Abstract

This is a long and dissenting review, in nine acts, of Ashoka Mody’s book EuroTragedy: A Drama in Nine Acts. It is based on a political economy approach, generally absent in the book. Mody’s work can be added to ‘The euro: it can’t happen, it’s a bad idea, it won’t last’ literature. It presents some fair criticism of the single currency and how the Eurozone authorities have (mis)handled the past crisis, but overall it is too one-sided in its dramatisation of the euro’s history, overlooking key events and the developments that first prompted the introduction of the euro and then made the euro stronger over the years. While Mody thinks the euro is economically illogical and therefore should be discarded, with Germany being the first country to leave, there is a strong consensus among political and business elites –and economists and political scientists on the continent– to retain it. Furthermore, after 20 years public support for the single currency is at its highest ever. There is no attempt by Mody to explain this, which is a pity because overall Mody makes the valid point that for the euro to survive it needs a legitimate political authority to sustain it. The problem is that he thinks that Europe cannot move forward, so he wants it to go backward.

Preamble

I was at first reluctant to read Ashoka Mody’s EuroTragedy. I knew his opinions on the European single currency from following him on Twitter, and I was not sure I wanted to read yet more ‘euro-bashing’ from a scholar based across the Atlantic. I still remembered the pain of reading Joseph Stiglitz’s The Euro: How a Common Currency Threatens the Future of Europe. But as a scholar of the euro you need to read everything that is relevant to the subject and Mody’s credentials cannot be doubted. He is currently Charles and Marie Robertson Professor in International Economic Policy at the Woodrow Wilson School at Princeton University and was previously Deputy Director at the IMF’s Research and European Departments, being responsible, among other things, for the design of the Irish financial rescue package of 2010-11. Thus, in principle, he is certainly knowledgeable about the workings of European monetary union.

The book also received many positive reviews. Foreign Affairs, The Economist and the Financial Times(publications that are often on my screen) considered it one of the best books of 2018, and as we are now celebrating (or lamenting, depending on where one stands) the 20th anniversary of the single currency, I thought it would be good to drop my prejudices and engage with Mody’s nine-act tragedy. Since the book is organised as if it were a play, I decided to follow suit and treat it like drama. Hence, the review is necessarily long, but aims to give the reader the chance to follow my train of thought as I soak in Mody’s story, which is intense and therefore very rich in detail and consequently deserves in-depth dissection. I believe this review can be useful not only for Eurozone scholars, experts and policymakers who have already read the book (quite likely since it is over a year old) but also for those who intend to read it. I think such a structure is also useful for students of European monetary integration. I will certainly ask the students at my courses on the subject to read the book (or at least certain passages) and then give them this working paper review so that they can see that it is possible to have two very different, and sometimes opposing, analyses of the same socio-economic and political phenomenon.

Introduction

While reading the introduction, I discovered early on that this would be another tome in the long list of works written by US (or US-based or educated) scholars and pundits that consider the euro’s creation economically irrational. Lars Jonung and Eoin Drea put it magnificently in a 2009 paper titled ‘The euro: it can’t happen, it’s a bad idea, it won’t last. US economists on EMU, 1989-2002’. Interestingly, 30 years on (1989-2019), the list keeps growing, and Mody’s book is the latest addition to the ‘euro-doom’ tower of scholarly work.

Another striking aspect is the missing parts. There is no engagement whatsoever with key concepts of the international political economy literature that has studied international monetary affairs for over 40 years, such as ‘international monetary power’ and the ‘dollar weapon’, also known in the economic literature as the ‘dollar shock’ (see my work on this). According to Mody, the creation of the euro was strictly an endogenous affair, without considering important, for some decisive, exogenous factors such as US dollar hegemony. As Randall Henning has wonderfully explained in his essential ‘Systemic conflict and regional monetary integration: the case of Europe’, the creation of the euro is above all a defensive move by the Europeans against the monetary power (including the dollar weapon) of the US. There is a strong consensus in the international political economy literature on the subject, with Benjamin J. Cohen –who has done the most to develop the concept of international monetary power over the years– in the lead. But even non-IPE scholars, who have chronicled the evolution of European monetary integration over the past decades, like David Marsh, include the US factor. It is striking that Mody does not.

