Introduction

The Busan proposal for a “more effective cooperation” aims to overcome the limitations of official aid in achieving development goals. It frames, within the strategic framework of international cooperation, all public and private economic flows from both North and South that promote these goals. Private investment is included within these global funding flows for development; it plays a key role in promoting innovation, wealth creation, income, and employment. In order to realize the potential of the private sector and direct flows toward poverty reduction, the Busan Forum proposes to advance the “innovative mechanisms to mobilize private financing in favour of the shared development goals” (OECD, 2011).

In 2010, the Fondo de Promoción del Desarrollo (FONPRODE, Fund for the Promotion of Development) was created in Spain as a mechanism of Spanish development policy resulting from the reform of the Fondo de Ayuda al Desarrollo (Development Aid Fund). FONPRODE itself encompasses well–established mechanisms of cooperation such as budget support for the Fondo de Concesión de Microcréditos (Microcredit Fund) inherited from the Agencia Española de Cooperación Internacional para el Desarrollo, (AECID, Spanish Agency for International Cooperation for Development). One of FONPRODE’s purposes is the participation in small and medium enterprises (SMEs) of partner countries through financing mechanisms such as private equity funds. Thus, FONPRODE, along with many other development finance institutions (DFIs), becomes one of those innovative financing tools for development as defined by Busan.

Financing operations by FONPRODE and other DFIs are subject to financial analysis, like any other investment. Given that they are a tool for development cooperation, an analysis is also performed on their potential impact on development before approval is granted. This paper analyzes a selection of Colombian SME investments by private equity funds participated in by development finance institutions. The objective is to improve knowledge of the different effects that these investments can have on local development, and how such effects can be influenced by investors such as FONPRODE.[3]/[4]

This work is part of a research project by the Elcano Royal Institute on the impact of local investment supported by financial cooperation and foreign direct investment. The ultimate goal is to identify the aspects of investment that make a positive impact on development, thus drawing conclusions for public policy. More specifically in the case of FONPRODE, the aim is to contribute to the DFIs’ understanding of the socioeconomic effects of private investments and the factors that determine them, so that these institutions can improve their ability to make investment decisions for development. When applying this approach to FONPRODE and its participation in private equity funds, we must bear in mind that investment decision–making is actually a process consisting of three steps: an SME decides to invest its own and foreign capital in its expansion,; a private equity fund becomes part of the SME’s capital; and a DFI becomes part of the fund as an institutional investor.This document, the theoretical framework on which it is based, and the recommendations in this study are part of a project funded by the Spanish Agency of International Cooperation for Development.[5] The theoretical framework for analyzing the impact of local investment on development (Olivié et al., 2012) has identified the factors, mechanisms, and development processes that can be activated in financial cooperation and that ultimately impact the partner country’s development. These are analyzed for a selection of Colombian SMEs.

For this purpose, the research work was organized as desk work and as semi–structured interviews (Dexter, 2006) with more than fifty people, among whom were representatives of the Colombian administration, Colombian delegations of bilateral, multilateral, and institutional donors, private equity funds, and productive enterprises funded by financial cooperation. This fieldwork, conducted between April and June of 2012, had the support of the Colombian[6] Agencia Presidencial de Cooperación (Presidential Agency for Cooperation) and the collaboration of the Universidad de los Andes (University of the Andes), specifically of Linda Martinez and Juan Garcia in the collection of data regarding the activity of SMEs. In addition, a workshop co–organized with the University of the Andes was held in June 2012. Various stakeholders involved in financial cooperation in Colombia were able to discuss the preliminary results of this research.

Chart 1. Decision–making process

Although the object of this study is the SMEs and their impact on development, for the research to be politically relevant it is necessary to analyze the entire chain of financial cooperation, and how previous decisions taken by the various stakeholders affect the final outcome. This research seeks to find an answer to the following:

1. How an SME generates positive effects on local development through its investment;

2. How these effects are conditioned by the investment strategy of a fund and that of the DFIs participating in the fund.

In order to answer these questions, seven Colombian SME investments were examined along with five private equity funds and seven institutional investors involved in funding these SMEs. The bulk of the selected group is made up of SMEs financed by private equity funds in collaboration with DFIs such as the International Finance Corporation (IFC), the Inter–American Development Bank (IDB), the Corporación Andina de Fomento (CAF, Andean Corporation for the Promotion), and FONPRODE. SMEs with direct support from DFIs without mediation of a fund were also included, as well as SMEs funded without the participation of DFIs. Among the investors analyzed, two of them are ‘investors of impact’ of non–official cooperation but with development mandates (the AVINA and Clinton Foundations) and the Colombian development bank (BANCOLDEX). In some cases they operate together with DFIs, while in others they operate separately.

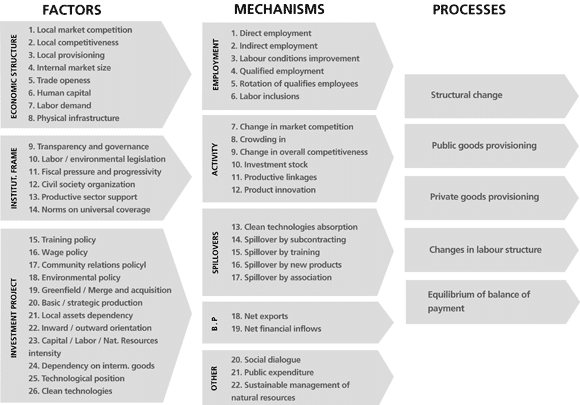

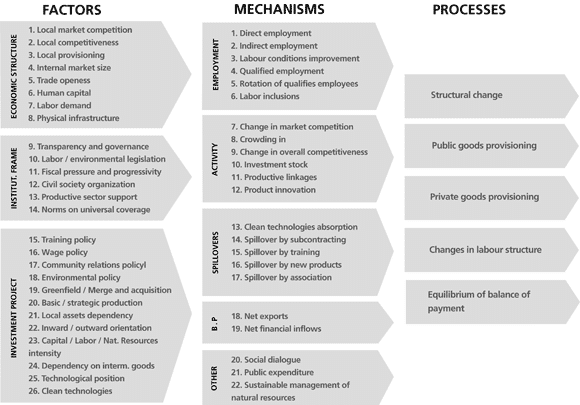

The development outcomes considered in this research are the 22 ‘mechanisms’ of the impact analysis framework of local investment on development (LID) in which this research was based (Olivié et al., 2012). These mechanisms are defined as sequences of events that contribute to the main processes of development of an economy: structural change, improving the provision of private goods, improving the provision of public goods, improving the labour structure, and equilibrium in the balance of payments.

Chart 2. Investment and Development, an analytical framework

Source: Olivié et al. (2012)

Considering that the first research question regards the way in which the effects on development are produced, and not simply what those effects are, the analytical framework also proposes a list of factors having to do with the type of investment and its institutional and economical framework. Different combinations of such factors, as presented in Annex 1, trigger different mechanisms.

Thus this paper analyzes the selected companies following the above mentioned theoretical framework. The first section of the document presents and analyzes the development outcome of the selected investments. The second and third sections analyze the influence that financial intermediaries and development investors have on these effects. The fourth section contains a proposal for the ex ante evaluation of these operations by development cooperation on the basis of the analytical research framework. Additionally, reference is made to other phases of the decision–making process of financial cooperation, where an analytical framework for private investment for development is equally useful. These phases take place before approval (the creation of strategic frameworks, identification of investment opportunities) and after approval (monitoring and evaluation). Finally, we end with a brief Conclusion.

