Theme: The trade negotiations between the EU and the US are motivated more by geopolitical than economic considerations.

Summary: Closing an ambitious accord on trade and investments could imply for the EU and the US both a boost to their economic growth and a recovery of their economic and geopolitical leadership, which has been increasingly questioned by the surge of the emerging powers. But it will not be easy going. It will be necessary not only to overcome domestic obstacles, linked to protectionist interests on both sides of the Atlantic, but also convince the emerging countries to accept the regulatory standards agreed upon by the EU and the US, something which is far from being assured.

Analysis

Introduction

Over the past 200 years the world economy has been dominated by the North Atlantic countries, First by Europe alone and then by Europe and the US (with a marked American leadership after WWII). However, over the next few years the loss of relative weight of the transatlantic axis in the world economy, which started two decades ago, is expected to speed up. The winners will be the new emerging powers, especially in Asia, but also in Latin America and Africa.

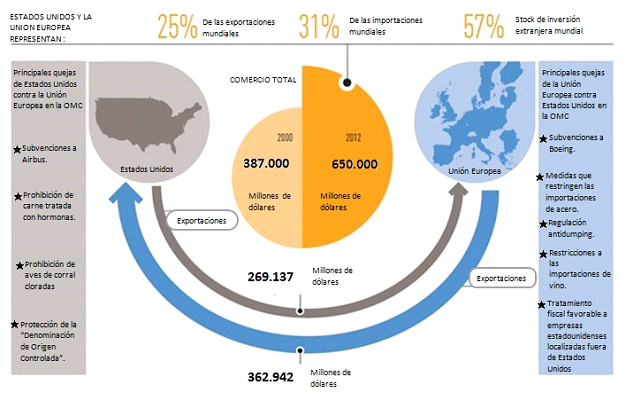

In view of this scenario, to which should be added that the Western economies are highly indebted and burdened by low economic growth, the EU and the US have opened negotiations to create a free trade and investment area (the TTIP) that will be the world’s largest, covering more than 40% of global GDP, a third of global trade flows (around US$ 650 billion per year) and almost 60% of global accumulated investment stocks (over US$3.7 trillion).

The aim of the negotiations is to create by 2015 a tariff-free integrated economic zone for manufactured and agricultural goods with a significant degree of regulatory harmonisation to facilitate cross-investment and the provision of services. It is not that tariffs are excessively high at present, but rather that the regulatory differences on the two sides of the Atlantic –which especially affect the trade in high added-value services– place significant hindrances to trade.

Although the EU and US authorities have emphasised the significant economic benefits such an agreement would give rise to, in this paper we maintain that the TTIP’s true purpose is geopolitical. On the one hand, it attempts to revitalise the transatlantic relation to counter the increasingly dominant narrative in international relations according to which the future belongs to the emerging nations and will be located in the Pacific basin. On the other hand, it aims to restore to the US and EU the power to establish the ground rules for the world economy which they enjoyed after WWII and which has steadily been eroded since then.

Nevertheless, the going will not be easy. First, it is necessary for the US and the EU to agree on the new rules for trade, which is difficult considering the different regulatory traditions on each side of the Atlantic. Secondly, even if they are able to negotiate an ambitious TTIP, there is no certainty that the emerging countries will conform to the rules, which might cause the world market to split into rival trade blocs and kill off an already weakened World Trade Organisation (WTO).

The Transatlantic economic relationship

The economic relations between the EU and the US are the world’s most intense and important. Although this close link was forged during the Cold War, the current phase of globalisation that began in the 1980s, along with the technological revolution that allowed the expansion of the trade in services, has intensified both trade and capital flows, leading to the (partial) integration of markets that until recent decades had been closed off to the outside.

After decades of successive rounds of trade liberalisation under the aegis of the GATT, today the transatlantic trade in goods is more open than ever, with applied tariffs below 4% on most manufactured goods, average waited tariffs of 2.8% and some higher tariffs in the agricultural and textile sectors. This has allowed the US to be the EU’s main trading partner and vice-versa. According to Eurostat data, in 2012 11.5% of European imported goods were from the US while 17.3% of the EU’s exports were directed at the US. For the US, the comparable figures are 15.8% and 16.5%, resulting in a trade balance favourable to Europe.

