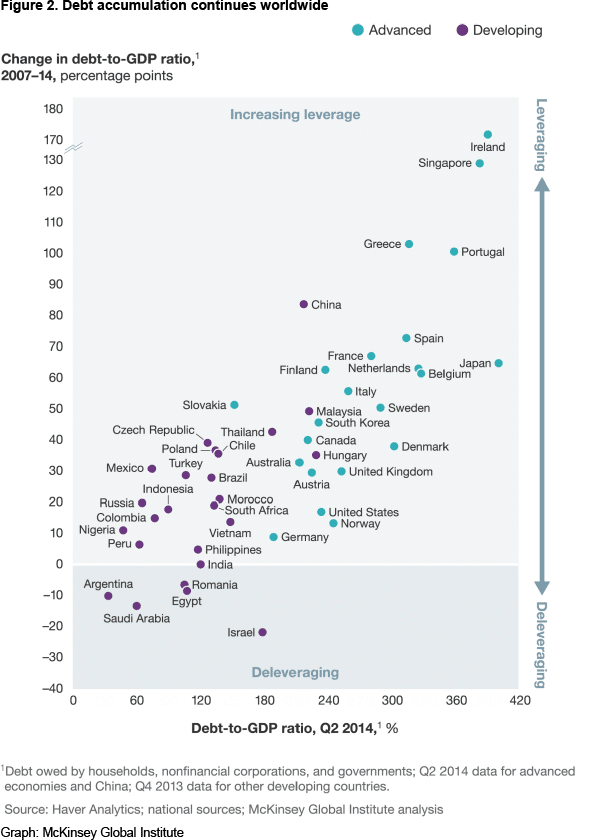

The recent steep falls in the stock markets show that the international financial markets are still very volatile, prone to herding effects and hence have the potential to cause new financial crises. Since the GFC, financial regulation has been tightened, but a number of voices have warned that these efforts are not enough to secure financial stability (Kirshner, 2014; Wolf, 2014; Turner, 2015). A number of financial risks remain: monetary policy continues to be ultra-expansionary in the developed world without a clear understanding of the mid- and long-term consequences of quantitative easing; large swings in capital flows have generated great instability; volatility in exchange rate and commodity prices persists, benefiting some countries and hurting others; the too-big-to-fail problem has not being solved; the expansion of the derivative markets and the shadow banking systems are another source of concern; and, most importantly, the massive accumulation of debt (both private and public) continues unabated (see Figure 2). Until the international community does not solve how to jointly reduce the volume of debt, from the US, to Greece and from Brazil to China and Japan, the levels of overall investment will continue to be disappointing and growth will be weak.

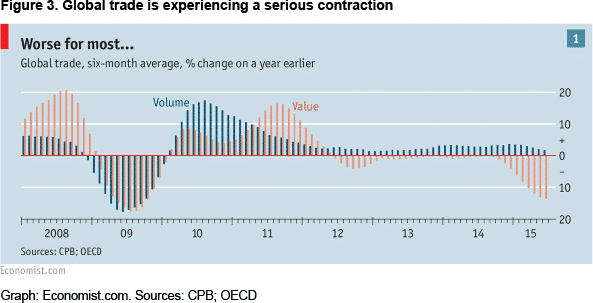

Unfortunately, risks are not limited to the financial sphere. In 2015 global trade declined the most since the GFC (see Figure 3). This is on the business side; on the governance side it is widely recognised that the WTO Doha Round is effectively paralysed and that hidden protectionist measures have increased (Evenett & Fritz, 2015). The new trend is to sign preferential trade agreements such as the Transpacific Partnership (TPP) and the Transatlantic Trade and Investment Partnership (TTIP), which for many undermine the global multilateral framework and have the potential of creating rival trade blocs. In addition, the effects of these agreements will only be visible in a few years’ time.