Development outcomes from SMEs. Evidence from the field

The following seven Colombian SMEs were analyzed in this study[7]:

| Type of business | Activity | |

| 1 | Plastics industry | Plastic packaging industry for pharmaceuticals and cosmetics |

| 2 | Digital studios | 3D digital animation, mobile applications, video games, TV post–production and content development. |

| 3 | Agro–food industry | Fruit and vegetable processing plant for the production of pulp for juice products and the like. |

| 4 | Coffee distribution | Coffee distribution business with own supply chain and sales to supermarkets |

| 5 | Rural hotel | Hotel in a rural indigenous area |

| 6 | Internet shop | Retail chain of office automation services and telecommunications |

| 7 | Financial services | Factoring services for SMEs |

Interviews with these SMEs’ managers were structured around the LID framework mechanisms and factors; these made possible the identification of various types of investment depending on their impact on development. Investments were grouped by the type of impact that they have and are described by the following categories.

Investments that contribute to structural change

As a result of their technological and physical capital, some investments contribute to changing an economy’s pattern of production to favour better resource allocation and increased productivity. This contribution is greater when improvements occur not only within the company but are spread to other economic stakeholders (technological spillovers). Of the case studies, the digital studios and the plastics industry stand out for the contribution they make to structural change.The digital studios produce digital content for advertising and marketing, animation, and video games. Their business strategy is based on constant innovation supported by employee talent and continued development. The studios’ impact on development has to do with the spread of new information technologies by way of staff training, rotation into other companies, and collaboration with other SMEs and professionals in the communications and image industries, as well as with universities and other institutions. These mechanisms are made possible thanks to the technological superiority obtained through contact with the international industry, as well as to local human capital and the recruitment of specific foreign human resources within the permissible legal quota, to ensure a balance between the introduction of external knowledge and local ownership.As explained in the Prosperidad para Todos (Prosperity for All) National Development Plan, Colombia’s economy has a primary–export orientation, and structural change requires further investment in the industrial sector (and within that, a move towards technologically advanced industries). The plastics industry here examined is an SME producing plastic containers. Its technological content is relatively low, but the basis of its expansion is a specialization into products for the pharmaceutical and cosmetics industries, indicating a greater requirement for quality and precision than other sectors. Investment was directed towards improving production processes, product development, and training of its nearly one thousand employees. The technological externalities generated are not obvious, but this type of investment delivers productivity gains for the intensity of its capital.

Investments that promote productive linkages and indirect employment

Agribusiness and coffee distribution are investments that also favour structural change because they are part of a food production chain of higher added value than mere agricultural production. The effects they generate in their own supply chains are also to be highlighted.The coffee distribution business is an associate of the Federación Nacional de Cafeteros (National Federation of Coffee Growers) and the Fondo Nacional del Café (National Coffee Fund), which are public–private entities pursuing the development of the Colombian coffee sector. Expansion of the distribution business is based on the Juan Valdez coffee shop chain and production of a high–end coffee, and the business has developed a program to improve the capabilities of federated coffee growers. The purpose is to secure employment and improve productivity across the sector, otherwise subject to strong international competition.The agro–business company under study pioneered the development of certain food processing methods, mainly of fruits and vegetables, thereby channelling the produce of fruit growers who would not otherwise be able to trade their fresh produce. Colombia’s horticultural supply capabilities are very high, as is the potential of the processing industry to create indirect employment.

Investment with direct effects on employment

While the above mentioned investments had impact on indirect employment, other investments have direct effects, such as job creation, improvement of working conditions, and accessibility to formal employment for excluded groups. In the case of Colombia, these two mechanisms are of greater importance since low official unemployment rates conceal significant job insecurity and informality.For example: the rural hotel is currently under construction. It is in a remote, poor, and ecologically rich area with no quality hotels but with some demand for business, due to the proximity of a large mine, and with great potential for ecotourism. The hotel is located in an attractive environmental and cultural setting linked to the La Guajira region. It is expected that local people who have been excluded from the labour market will be employed by the hotel – the intensity of labour required by the hotel business favours this, while the low levels of local training play against it. But this latter concern is offset by the company’s staff development policy, with strong investment in training and social inclusion programs from NGOs and UNDP.The Internet shop provides internet, telephone, and virtual office services, acting as an intermediary in the communications market and focusing on the base of the pyramid. Similar services are provided in the informal market, but this company is intensive in job creation and offers formal employment contracts, training for employees with limited access to education, customer services training, and the opportunity to integrate into an organizational culture.

Investments that improve the provision of goods and services

Besides the impact on employees and suppliers, some investments encourage development through products and customers, improving the provision of goods and services. In this regard, two companies of the selected group stand out for their focus on the domestic market. Their business concept is to focus on neglected market niches through product innovation. This is understood not in terms of innovation to create new a product, but rather in product adaptation to the local context.One such company is the Internet shop which, as explained above, acquires computer and telephony equipment and then contracts associated services from large companies , offering these services to clients without private access to ICT.The financial company examined provides consultancy and liquidity services to small businesses using factoring operations. This is a market niche not covered by the big banks in the country. The financial success of this company is based on the development of its own risk assessment systems for the portfolios they access. It has developed technological tools for electronic factoring, which makes it possible to serve many small invoice discounting operations of small businesses with no access to credit.

Can an SME’s development outcome be anticipated?

The previous analysis and classification of SMEs clarifies the outcome to be expected from an investment by way of its contributing factors. For example, investments in labour–intensive activities, when accompanied by a training plan, responsible hiring policies, and adequate human capital, are suitable for investors who wish to contribute to development through employment creation (as in the internet shop example). When human capital is not sufficient, the investment can still provide an equally interesting opportunity if other development activities take place, such as social and labour integration programs (as in the rural hotel example).

Moreover, it should be noted that classifying these selected SMEs by their effect on development does not forbid certain investments from involving factors that lead to multiple types of effects. In this regard, the coffee distribution business is noteworthy. While its effects on the supply chain and contractors stand out, it also contributes to structural change (by adding value to coffee before export), to the equilibrium of the balance of payments (through exports), and to the development of new services within the upper tiers of the national market. Also, the business makes a special tax contribution to the National Coffee Fund.

Table 1. Seven Colombian SMEs supported by reimbursable cooperation. Development outcome analysis

| Coffee distribution business | Plastic packaging industry | Agroindustry | Digital studio | Rural hotel | Internet shop | Financial services |

| The company trades coffee from the Federación Nacional de Cafeteros, under the Juan Valdez brand, owned by the Fondo Nacional del Café. It has launched a range of premium coffees and the Juan Valdez coffee chain. | A plastic packaging company specializing in the higher quality segment (pharmaceuticals and cosmetics) through investment in its plant and personnel training. | Agro–processing fruits and vegetables, it complements the agribusiness value chain, generating direct and indirect jobs with products that with no transformation would have no commercial value. | Digital contents for advertising and marketing, animation and video games. Its business strategy is based on constant innovation through employee talent and training. | Hotel under construction in a remote, economically poor but ecologically rich area. This company is expected to integrate employ local people currently excluded from the labour market. | Internet, phone and virtual office services. It acts as an intermediary in the communications market, focusing on the base of the pyramid. . | Financial company offering advising and liquidity services to small businesses using factoring operations, A market niche not exploited by the big banks. |

| Mechanisms: development outcome from SME | ||||||

| Productive linkagesIndirect employmentSpillover by subcontractingIncrease in competitivenessImproving the commercial balance | Increase in competitivenessIncrease of investment stockImproving the commercial balance | Productive chainsIndirect employmentIncrease of investment stockProduct innovation | Product innovationCreation of qualified jobsSpillover by training and new productsImproving the commercial balance | Direct employmentImprovement of working conditionsLabour integrationSocial dialogueNatural resources management | Direct employmentImprovement of working conditionsProductive innovation | Product innovationTechnological spillover through new productsIncrease of competitionIncrease of competitiviness |