Furthermore, in the services markets, although incomplete on account of the regulatory barriers, the EU and the US have the world’s highest degree of integration between two economic blocs. Given the high allocation of capital per worker, the consumers’ high level of income and the legal certainty on both sides of the Atlantic, its natural that the trade in services is dominated by the higher value-added segments (financial, judicial and consultancy services, insurance, telecoms, etc) and supported by high levels of cross-investments. Thus, according to Eurostat data, in 2012 35% of the stock of US investments abroad were in the EU and 33% of European countries’ investments outside the EU were in the US, with the UK, Germany and France in the lead and Spain registering a significant growth.

Graph 1. Economic relations between the EU and the US

Source: based on Bertrand Largentaye .2013. ‘Challenges and prospects of a transatlantic free trade area’, Policy Paper nr 99, Notre Europe, p. 9.

In summary, despite the economic surge of the emerging economies, the US and the EU are still the big players in the international economic system, in addition to having the most fluid, intense and open bilateral trading and investment relations.

A friendly relation with limited integration

In general, the transatlantic economic relation has been relatively conflict-free. Beyond sporadic disputes (see Graphic 1), economic relations are easy. This is because both sides share the same ideas about how markets should operate, have liberalised and open economies and have fairly compatible interests, something which is not so evident between the West and the emerging nations.

Despite their strong economic links, the integration of the transatlantic market is far from complete. There is no single market with the free movement of goods, services and factors of production, which is the case both within the EU and between the states of the US. There remain significant non-tariff barriers because each side maintains its own regulatory autonomy on issues such as intellectual property, food safety, taxes, immigration, health and plant-health measures, audiovisual services, labour, accounting and financial legislation, and competition, energy and environmental policies. Examples of existing barriers are the auto and public procurement sectors. In the former, despite none too excessive tariffs, norms and standards (especially as regards security) on both sides of the Atlantic are very different, which effectively acts as a protectionist barrier. In the latter case, local or state rules, which are particularly important in the US, mean that an enormous market is practically closed to international competition.

The absence of harmonisation in the economic legislation and institutions of the two sides of the Atlantic is due to the continuing difference between the European and American economic models, a product of the difference in their citizens’ values and preferences, although this has not prevented a large volume of cross investments. Until a few years ago, the existence of these barriers, which naturally increase transaction costs and reduce economic efficiency but serve to preserve institutional sovereignty and the most entrenched social values, were never questioned. It was assumed that economic integration would not be complete because certain social costs had to be avoided; hence, no attempt was made to reduce the barriers, which for some were a case of unjustifiable ‘economic nationalism’ but to others a legitimate way of preserving national identity.

Nonetheless, as explained below, the new international economic and geopolitical scenario, with the swift rise of the emerging powers and a Western economy that is highly indebted, increasingly old, less dynamic and in clearly relative decline, has prompted the launching of the TTIP precisely to reduce the barriers to trade and investment that had so far had been considered acceptable or even desirable.

Thus, negotiations began in July 2013. The TTIP’s aim is to achieve a an ambitious accord based on tariff reduction and the convergence of standards to be closed during the course of 2015, which is the window of opportunity opening up after the elections in 2014 (both to the European Parliament and the US mid-term congressionals) and before the US presidentials in 2016. In fact, even if it proves to be impossible to reach an ambitious accord in the appointed time, the negotiators are well aware that for the TTIP to have a future it is essential to sign some sort of agreement in 2016 and to build on it after 2017.

The justification for the TTIP: it’s not the economy, it’s geopolitics

The main justification provided by the European and US authorities to launch the agreement is that it will generate growth and employment. According to a study by CEPR, commissioned by the European Commission, a broad and ambitious accord could generate €119 billion per year for the EU and €95 for the US, which would imply an average additional disposable income for each four-member family of €545 in the EU and €655 in the US (assuming its benefits are evenly spread over the total population and/or that the losers are compensated, which is most unlikely).