The current state of the advanced economies is better defined by what Larry Summers has called “secular stagnation”.1 In other words, despite negative interest rates, we have very low levels of investment and consumption (insufficient effective demand), weak growth, low productivity and relatively high unemployment and/or declining labour participation. This lack of dynamism in the developed world is at the same time affecting China, which is not able to transform its economy from export and investment-led to consumption-driven at a sufficiently fast pace to fill the gap in global demand left by the traditional US consumer of last resort. This in turn has led to massive overcapacity in many sectors and great uncertainty about the debt overhang, not only in China but across the world.

Given this worrying outlook, and the huge interdependences that exist in the global economy, multilateral cooperation should be the highest priority. The problem is that the new threats are not that punctual and clearly visible. Rather, they are protracted, structural and not easy to explain. This has dampened the sensation of urgency (at least until now) and discouraged bold joint action at the G20. This inactivity has fed two intertwined dangers: the return of protectionist and nationalist policies and the formation of rival blocs.

These two menaces relate to the structural power shift that we are witnessing from the West to the rest, more specifically from the US (and Europe) to China. The populations of the West are starting to be aware of this phenomenon and they are increasingly suspicious of the benefits of free trade and embracing political parties with an anti-globalisation agenda. In turn, they are also demanding a tougher approach vis-à-vis a rising China. Influenced by this social pressure, the US Congress has waited five years to approve the IMF quota reform that gives emerging markets a greater say in the organisation. This suspicion and unwillingness to change the current governance structures of the global economic order have encouraged the BRICS countries to strengthen their cooperation (the creation of the BRICS NEW Development Bank is the clearest manifestation of this) and China to establish the Asian Investment Infrastructure Bank (AIIB). Hence, the danger is the creation of two geopolitical and geoeconomic blocs. The BRICS led by China, on one side, and the advanced countries (including Japan) led by the US, on the other.

A number of European powers, including Spain, are concerned about this possible bloc formation and this is one of the reasons why they were keen to join the AIIB, despite diplomatic pressure from the US to do otherwise. Even the Asian Development Bank (ADB) has recognised that there is an US$8 trillion infrastructure gap in Asia. Therefore, there is a strong argument to be made that the AIIB is not a rival, but rather a complement to the Bretton Woods institutions. More competition between different multilateral development banks (MDBs) is not necessarily a bad think. The AIIB leadership knows that it needs to comply with Western standards of transparency, risk assessment and social and environmental awareness if it wants to be credible. But it can also learn from the mistakes of the established MDBs and consequently be more effective in promoting sustainable development. Although certainly not entirely transplantable to other parts of the world, the track record of China in fighting poverty is impressive. The Asian Development Bank has already noted the pressure of the newcomer and in its upcoming 2030 strategy it is likely to outline a series of substantial reforms in its structure and operations. Ultimately, this competition might lead to further specialisation and a healthy division of labour between the AIIB and the ADB.

Similarly, the IMF and the World Bank need to be further reformed. The Europeans have a clear understanding that the emerging powers need to have a bigger say, and following this logic, during the 2010 G20 presidency of South Korea, they agreed to lose two seats at the executive board of the IMF and see a vote transfer of around 6% in favour of the emerging countries. Spain, in particular, was very keen to see this reform happening because, incidentally, it is one of the few developed countries that will increase its quota. Over the past 40 years the centre of gravity of the world economy has shifted from the Atlantic, passed the Mediterranean and moved towards Asia (Quah, 2011), but coincidently in parallel to this trend Spain has also increased its GDP and per capita income significantly, and similarly to what happened to China, its newly acquired strengths have not been duly recognised in the governance structure of the Bretton Woods institutions.