| Country factors: institutional and economic–structural features conditioning development outcome | ||||||

| Local competitivinessSupport to the productive sectorLocal provisioningMarket openness | Local competitivinessMarket competitionMarket openness | Local competitivinessMarket competitionMarket openness | Market competitionHuman capitalLabour demandCommercial openness | Labour and environmental legislationCivil society organization | Local provisioningDomestic market sizePhysical infrastructureLabour legislation | Domestic market size |

| Business factors: business features conditioning development outcome | ||||||

| Dependency on local assetsExternal orientationIntensity of intermediary goodsTechological superiority | Training policyIntensity of capitalTechnological superiorityExternal orientation | Intensity of intermediary goodsTechnological superiorityDependency on local assets | Training policyIntensity of capitalTecnological superiorityExternal orientation | Work intensityTraining policyNew plantDependency on local assetsCommunity relationsEnvironmental policy | Training policySalary policyStrategic productionInwards orientationLabour intensityIntensity of intermediary goods | Strategic productionInward orientationTechnological superiority |

Source: developed by the authors.

The influence of private equity funds in the investment–development nexus .

A few of the funds financing these selected SMEs have a development mission, but most, like the majority of funds registered in Colombia, have no explicit development goals. Rather, they seek profitable and secure investment opportunities (see Table 2). The investment strategies of these funds are so vaguely defined that it is difficult to assess what type of investments they actually promote. Others, meanwhile, specialize in very specific sectors, so that even when their development objectives are not stated, it is possible to anticipate likely effects of the investment fund. Based on the following two criteria, the mission and the investment focus, it is possible to differentiate three types of funds on the basis of their development outcome.

Funds with undefined investment focus

The vast majority of the funds examined define their investment focus with formulas such as “participating in companies with proven business models and volumes above 2.8 MUSD”; “to invest volumes below 1000 M COP in early growth stages”; “support clear business proposals in sectors with growth potential and barriers to enter them”; etc. This indicates the financial criteria governing their business, but there is no clarity on the possible alignment between their investments and the country’s development strategies.

These funds (Altra Investment, Aureos, and Escala Capital) base the management of their impact on development solely on the introduction of a number of responsible investment criteria into the regulations. These criteria are often adopted through the influence of DFIs; they respond to a “do no harm” approach and intend to avoid negative impacts on health, safety, and the environment. On one hand, these criteria serve to keep investment out of excluded sectors such as the military and pornography industries, and on the other hand, by following due diligence processes, they ensure that the SMEs operate legally and responsibly in terms of labour, the environment, and corporate governance. All this can help to avoid negative effects on development, but there is insufficient information on the type of positive effects that their investments could bring.[8]

In conclusion, it can be said that funds that lack a development mission or a sufficiently accurate investment focus can neither anticipate nor condition the development effects of their investments beyond avoiding certain negative effects.

Funds with defined investment focus

The Kandeo fund specializes in companies providing financial solutions to markets not served by traditional banks, which may result in a better provision of private goods and services. The financial sector can be considered a strategic sector, and the fund has a domestic market orientation (Colombian SMEs) and can combine local supply capacity (national savings) with its technological superiority (ICT tools and financial experience in other markets). These are all factors that, according to the LID framework, could have the following effects: product innovation and financial services, vertical technology spillovers, production chain with traditional banks, and increased competition in financial markets.

Such an investment strategy is aligned to the financial deepening goal included in the Colombian development plan and in many development agencies’ strategic papers. However, the Kandeo fund has no funding by any such development investors.

It should be noted that none of the funds analyzed has a geographically defined focus, which might be very interesting for development investors, especially in countries like Colombia with strong regional imbalances.

The impact of investment funds

The mission of the Fondo Inversor is to promote inclusive business in sales, purchases and capital, while the Fondo Acceso seeks positive effects on employment. These funds belong to a new stream of investors seeking not only financial returns but also social and environmental impacts, even at the expense of returns. These investors have generated what JP Morgan considers “new types of financial asset with an investment opportunity close to $400,000 billion and profit potential between $183 billion and $667 billion in the next decade” (Martin, 2012). Colombian funds of this type, Inversor and Acceso, have non–profit promoters like the Avina Foundation and the Clinton and Slim Foundations, respectively.

The Fondo Acceso is perhaps the clearest example of how it is possible to apply a framework of analysis like the one here employed to seek certain effects on development through private investment. Acceso aligns with the Clinton–Giustra strategy of inclusive growth for Latin America to promote human development by way of employment. To that end, it defines four objectives for the projects funded: direct job creation, indirect job creation, internalization,[9] and formalization of employment. Consequently, its investment focus is defined in terms of two key factors that trigger such mechanisms: employment–intensive businesses (e.g. the Internet shop network) and consumers of inputs from labour–intensive sectors (e.g. agribusiness).

Another feature of impact investment funds derived from their development orientation is their accountability system. The involved SMEs report to their investors not only about their financial performance, but their social and environmental performance as well. Other funds provide information on such social aspects only when requested to do so by their investors, generally DFIs. In these cases, the reporting is done less systematically and efficiently.

Within this common trait of impact funds, Inversor and Acceso differ for having launched two completely different tracking systems. The Acceso system is much simpler and defines four proprietary indicators: number of direct jobs created, estimated induced indirect jobs, number of jobs formalized, and number of autonomous jobs registered. The participation of the fund’s management in administering the SMEs ensures that these indicators are regularly met, and that they are added to the fund for the purpose of accounting to the investors. On the other hand, the investment fund has chosen to promote the Impact Reporting and Investment Standards system (IRIS), linked to the Global Impact Investment Network (GIIN) and supported by the Rockefeller Foundation. This system offers standard indicators by sector, which helps not only to define impact objectives but also to perform comparable and aggregate accounting. External consultants are also part of the system to perform an independent assessment.

Table 2. Analysis of funds: determining elements of the effects of investment on development

| Name | ALTRA | FORESTAL | AUREOS | INVERSOR | ESCALA | PROGRESA | ACCESO | KANDEO | |

| Investors | CDC (UK), FMO (Ne), SIFEM (Ch) | FINAGRO | CDC, IFC, Norfund, MFO, SIFEM, CAF, COFIDES and Corporación Mexicana (SEMIC). | AVINA, FOMIN, CAF and Bolsa de Colombia | CAF, IIC (IDB), Bancoldex | AECID, FOMIN, Bancoldex | Carlos Slim AC, Clinton Foundation, | Traditional investors only (pension funds, family offices) | |

| Development objectives | Not present | Not present | Not present | To favour inclusive business in production and sales, employment and suppliers or in the business capital | Not present | Not present | Social impact of the investment translated in job creation | Not present | |

| Focus | Sector | Sectors being restructured or growing | Commercial forestry plantations | Multisector | Multisector | Health, engineering for energy and hydrocarbons, agroindsutry, logistics and waste | TIC, life sciences, applied engineering | Agroindustrial, services at the base of the pyramid, industries intensive in job creation | Financial deepening: financial services for markets that are not exploited |

| Geography | Peru, Colombia | Colombia | Central America and Andes | Colombia | Colombia | Colombia | Colombia | Mexico, Peru, Colombia | |

| Type of business | Tested business models | Projects (not businesses) in association with the forestry operator and land owners | Volume between 5 – 1000 M USD / annual | Inclusive businesses | Growth capital: businesses with long track record and volumes above 2.8 M USD | Capital venture: business in initial development phase with volume below 1000 M COP | Sales between 0.5 and 1 M euros, with great growth potential and clear business proposal with entrance barriers | ||