Mody argues that there were no good economic or political reasons to create the euro and dismisses oft-cited arguments such as the common agriculture policy (CAP). He writes that this was not the reason for creating the euro because it was not written in any official documents. But this is misleading. With the erosion of the Bretton Woods system in the late 1960s, and the ultimate repudiation of it by the US in the 1970s, exchange rate volatility became the norm, so what the CAP needed was to have stable exchange rates. This explains the European obsession with the snake in the tunnel and the European Monetary System and the Exchange Rate Mechanism (ERM). Mody also says that the (irrational) fear of competitive devaluations could not be a reason, because that was not written in any of the documents either. However, one wonders whether the memory of the drama of the devaluations in the 1920s and 1930s was still so strong in the 1960s and 1970s that policymakers did not have to make a written reference to acknowledge its negative consequences. As Barry Eichengreen, perhaps the most renowned monetary historian of our times, has pointed out:

‘Europe, not the United States or Japan, was where floating currencies had been associated with hyperinflation in the 1920s. Europe was where the devaluations of the 1930s had most corroded good economic relations’ (p. 150).

In describing the reasons for further monetary cooperation in Europe, apart from, of course, pointing to instabilities from the dollar area, Eichengreen also highlights that ‘the desire to avoid jeopardizing the CAP, whose administration would be complicated by frequent and sizable exchange rate movements, was a source of support for the Werner Report’ (p. 151).

In finding logical reasons behind the creation of the euro, Mody also overlooks the desire of many peripheral countries, even France, to buy Germany’s price stability culture. Here the essential book is Kathleen McNamara’s The Currency of Ideas, which explains how in the 1980s and 1990s there was an emerging consensus among central bankers that the Bundesbank model was the one to follow and that it therefore made sense to regain part of the monetary sovereignty by creating a supranational central bank, thus having a seat at the table. Marsh (2011) refers to this as the way to overcome the ‘tyranny of the Mark’. In the same vein, there was also a strong desire in Europe, especially in France, to restrain or tame German power. This, again, is well explained not only in Marsh’s account but also in other works by well-known political economists and experts in EMU like Amy Verdun, and especially Kenneth Dyson and Kevin Featherstone in their fascinating Road to Maastricht. Helmut Kohl himself agreed with this taming strategy, as explained more recently by Thomas Klau.

At this point, when I had not even reached the first act, I was realising that Mody had overlooked most of the political economy literature that had been written on the euro in the past 20 years. I went straight to the bibliography and discovered that Henning and Marsh and Dyson and Featherstone were there but after checking the passages quoted I realised most of their references were marginal to Mody’s story. I also discovered that there was no mention of Erik Jones, Mathias Matthijs and Mark Blyth, Waltraud Schelkle, Nicolas Jabko, Manuela Moschella or Michele Chang. One could say: ‘it’s not fair, Mody is an economist so he doesn’t need to know the political economy literature on the euro’. That may be true, but then I checked for well-known economists, experts in EMU, and they were also absent from the bibliography. Big names like Guntram Wolff, Daniel Gros, Stefano Micossi, Isabel Schnabel, Sebastian Dullien, Nicolas Véron and Paul de Grauwe –for me the leading scholar on the subject, with a textbook on the Economics of Monetary Union that is in its 12th edition– were missing. Neither were there citations of important books on the euro written in recent years, like Pisani-Ferry’s The Euro Crisis and its Aftermath, Martin Sandbu’s Europe’s Orphan and Markus Brunnermeier et al.’s The Euro and the Battle of Ideas. Even giants in the field like Tommaso Padoa-Schioppa is only cited once, and certainly not on account of his most important work on the euro. It is certainly striking.

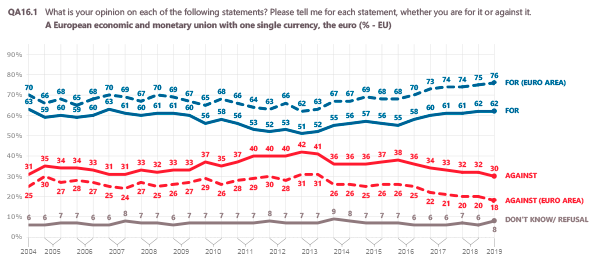

What was also surprising in the introduction was to see that there was no mention of the popular support for the euro that, according to Eurobarometer, is currently at historic highs, as it was already when Mody was writing the book (see Figure 1). There was also no mention in the introduction of some of the most important institutional innovations in the architecture of the EMU since the euro crisis of 2009-10. Incredibly, the European Stability Mechanism (ESM), the European equivalent of the IMF, and the banking union were absent in the short summary of the book’s key messages. It appeared that Mody was only focusing on the bad and not the good. Hence, having finished reading the introduction, I knew I was in for an ‘interesting’ play.

Miguel Otero-Iglesias

Senior Analyst at the Elcano Royal Institute, and Professor at the IE School of Global and Public Affairs | @miotei

1 I would like to thank Nicolas Véron for reading the whole text and providing valuable comments and suggestions.

Eurotower in Frankfurt, Germany. Photo: Michael Scheinost (CC BY-NC-ND 2.0)