This increased income in Europe would be the result of a 28% rise in the export of goods and services from the EU to the US (equivalent to €187 billion annually), generating a total increase in trade volumes of 6% in the EU and of 8% in the US. Since tariffs are already low, 80% of the increase would derive from progress towards a transatlantic common market; ie, from the reduction of non-tariff barriers, especially the liberalisation of the trade in services and public procurement, as well as from simplifying administrative processes and homogenising regulations. This means that the TTIP is essentially about what is known in economics as positive integration (establishing new common rules) rather than negative integration (removing barriers to trade). It is therefore not an exercise in deregulation but rather the complete opposite. This is because the areas which stand to gain the most (services, investments and public procurement, for instance) are highly regulated on both sides of the Atlantic because they tend to have market faults that require public intervention, as in the case of the financial system or the food and pharmaceutical sectors.

Finally, the report predicts that the agreement’s impact on the rest of the world will be positive to the tune of €100 billion (trade generation will be greater than the diversion of trade), and that only between 0.2% and 0.5% of European workers will have to change jobs, while a large number of employment opportunities will be generated in a wide variety of sectors.

Although assessing the impact by country is even more difficult, according to a study by the Bertelsmann Stiftung, if a broad-based agreement is achieved the countries to benefoit most (in terms of an increase in per capita income) would be the UK, Sweden, Finland, Ireland and Spain, while France would benefit the least.

Beyond these forecasts being overoptimistic or falling short, they are not at all surprising: all international trade models predict that a reduction in trade barriers increases the consumer surplus, although they also highlight that a greater openness has a significant redistributive impact by giving rise to winners and losers, and the losers are hardly ever compensated. Furthermore, once countries attain a high income level and the weight of services in their GDP rises, the greatest trade gains precisely require the opening up of the services sector, which is one of the fundamental points of the TTIP. In summary, in a context of low transatlantic economic growth andlittle scope for increases in public expenditure to boost growth, trade liberalisation appears to be a good initiative. Although signing the TTIP will certainly not be sufficient to make the Great Recession something of the past or to resolve the problems of the European monetary union, the agreement can generate income gains at zero cost for the public treasury. And that, in itself, makes the TTIP a desirable initiative.

However, all these potential trade gains were also there 10 years ago and will likely be there in the future. Hence, the key question is: why the TTIP now? The answer is geopolitics.

The TTIP as a response to the emerging powers

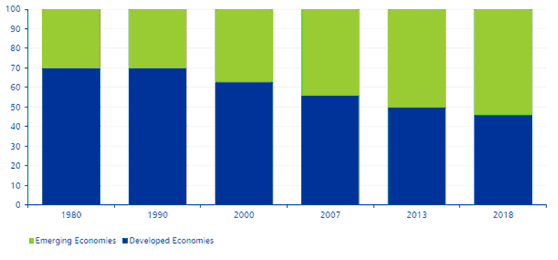

Over the past few decades, as economic globalisation spread and the emerging countries (especially the Asian ones) opened up to the world economy, the focal point of the international economy has slowly shifted from the Atlantic to the Pacific. At first these changes did not pose a challenge to the West’s political, economic and intellectual leadership: the newcomers were simply to adopt the rules imposed by the older powers. But, since the outbreak of the global financial crisis in 2007, and of the Great Recession that followed it, the process of convergence between the main emerging economies and the advanced countries has speeded up. While the former withstood the crisis quite well, the latter have become enmeshed in vicious circles of low growth and high debt, which hinder them (especially the Euro Zone) from retrieving the leadership they had in the past (Graph 2).

Graph 2. Contribution to world growth of the advanced and emerging countries, 1980-2018

Source: BBVA Research with IMF data.

Even the US, whose relative decline is far less than in most European countries and which could maintain its position as sole world superpower for decades due to its military hegemony, capacity for innovation and its recent energy revolution, has opted for starting a strategic withdrawal from international affairs. Thus, in the space of a few years the US and the EU have seen the legitimacy of their economic model questioned, their leadership in the world economy weakened, the international economic order they had designed contested and, more importantly in symbolic terms, a new narrative appearing, in which the future belongs to the emerging nations.