| Code of conduct | Investment code with HSEQ, Health, Security, Environment and Quality. Exclusion list for sectors 1 | Not present | List of excluded sectors and expansion between environmental, social, and administration businesses | IRIS, Impact Reporting and Investment Standards. | The Fund code includes a section on the environment and social aspects (employment) | The Fund code includes a section on the environment and social aspects (employment) | In alignment with the Clinton–Giustra strategy of inclusive growth | In the process of adhering to PRI | |

| Monitoring and Impact evaluation | HSEQ annual report. Enviromental Footprint | Not present | Reporting on environment and social matters separately upon request from each development investor | Two tools for social impact measurement, IRIS and environmental: LEED (Leadership in Energy and Environmental Design) | Reporting on environment and social matters separately upon request from each development investor | Reporting on environment and social matters separately upon request from each development investor | Four qualitative objectives: number of direct, indirect, formalized, and internalized jobs. | Integrated IT system for follow–up of clients with depthening and impact | |

| Complimentary development actions | Tool kit and support from development investors on HSEQ | Not present | Inclusive business programmes of AVINA Fund | Development investors support the integration of environmental and social aspects in the code | Development investors support the integration of environmental and social aspects in the code | Strategic support of Clinton Fund | Clients can access multilateral cooperation credits |

Source: developed by the authors.

What is the development outcome sought by DFIs, and how do they achieve it?

The overall objective of access to finance and private sector development

The financial cooperation chains of the SMEs examined in Section 1 are initiated in seven institutional investors with development mandates. These include three multilateral stakeholders (the International Finance Corporation (IFC), which belongs to the World Bank Group, the Inter–American Development Bank (IDB), and the Corporación Andina de Fomento (CAF)); one bilateral donor (AECID, operating through FONPRODE); also BANCOLDEX, the development bank of Colombia; and two foundations (AVINA and the alliance between the Clinton and Carlos Slim Foundations).

Most of these investors (the multilateral funds and Colombia’s BANCOLDEX) frame these operations within a single development objective: the creation and consolidation of a capital–fund industry that promotes the development of the private sector. This approach is perfectly aligned with the main objectives of the “Prosperidad para Todos” National Development Plan. That plan considers access to financial services and the development of capital markets as transverse supporting mechanisms to the objectives of competitiveness and productivity growth. These, together with innovation and support to growth, define the strategy for sustainable growth and competitiveness.

In addition to this general objective, multilateral DFIs guide their decisions using three internationally agreed criteria: additionality, catalysis, and sustainability. Additionality is about being present where no other investors are; the catalytic effect is about leveraging other private and public capital; and sustainability has to do with the development of spaces that can be supported by national funding after divestment (Nathan, 2011).

AECID differentiates itself from the other investors analyzed in the way it connects with the development cooperation system, and through its integration into the institutional framework to ensure aid effectiveness. This can be an advantage in securing complementarities with non–reimbursable aid and alignment to the international cooperation strategy developed by the country. In the case of Colombia, this strategy is driven by the Agencia Presidencial de la Cooperción International (Presidential Agency for International Cooperation), which maintains an ongoing dialogue with AECID and other cooperation agencies but not with development banks and bilateral DFIs. In this regard, it is noteworthy that the participation of AECID in the first venture capital fund in the country (focusing on SMEs in the early stage of their business development), with a manager in the Antioquia region and not in the nation’s capital, is the result of a complementary program by the Universidad de Antioquia (University of Antioquia) to promote entrepreneurship (known as the ERICA program).

The adoption of codes of conduct

As discussed in Section 2, private equity funds have taken on board a series of management guidelines to avoid undesirable effects on development. This responds largely to the influence of DFIs with extensive experience in financing projects in developing countries, as well as learned lessons that favour the adoption of various codes of conduct. Some are specific to each institution and others are agreed upon internationally.

Among the internationally agreed–upon principles, the Equator Principles stand out. These are embedded in commercial and development banks but with a greater focus on project financing than on equity investment. The United Nations Principles for Responsible Investment (UNPRI), meanwhile, target the entire financial community, but these offer only a minimum commitment of a procedural nature for the integration of environmental, social, and governance matters. Another way of financing decisions to avoid negative effects is through the establishment of exclusion lists, such as that of the International Finance Corporation (IFC), which serves as a reference for many other development investors.

In the case of Colombia, it is noteworthy that BANCOLDEX, the main investor in the country’s development, has adopted certain principles regarding the prevention of money laundering and terrorist financing, and these principles have been integrated into the due diligence audits performed to private equity funds. Influenced by the IDB, BANCOLDEX has also included environmental–impact criteria.

Monitoring and evaluation

The examined multilateral DFIs have shown well–defined monitoring and evaluation routines that are implemented internationally. These are among their main tools for guiding management towards development results. The routines are based on standard indicator lists (DOTS in the case of IFC, and national official indicators in the case of the IDB). The most relevant are chosen for each operation before it is approved, and they are incorporated into annual monitoring reports for their governing bodies. Occasionally, reporting is completed via the engaging of external auditors; however, there is no evidence in Colombia of an evaluation specifically focused on capital transactions within development cooperation.[10]

Although from the procedural point of view these monitoring and evaluation systems are highly developed, from the conceptual point of view, they are limited to financial issues as shown in Table 3. This table shows the indicators used by IFC to measure the impact on development of their investments through financial intermediaries. This is perfectly consistent with what was explained at the beginning of this section: development financial institutions usually frame their participation in capital in the financial sector as part of an overall strategy to develop the private sector, and without pursuing specific effects of productive investments that are ultimately implemented thanks to the funds. DFI’s expect that such an outcome will not conflict with other development objectives of the country.

Table 3. DOTS indicators for the financial sector

| INDICATOR_ID | INDICATOR_TITLE |

| 105 | ROE (%) – Life of Project |

| 15 | ROE (%) – Annual |

| 149 | Portfolio Quality (% NPLs) |

| 2309 | EROE – Life of Project |

| 11 | EROE (%)- Annual |

| 236 | E&S Management Systems (Y/N) |

| 31 | Community Development Outlay ($) and (#) |

| 3469 | Access to Finance: New Loans and Outstanding Portfolio/SME/Microfinance |

| 3469 | Access to Finance: New Loans and Outstanding Portfolio/Microfinance |

| 3470 | Access to Finance for Women: New Loans and Outstanding Portfolio/Microfinance/Gender Finance |

| 2890 | Access to Insurance: Policies and Premiums |

| 2891 | Access to Insurance: Clients Insured |

| 2892 | Access to Insurance: Reinsurance Agreements and Premiums |

Source: DOTS indicators of the International Finance Corporation (IFC), available on www.ifc.org

It should be noted that DOTS and similar tools (such as GPR, used by FONPRODE) contain indicators that measure real effects on the economy. However, these indicators are used in direct investments by development institutions, and not in cases of investment through financial intermediaries. For example, when IFC invests directly in a food–chain company, as in the example case of the coffee distribution business, it intends to monitor and evaluate ex ante and ex post variables such as the number of jobs created, the national purchasing volume, or the number of farmers reached.