At some point the Europeans, especially the Eurozoners, will have to accept that they are overrepresented and that the only way to keep their influence is to pool their weight in one single seat. This will not happen tomorrow (France and Germany are reluctant), but it is inevitable, at least from a Spanish perspective. However, while the Eurozone does not unite, Spain will understandably continue to defend its own national interests. Fortunately, after an intense diplomatic campaign, Spain obtained permanent invitee status at the G20. As mentioned above, the Spanish government acknowledges that Europe is already overrepresented and that on top of this the EU, which defends the interests of all its member states, has a permanent seat. Nonetheless, it is very important that Spain is around the table. Like South Korea (also a medium power with a population of around 50 million), Spain can play a vital bridging role between the developed and developing powers. Spain and South Korea are the only two countries within the G20 forum that have been able to overcome the middle-income trap in the past 40 years.

Sometimes it is forgotten that 40 years ago Spain’s per capita income was US$3.000, now it is around US$30.000 (Chislett, 2015). This is important because when it comes to discussing how to achieve economic and institutional progress, modern infrastructures and inclusive development. Spanish and Korean officials can draw from their own experiences and hence have more sympathy and understating for the challenges that policymakers in India, China, Indonesia or Brazil face today. Over the past years Spain has devoted (and will continue to devote) great efforts to overcome the ‘Great Recession’, to clean up its banking system, to reduce its debt levels, to transform its growth model, to fight corruption and inequality and reform its institutional framework. There are certainly a number of valuable experiences here that can be shared with the other participants of the G20.

Apart from being a bridge country, and therefore key to avoiding the formation of blocs, another contribution that Spain can offer to the G20 is that it is an ardent believer in the benefits of multilateral settings and agreements. Its strong commitment to multilateralism can be explained through its past. Spain enjoyed the privileges of being an empire, but also suffered the consequences of being an autarchic dictatorship. Through these up and downs it has learnt the benefits of pooling sovereignty upon the basis of shared interests and values. Spanish society is strongly in favour of an ever-closer union in the EU and deeper political integration in the Eurozone. As a current member of the UN Security Council, it is also convinced that the big challenges of our times, most of them transnational (such as economic globalisation, financial instability, climate change, jihadi terrorism, massive migration and cybersecurity), can only be tackled by strengthening international cooperation between the G20 powers and the rest of the UN members.

This is particularly evident in the fight against climate change. Spain has long ago acknowledged the risks associated to the emission of CO2 gases and it has made huge efforts to promote renewable energies. However, this is not enough. Pollution levels in many Spanish cities, especially in Barcelona and Madrid, are still too high, and our citizens are increasingly (and more vocally) demanding better air. Here again Spain, given that it developed later than other European countries –and therefore has acquired its environmental awareness more recently– can be a good source of shared experiences for the developing countries in the G20. Spain consumes more than 15% of its energy from renewable sources, which means that in the past decades it has acquired considerable expertise in the field. The same can also be said in areas such as the successful internationalisation of enterprises, the inclusion of females in the labour force, dealing with massive migration inflows and fighting terrorism.

As mentioned, the next few years will be marked by slow growth and greater geopolitical risks. In order to avoid further tensions due to uncoordinated unorthodox monetary policy, a new round of currency wars, possible debt defaults, lack of progress in dealing with the shadow banking systems, failure to stop the widening of inequality, more protectionist measures, geoeconomic border disputes and competing bloc formation, coordination and even cooperation at the G20 will have to be strengthened. The 2016 G20 presidency of China –the leading emerging market– is a good moment to do so. One cannot be naïve, however. Major agreements to solve the huge structural problems mentioned above are unlikely (a global debt restructuring conference, although desirable, is not going to happen any time soon, for instance), but concrete steps are certainly possible. The recent efforts, under the US leadership, to make tax havens more transparent and reduce international tax avoidance and evasion –although not as ambitious as demanded by some– are certainly a good example of how a multilateral approach can be successful.