Table 4. Agroindustry sector, DOTS indicators

| INDICATOR_ID | INDICATOR_TITLE |

| 104 | FRR (%) – Life of Project |

| 106 | ROIC (%) – Life of Project |

| 15 | ROIC (%) – Annual |

| 166 | Project Cost ($M) and Completion Date |

| 103 | ERR (%) – Life of Project |

| 102 | EROIC (%) – Life of Project |

| 12 | EROIC (%) – Annual |

| 254 | Employment (#) |

| 197 | Taxes and Other Payments ($M) |

| 267 | Purchases from National suppliers ($M) and (MT) |

| 192 | M/SMEs Reached (#) |

| 52 | Farmers Reached (#) |

| 194 | Subsidies Received ($M) |

| 236 | E&S Management Systems (Y/N) |

| 229 | Resettlement (#) and Livelihood Restoration (#) |

| 31 | Community Development Outlay ($) and (#) |

How to manage capital investment tools in a more strategic manner? The case of impact investment funds

Investment approaches such as those mentioned above are considered to be of a low order of accuracy by Eurodad, a network of European NGOs for advocacy on debt and development, which recently published a report claiming that “public authorities must fulfil their responsibility by ensuring that the taxpayers’ money is channelled to businesses that can deliver the best possible developmental outcomes, such as the creation of decent work or the payment of taxes” (Kwakkenbos, 2012). Also, some financial institutions have engaged in self–criticism along the same lines. In the UK, for example, the role of CDC is being reviewed by the Department for International Development (DFID) in order to “radically increase their impact on development” (Nathan, 2011); and in Sweden, two assessments performed by the government question the additionality of their IFD Swedfund (Kwakkenbos, 2012).

In the field of private investment, so–called responsible investing (which focuses on minimizing the negative impacts of an investment) has been overtaken by impact investment proposals (which seek positive and tangible social and environmental returns). The Fondo Inversor in Colombia seeks to invest in inclusive businesses, and this case study has confirmed how one of its investments, the rural hotel, qualifies as promoting the employment of excluded groups. The Fondo Acceso, on the other hand, aims to contribute to development through employment and, based on the information obtained, their two investments under analysis have achieved that goal: the Internet cafe creates a relatively large number of jobs while the agribusiness company does so indirectly, drawing supplies from small fruit producers in the local market;.

The proliferation of such proposals by fund management agencies would enable DFIs to more easily recognize investment policies aligned with the cooperation strategies of their governments, and to improve the management of the impact on development. However, these funds are still in their infancy and probably lack the capacity to channel the entirety of DFI funding. Moreover, the fact that traditional funds do not seek explicit developmental objectives does not mean that their investments do not favour certain developmental effects. As pointed out in the case of the Kandeo Fund, its investment strategy is perfectly aligned with financial deepening strategies of the development cooperation stakeholders. Therefore, the DFIs’ strategic management for participation in capital funds depend much less on the fund having a developmental mission than on the investment strategy being precise enough to render its effects predictable, thereby making the decision to invest valuable in terms of development.

Table 5. Institutional investors with a development mandate in Colombia

| Name | IFC | IDB | CAF | Bancoldex | AVINA | AECID |

| Fund participation | Tribeca, Ashmore, Aureos | Escala | Escala, Aureos, Inversor | PROGRESA, ESCALA | INVERSOR | PROGRESA Capital |

| Development objectives | Access to finances framed in a WB country´s strategy, aligned with the Plan Nacional de Desarrollo Prosperidad para Todos | Access to finances | Development of the corporate and financial sectors | Creation and consolidation of the industry and additional investors in line with the strategy of access to financing of Plan Prosperidad para Todos | Supports the creation and expansion of business with a threefold approach: economic, social, and environmental so that inclusive markets can become a strength in the economy of Latin America. | Inclusive economic growth, respectful of the environment and the communities’ cultural identity, it does not put at risk food security and it focuses on the reduction of poverty and inequality. |

| Focus | Financial markets in general | Entities such as Bancoldex | Big financial mechanisms in the private sector, complements CAF´s technical assistance | The private capital funds industry in general. Industry and Services industry | Financial mechanisms of inclusive business as a pilot experience | Risk capital. Regions affected by conflict |

| Monitoring and evaluation | Inclusion in the annual report of development indicators in accordance with standards by the IFC sector (DOTS). 5–year evaluation of the Independent Evaluation Group | Indicators and national systems (Plan Nacional de Desarrollo and Departamento Nacional de Planeación). IDB development effectiveness frame. In charge of evaluation to Bancoldex | Macroeconomic indicators. Do not measure impact of projects but the development of sectors and regions where they cooperate | Number of agreements made. Volume of complimentary resources mobilized. Businesses informed regarding the mechanisms | GPR tool for ex ante evaluation of capital operations from FONPRODE, including indicators of impact on development | |

| Code of conduct | Ecuador Principles | Ecuador Principles | Exclusion list | IFC exclusion list. Principles of money laundering and financing of terrorism. Environmental terrorism | FONPRODE responsible financing code | |

| Complementary actions | Non–reimbursable aid for consultancy services regarding access to financing, improvement of the business context and other topics related to a country´s strategy | Technical assistance for environmental management | Technical assistance for the development of the corporate sector | Implementation of good environmental practices with the IDB. Informative actions about the FCP strategic sectors | Open competition for business plans, knowledge networks and other financing mechanisms: “angel” investors, seed capital, SME credits | ERICA, business spin off program at Universidad de Antioquia supported by Spanish Cooperation |

Source: developed by the authors.

A proposal for an ex ante development assessment of equity operations.

The challenge of optimizing the impact on development of reimbursable aid directed to the private sector is still pending, as explained above. Codes of conduct do prevent negative impacts but do not help to identify positive impacts. Impact investment funds pursue certain positive social and environmental returns, but they are isolated proposals, still in an early stage. Monitoring tools deployed by multilateral cooperation efforts offer good indicators and procedures for reporting back, but so far these have only served to measure effects in the financial sector, and not in the real sector of the economy.

Taking into account the monitoring limitations, and considering that the definition of indicators depends on the variables to be measured, the following analytical proposal aims to define and clarify a wider range of development outcomes following a business investment. This framework is based on the theoretical framework on the impact of local investment on development (LID) (Olivié et al., 2012).

A framework to define private sector development strategies

The LID framework proposes a list of 22 effects of investment on development, mechanisms triggered by the company under certain factors. Such mechanisms are considered to have an incidence on socio–economic development:

Table 6. The effects of investment on development, mechanisms of the LID framework

In line with partnership agreements between donor and recipient countries, this list can be used to define the objectives of an overall strategy for private sector support and to develop a more precise geographic strategy. For example, in the case of Colombia, the “Prosperity for All” National Plan has goals related to technology, as the country is “considerably behind” in all economic sectors. “Compared with the United States, the average labour productivity is nearly 24%, and it is less than 20% in sectors that are major generators of employment such as trade, industry, and agriculture.” Thus there are three –technology– and capital–intensive areas that should be promoted to private investment, and these areas all have potential for technological spillovers on the rest of the sector. Moreover, the Estrategia Nacional de Cooperación Internacional (National Strategy for International Cooperation) of Colombia, a document in which the government sets strategic guidelines for foreign donors and proposes cooperation in solving productivity problems in the primary sector, suggests selective actions in agricultural sectors featuring particularly low competitiveness but high contributions to GDP. In terms of employment, the goals are consistent with this strategic framework in terms of qualitative effects, integration of certain groups, and improvement of working conditions rather than the creation of direct and indirect jobs.

As evidenced in section 3, where the strategic approaches of the various investors are compared, Spanish cooperation sets itself apart from other investors because it promotes investment through its cooperation agency, AECID. Once an analytical and strategic framework is defined, field staff are in the right position to include in the partnership framework suitable targets for reimbursable aid and to identify potential operations. The latter requires the Technical Cooperation Offices to expand knowledge and institutional relations in the economic and financial sectors.

How to identify inclusive growth effects in a business plan

Colombia is a country of medium–income category but with strong internal inequalities. Equity is a key dimension to consider in any development intervention, as economic improvement may even aggravate inequalities between socioeconomic strata. For example, given the duality of the economy, support for certain high–tech industries in the interest of structural change can concentrate exclusively on the more developed urban areas, with no benefits to the agricultural regions of the country, further deepening the differences between urban and rural classes. In some countries, these differences may be related to ethnic, geographic, or gender factors unfairly impacting access to the benefits delivered by economic development actions.

Although the LID framework contains some mechanisms that are inclusive in themselves, such as social dialogue and access to the labour market by excluded groups, in general terms, the framework systematizes economic effects generated by companies’ activities and does not specify how such effects are distributed among different groups. However, such proposal can be operationalized integrating pro poor criteria or regional economy goals. For this, it is sufficient to define mechanisms containing target groups for cooperation. For example, mechanisms such as productive linkages or indirect job creation can be transformed into productive linkages in rural areas or the indirect job creation for women. There are many possibilities in this regard, and they will depend on the circumstances of each country and the priorities of each investor.

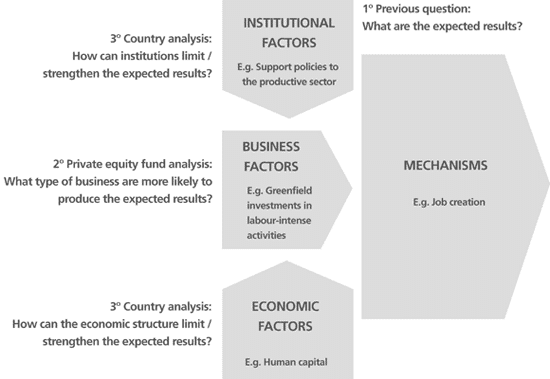

A framework for assessing ex ante investment proposals

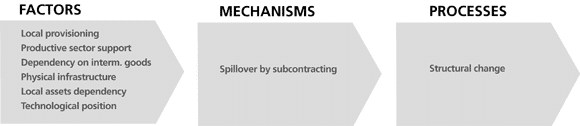

As shown in the diagrams in Annex 1, each of the mechanisms of the framework (for example, spillover resulting from supply chains) is determined by various factors. Some of them depend on the investor (e.g. technological position) and others on the country’s economy and institutions (e.g. local provisioning). Except in the case of impact investment, private equity proposals to DFIs do not take development outcome into account. Therefore, once the desired effects are defined, the factors included in such proposal should be evaluated in order to anticipate the possible effects on development.

For example, a DFI whose strategy is to contribute to improving the productivity of the country will aim to promote technological spillovers in the value chain within the territory. For that, it will focus on companies with relatively superior technologies and a high dependency in intermediary goods; otherwise, their links to local suppliers will not be relevant. If possible it will also aim to promote companies with some dependence on local assets, as to ensure value chains within the territory. Moreover, for the proposal to be viable, the local economy should have sufficient provisioning capabilities, an infrastructure that enables suppliers and customers to connect with each other and, ideally, support policies for the manufacturing sector in question, especially if provisioning capabilities are not entirely guaranteed. The above factors were present in the coffee distribution business and, in a country like Colombia, they could also exist in many agribusiness companies.

Chart 3. Combinations of factors determining spillovers by outsourcing

Continuing with the example, with respect to pro poor growth, it must be noted that if a particular region or social group have been set as a target for international cooperation, the economic and structural factors of that region or group must be assessed. For example, the coffee distribution business can generate spillover by outsourcing in the poorest areas of the country (where sourcing capabilities are located), but a digital studio that outsources technology services will rarely transfer knowledge outside of the country’s development poles.

That said, before investing in an equity fund the DFIs perform an evaluation, and they have no information about the companies to receive the funding. Therefore, as explained in section 3, it is necessary that the funds’ proposals already have a well–defined focus, or that such a focus be defined during the negotiation between intermediaries and investors. Once an analysis is performed on the investment focus and on the conditions necessary to produce the desired effects (company factors), it becomes possible to analyze how the characteristics of the country (including other development cooperation policies in place) will converge with the company characteristics to trigger development mechanisms (country factors). The chart below gives a general idea of this proposal. If implemented, it would have to rely on a combination of factors and mechanisms described in the analytical Annex.

Chart4. LID framework and questions of the ex ante assessment of investment proposals

A framework for the monitoring and evaluation of investment proposals

Once the desired effects of an investment have been defined from a conceptual standpoint, it makes sense to accompany these objectives with quantitative indicators that can give an approximate evaluation of their achievement. These should be based on information that is readily available and easy to add. This is the basis of a tracking system.

Like any development intervention, monitoring is effective when its procedure has been included in the design of the intervention and is integrated into its operation. The complication often arises when the activities have not been anticipated in advance. For FONPRODE’s equity investments, it should be borne in mind that the managers of the funds are also involved with the board of directors of the financed SMEs, and that AECID participates in the boards of directors of the funds taking part; therefore, the tracking of effects as they develop must be part of the reporting for reasons of financial control. The specifics to report (i.e. the development indicators) should be communicated from top to bottom at the time of signing of the various financing agreements.

Moreover, monitoring is more efficient when establishing shared indicators for different reporting systems. Does this mean that the standard indicators developed by the major donors facilitate tracking? According to the findings of this case study, the answer is negative. What constitutes a standard for an international organization, such as the IDB, it is not necessarily appropriate for a Colombian capital fund, because they have to handle standards for each DFI that participates in their capital. Consequently, it is more efficient to follow one of the two paths taken by the impact investment funds at work in Colombia. That is, either to define a few very simple indicators for the specific purpose of the fund in question (as is the case with Acceso), or to opt for a standard at SME level (as is the case with Inversor and IRIS). For an investor such as FONPRODE, it seems more reasonable to follow the example of Acceso and hope that the various proposals for measuring the impact on development converge into a true standard.

Regarding ex post evaluation, this proposal is primarily meant to clarify the evaluation of effectiveness according to the CAD evaluation criteria implemented within Spanish cooperation. The effectiveness, i.e. the degree of achievement of the specific objectives of a development intervention, should be valued on the basis of the achievement of the effects on development (mechanisms) which were defined during the process of investment approval. Additionally, the predefined combination of country factors, company factors, and mechanisms would be subject to relevant assessment. This must assess the quality of the design of the intervention and its relevancy to development strategies.

Conclusion

The FONPRODE, as a reimbursable aid instrument for private sector support, is innovative and can lever other public and private funding, from both North and South, towards businesses with effects on development and poverty reduction. This partnership approach has numerous precedents with other bilateral and multilateral donors, and it seems an appropriate response to the challenges faced by the international community at the recent Busan Forum. However, the evidence collected in this document, along with the analysis of certain civil society organizations and development finance institutions with longer track–records, highlights the difficulties in realizing this general approach for each discrete investment proposal. Development investors have a clear mandate to boost business activity through financial intermediaries and even to avoid certain negative effects of such activity. However, only in some cases do they pursue concrete and positive effects on the development of the country where they operate.

On the face of it, proposals proliferate for measuring effects on the development of business. Prior to the adoption of measurement tools, it is necessary to perform an analysis that allows specification of the expected effects and to choose those most suitable to the development agenda, the added value of each donor, and in particular the priorities of the recipient country. The conceptual proposal of this document would help to identify those targets at the initial moment a partnership framework is defined. It would also ensure the alignment of investment decisions with the development strategy of each partner country, notwithstanding that this conceptual precision would also help to improve the monitoring and evaluation of these interventions and the reporting of the assistance received. Spain, unlike other donors, has made FONPRODE part of the cooperation system and is therefore in a unique position to contribute to a more strategic management of repayable assistance to the private sector.