This same more realistic, piecemeal strategy could be adopted in other fields. There could be concrete coordination, for example, in strengthening the global financial safety nets (Shafik, 2015). At the moment the IMF does not have the resources to deal with a potential balance of payments problem in any of the large emerging markets heavily indebted in dollars, let alone in a few of them simultaneously. Even China, which not long ago, with almost US$4 trillion in reserves, seemed rock solid, is losing US$100 billion every month and is starting to look increasingly vulnerable. More coordination, even if it is only ad hoc, also seems necessary in buffering exchange rate misalignments. Consensus exists on avoiding big swings in the major currencies. It is about time to design mechanisms to avoid them. If China needs a devaluation of its currency to release market pressure, this should be managed multilaterally. If current intense and herd-driven capital flows are perceived as too destabilising the G20 should agree specific guidelines on when capital controls are necessary, and perhaps even consider the introduction of a financial transaction or a financial activities tax, as proposed by the IMF (2010), in order to reduce the size and complexity of the financial sector. Finally, and perhaps more pressing in the current circumstances, G20 leaders might need to come up with a joint strategy to lift global growth. A second global recession in less than 10 years needs to be avoided.

Conclusions

Multilateral cooperation in global economic governance has always been difficult, especially in monetary and financial affairs, in which progress has been more limited than in international trade. National sovereignty in macroeconomic policies is paramount and world leaders take joint action only when the situation is extremely dramatic. The G20 has lost momentum since 2009 –the peak of the global financial crisis–. However, the general malaise in the world economy remains. Growth is weak, global trade is contracting, currency wars are increasing, geopolitical tensions are on the rise –so is nationalism and populism– and the formation of two opposing blocs led by the US and China is a looming threat. For a convinced multilateralist country such as Spain these are worrying developments. In a world less dominated by the US, major and binding agreements to establish fixed limits on global imbalances, exchange rate movements, avoid fragmentation in financial regulation, restructure sovereign debt and fight inequality are unlikely (Otero-Iglesias, 2015). But concrete steps in order to mitigate the negative consequences of these phenomena should be possible –especially now that the global economy is tanking–. In this regard, the Spanish government, as a permanent invitee to the G20 meetings, and the Elcano Royal Institute, as a new member of the Think Tank 20 (T20) network, will try to be reliable partners in proposing pragmatic solutions and in enhancing the multilateral dimension of the G20. We strongly believe that this is the only way to deliver common public goods.

Miguel Otero-Iglesias

Senior Analyst, Elcano Royal Institute | @miotei

References

Chislett, W. (2015), “Spain 40 years after General Franco: change of a nation”, ARI nr 66/2015, Elcano Royal Institute, Madrid.

Cohen, B. (2013), “The Coming Global Monetary (Dis)Order”, in David Held and Charles Roger (eds.), Global Governance at Risk, Polity Press.

Coyle, D. (2014), GDP: A Brief but Affectionate History, Princeton University Press, Princeton.

Evenett, S., and J. Fritz (2015), “The tide turns? Falling world trade and the G20”, VOX, 12/XI/2015.

Helleiner, E. (2014), The Status Quo Crisis, Oxford University Press, Oxford.

IMF, “Financial Sector Taxation: The IMF’s Report to the G20 and Background Material”, September.

Kirshner, J. (2014), “The Risk of Financial Crisis Remains high”, Forbes, 20/XI/2014.

Quah, D. (2011), “The Global Economy´s Shifting Centre of Gravity”, Global Policy, vol. 2, nr 1, p. 3-9.

Otero-Iglesias, M. (2015), The Euro, the Dollar and the Global Financial Crisis, Routledge, New York and London.

Shafik, M. (2015), “Fixing the global financial safety net: Lessons from central banking”, VOX, 5/X/2015.

Turner, A. (2015), Between Debt and the Devil, Princeton University Press, Princeton.

Wolf, M. (2014), The Shifts and the Shocks, Penguin, London and New York.

1 There are authors such as Diane Coyle (2014) who claim that the new technologies have dramatically transformed the world economy and unfortunately so far we are not able to measure the welfare and productivity gains that come with them. Hence under this new light the secular stagnation thesis is overstated. More research needs to be done in order to substantiate this claim.