Iliana Olivié, Senior Analyst for International Cooperation and Development, Elcano Royal Institute.

Aitor Pérez, Associate Analyst, Elcano Royal Institute.

Bibliography

Cortés, Javier and Clara Pérez (2012), “Fondo para la Promoción del Desarrollo. Fonprode. Un instrumento al servicio de la Política de Desarrollo”, Revista Información Comercial Española (ICE) Enero–Febrero, nº 864. Ministerio de Economía y Competitividad, Madrid.

Dalberg Global Development Advisors (2011). The Growing Role of the Development Finance Institutions in International Development Policy . Second edition, 21 January.

DEG (2010). The Corporate–Policy Project Rating. (GPR). DEG KfW Bankengrupe. Colonia, Germany, February.

Dexter, Lewis A. (2006). Elite and Specialised Interviewing, ECPR Press, Colchester (UK).

Domínguez, Rafael and Sergio Tezanos (2012), “Donaciones y créditos concesionales: impacto en el desarrollo”, Revista Española de Desarrollo y Cooperación, nº 29, pgs. 119–154.

Ellmers, Bodo; Nuria Molina and Visa Tuominen (2010), Development Diverted: How the International Finance Corporation Fails to Reach the Poor, Eurodad, Brussels, December.

Kingombe, Christian (2011); Isabella Massa and Dirk Willem te Velde. Comparing Development Finance Institutions. Literature Review. Overseas Development Institute (ODI), London. February.

Kwakkenbos, Jeroen (2011). Private profit for public good? European Network on Debt and Development, Eurodad. Brussels.

Martin Cavanna, Javier (2012). “La cara más amable del sector financiero”, Revista Compromiso Empresarial, enero–febero. Nº 32. Fundación Compromiso y Transparencia, Madrid.

Massa, Isabella and te Velde, DirkWillem (2011). The role of development finance institutions in tackling global challenges. Project Briefing nº 65. Overseas Development Institute (ODI), London. September.

Nathan (2011). Literature review of development returns to DFIs investment in private enterprises, Department for International Development. Final Report. Nathan Associates INC, January.

Olivié, Iliana (2012), De la coherencia de políticas a la financiación global para el desarrollo: cómo superar el trabalenguas de la agenda política,Documento de trabajo del Real Instituto Elcano, Madrid, March.

Olivié, Iliana, Aitor Pérez and Carlos Macías (2012), Inversión local, cooperación financiera y desarrollo: reflexiones sobre el FONPRODE (DT), Documento de trabajo del Real Instituto Elcano, Madrid, March.

OECD (1992), Development Cooperation 1992 Report, Organization for Economic Cooperation and Development, Paris.

OECD (2006), Promoting Private Investment for Development, the Role of ODA. Organization for Economic Cooperation and Development, Paris.

OECD (2011), Second Draft Outcome for the Fourth High Level Forum on Aid Effectiveness, Busan, Korea, 29 November–1 December 2011, Proposal by the Co–Chairs, DCD/DAD/EFF(2011)11, Organization for Economic Cooperation and Development, Paris, September.

Olivié, Iliana; Carlos M. Macías and Aitor Pérez (2012), “Del do no harm a los factores pro–desarrollo económico en el apoyo a la inversión: apuntes para un mayor impacto de la cooperación financiera a través del FONPRODE”, Revista Información Comercial Española (ICE) Enero–Febrero, nº 864. Ministerio de Economía.

United Nations (2002), Report of the International Conference on Financing for Development, UN, Monterrey, March.

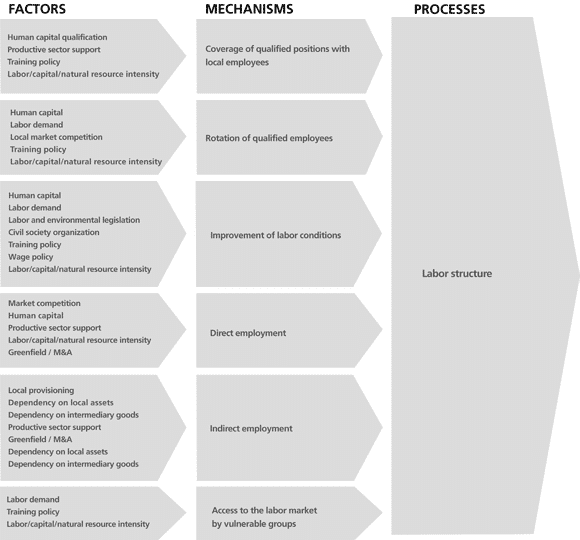

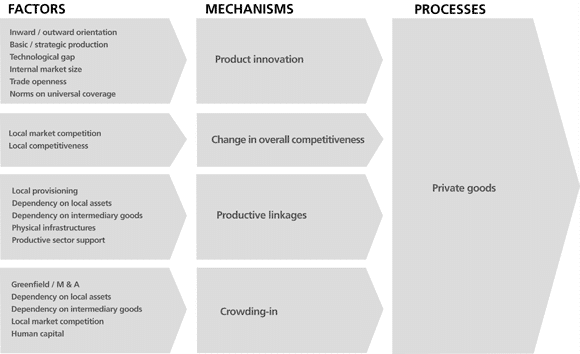

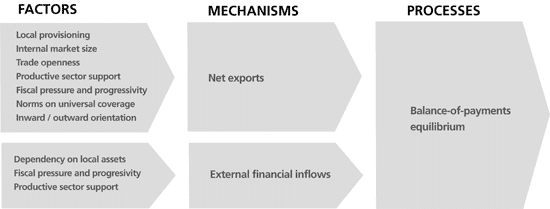

Annex 1. Analytical Framework

Overview: The investment and development analytical framework

Factors: those determining elements of a specific investment, the traits or characteristics of an investment as a whole, including both the investment company as well as the socio–economic structure in which it is inserted. Examples of factors are the intensity of labour that is required by the business or the availability of sufficiently trained human capital in a recipient’s country.

Mechanisms: sequences of events present in many different cases. These are triggered as a result of a combination of certain factors. A mechanism would be, for example, an improvement in working conditions, which could be explained by a combination of factors such as those in above example.

Processes: the ways in which investment generates positive effects on the development of the recipient country. These are the result of favourable operating mechanisms or a group of mechanisms. For example, an improvement in working conditions improves the country’s employment structure and, therefore, represents a step towards development.

Improving employment processes

Effects of investment in improving the employment structure

With new investment, the local economy can benefit from increased employment, better labour conditions that are advantageous for their workers, and more equitable access to employment:

- Creating skilled jobs

A new investment may result in the creation of new technical and management positions and therefore new opportunities for local labour to progress. - Rotation of qualified staff

If the company improves the training offered to staff, other sectors of the economy will be impacted through the rotation of staff. - Improvement in working conditions

Improving wages and other working conditions, and especially the overcoming of precarious and informal employment, is an expected effect of an advancing business. - Direct job creation

The creation of jobs in the invested company is already a mechanism for development. - Creation of indirect employment

Some investments that are not labour intensive can create indirect jobs if the activity makes demands on or complements other economic activities where labour is relatively more important. - Access to the labour market of excluded groups

Under certain circumstances, jobs created may be especially important from a development approach if they favour a fairer distribution of income and employment through access to the labour market of excluded groups.

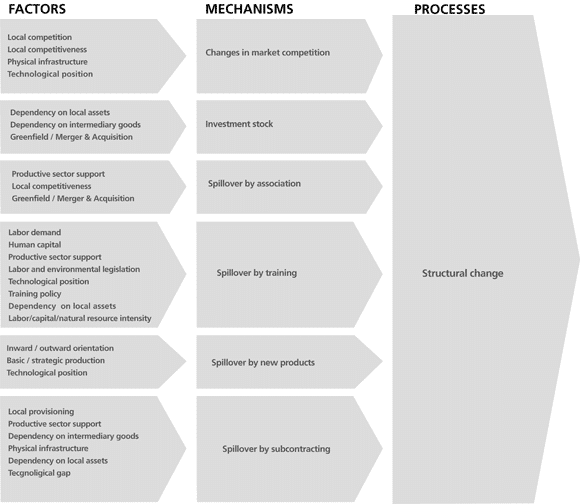

The process of structural change:

Effects of investment that promote structural change

Structural change is perhaps the most striking feature of any development process. It is defined as an economic transformation, supported by an increase of the total productivity of the factors, resulting in a situation where the ability to create wealth has been qualitatively improved and where the country’s competitiveness as a whole has been strengthened. Some effects or mechanisms contributing to structural change are:

- Improving competitiveness

Improving the company’s competitive position as a result of a new investment and competition forces improvement of competitiveness in the sector, and even in other sectors of the economy. - Increased investment stock

The new investment will often result in an increase of available capital, which is a key step to improving labour productivity. - Technological spillover by subcontracting

A new investment may lead to new production technologies, management, and marketing that often expand to the chain of suppliers due to requirements of the customer’s business. - Spillover technology by training

Socially, the workforce of the investment firm can spread technology, and it also can rotate to other firms. - Technological spillover by new products

The introduction of new and improved products, when they are directed to other companies, may also improve production and organizational improvements in client companies. - Technological Spillover by association

Companies with relatively advanced technology can collaborate with partner companies, governments, and other organizations to promote the expansion of technology.

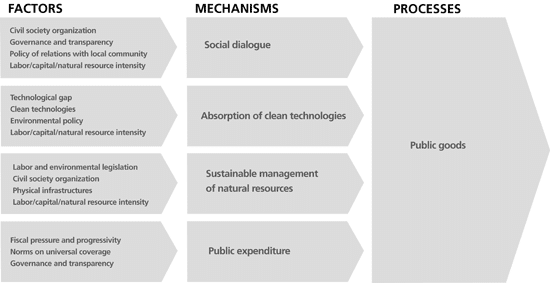

Provision of public goods process:

Investment effects that favour the provision of public goods

One of the processes that may promote DFI and that is most interesting from a social and environmental standpoint is the better and larger provision of public goods. This results from the strengthening of the capacities of the public sector to provide certain basic goods and services to the public, and from the sustainable management of environmental public goods.

The mechanisms that favour the provision of public goods are:

- Social dialogue

Corporate social dialogue with employees and other stakeholders facilitates the resolution of potential conflicts between private activity and collective interests. - Public spending

The company’s fiscal contribution under certain institutional conditions contributes to the financing of new or improved public services. - Absorption of clean technologies

It is remarkable that a technological change brought about by a new investment is environmentally more sustainable, and it will spread to other stakeholders in the economy. - Sustainable management of natural resources

A new economic activity may involve a new demand on scarce natural resources that requires socially and environmentally sustainable solutions.

Process provision of private goods:

Investment effects that contribute to a better provision of private goods

A new business investment is likely to increase production and supply of goods and services. The improvement of this offer would not only result from the company’s production but also from its impact on the market and on the private sector in general through its suppliers, competitors, and customers. The supply of private goods can acquire special importance for development when it meets basic needs, when the linkage with other industries is of strategic importance, or when the recipient of such goods is at the base of a country’s supply pyramid.

- Product innovation

The business activity may lead to an increase in the quality of private goods consumed in the country without involving a technological spillover. - Increased competition

The entrance or expansion of a new operator can have an impact in the sector’s level of competition as a whole. This impact is positive when the number of (or pressure on) competitors increases, and it is negative when it ends in a dominant market position. - Production chain

New investment in an activity can stimulate other activities in the economy through supplier–customer links. - Crowding–in

If the new investment leads to new business opportunities within the same or other complementary activities or subsidiaries, it can be expected that there will be new investors.

Equilibrium of the Balance of Payments process:

Investment effects that promote equilibrium in the balance of payments

Any business activity can affect the equilibrium of the balance of payments, either through trade or capital flows. The mechanisms enshrined in this process are:

- Net increase in capital inflows

Foreign investment in a company, followed by more capital flow (reinvestment, divestment, repatriation of dividends, etc.) and other debt transactions will have a net impact on the capital of the balance of payments. - Increased net exports

The SME’s balance between exports and imports resulting from the new investment will be its contribution to the trade balance.

Annex 2. Interviews conducted for the case study in Colombia

Institutions and number of people interviewed

| Investors: | ||

| BANCOLDEX | Bogota | 7 |

| Banco Interamericano de Inversiones | Bogota | 2 |

| Fondo Multilateral de Inversiones (FOMIN) | Bogota | 1 |

| International Finance Corporation | Bogota | 3 |

| AECID – OTC | Bogota | 2 |

| Corporación Andina de Fomento (CAF) | Bogota | 2 |

| Avina Foundation | Bogota | 1 |

| P4R | Madrid | 2 |

| Funds and financial intermediaries: | ||

| Altra Fund | Bogota | 2 |

| BANCOLOMBIA | Bogota | 3 |

| Inversor Fund | Bogota | 1 |

| Aureos Fund | Bogota | 1 |

| Forestal Fund | Bogota | 1 |

| Progresa Fund | Medellin | 1 |

| Escala Fund | Medellin | 1 |

| Acceso Fund | Bogota | 1 |

| Kandeo Fund | Bogota | 1 |

| SMEs: | ||

| SME 1: Coffee distribution business | 1 | |

| SME 2: Plastics industry | 1 | |

| SME 3: Agro–food industry | 1 | |

| SME 4: Digital studios | 1 | |

| SME 5: Rural hotel | 1 | |

| SME 6: Internet shop | 1 | |

| SME 7: Financial services | 1 | |

| Other: | ||

| Treasury Department | Bogota | 1 |

| Embassy of Spain – Economic and Commercial Department | Bogota | 1 |

| Embassy of Spain – Chancellery | Bogota | 1 |

| Industry and Commerce Office | Bogota | 1 |

| Chamber of Commerce of Colombia | Bogota | 2 |

[1] English version of ‘Los efectos en desarrollo de la ayuda reembolsable al sector privado: estudio de caso en Colombia’, DT 17/2012, Elcano Royal Institute, December.

[2] The authors thank Javier Cortés for his comments on this document; they have contributed decisively to improving its content.

[3] See Domínguez and Tezanos (2012) for an analysis of the debate concerning refundable cooperation vs. non–refundable cooperation and its impact on growth.

[4] See Olivié et al. (2012) for an academic, theoretical, and empirical literature review on financial cooperation, local investment, and development.

[5] Through an Open Permanent Call (Project 11–CAP1–0186).

[6] The authors are grateful for the support offered by Beatriz Mejía.

[7] To facilitate data collection, the interviews were conducted under non disclosure agreements in relation to the names of the companies in question

[8] See Olivié et al. (2010) regarding the differencesin approach in the management of the investment and its impact on development.

[9] The insourcing (as opposed to outsourcing) is about including in–house jobs performed by other companies or freelance professionals, which in the case of Colombia could mean that they were carried out by the informal sector.

[10] Colombia’s evaluation.