The TTIP, therefore, can be seen as part of the European and US reaction to their relative decline; ie, as an instrument to regain leadership and, therefore, acquire a greater influence in world affairs. The idea is to revitalise their power in an indirect way, without causing a conflict with the emerging countries, by establishing new ground rules in the economic sphere. As they did at the time of the GATT, the target is to redefine the world economic structure in accordance with their own rules, reflecting their own values and interests.

Nonetheless, they can no longer do so through their dominance over multilateral institutions like the WTO, whose Doha Round negotiations have stalled precisely because the emerging countries are no longer willing to accept the dictates of the advanced countries. The latter have therefore decided to attempt to forge common regulations for the sectors with the highest future growth potential, giving rise to a new and appetising transatlantic market that will simultaneously generate growth in their battered economies and, especially, become the most coveted market for exporters from the emerging nations, whose growth still depends to a significant degree on their sales to the rich countries. If the TTIP goes according to plan, the message for the emerging countries is clear: if you want to sell your products to my rich consumers you will have to accept my rules; if not, you will remain outside and your growth will be lower.

In fact, this geopolitical reading of the TTIP becomes even clearer bearing in mind that both the US and the EU have signed or are negotiating a large number of free trade agreements focused on services and investment with third countries. The most recent is the one the EU concluded with Canada in November 2013, which could be considered a precursos to the TTIP since Canada is already an advanced economy that already has a free trade agreement with the US (NAFTA, also including Mexico). But, furthermore, the EU has also signed an agreement with South Korea and is negotiating others with Japan and India, in addition to having a wide-ranging network of free trade agreements with emerging countries, particularly in Latin America (although in general these agreements do not cover many of the non-tariff barriers that are intended to be included in the TTIP).

For its part, the US, which also completed an agreement with South Korea in 2012 and has a large number of accords with Latin American and Arab countries, opened –a year before the TTIP– the negotiations for a Trans Pacific Partnership (TPP), which includes the major economies on both sides of the Pacific, including Japan but excluding China.

In sum, the US and the EU are at present leading a number of bilateral or regional mega agreements, both with advanced countries and with emerging nations that are sufficiently open to foreign direct investment and that are well established in the new global value chains, which today determine the patterns of world trade. All these accords aspire to a deep-seated integration, beyond merely tariffs, but always under the regulatory leadership of the US and the EU, which will always have a privileged position in the negotiations since in all cases the cost of non-agreement will be lighter for them than for their counterparts, given the appeal of their rich internal market.

If all the agreements are finally signed, and if they share more or less similar regulations and standards, it would not be difficult to multilateralise them in the WTO, since there would de facto be new rules for practically all world trade, whose model would be the TTIP. There would therefore be a WTO 2.0 that would have created new rules by mulilateralising the new regionalism under transatlantic leadership, thereby breaking the deadlock in which the organisation has been immersed for years precisely on account of the emerging countries’ refusal to accept this type of rules.

The plan could misfire

Using the TTIP as a lever to regain world economic leadership, and incidentally reviving the WTO, is no doubt an attractive proposition. However, the strategy could misfire, either because of an unsuccessful outcome to the negotiations on the TTIP itself, or because the reaction of the emerging economies is not what the transatlantic axis wishes for.

For the plan to be successful, it is necessary for the US and the EU to agree on new rules for trade and investment. Since the negotiation of the most intractable issues has been side-lined (the cultural industries, agricultural subsidies and part of the weapons industry), the achievement of an ambitious TTIP is feasible. Nevertheless, as the regulatory traditions on the two sides of the Atlantic are different, such a feat will be by no means automatic. In fact, since in economic terms the balance of power between the EU and the US is fairly even, neither will be able to force the other to adopt his own standards, mutual recognition is probably the best formula in order to make progress. But the EU well knows that even opting for mutual recognition rather than regulatory harmonisation, several decades were necessary to build its internal market. And, in services, this has still not yet been achieved.

Difficulties will put in an appearance at several levels. First, the resistance of the protectionist interest groups will have to be overcome in order to reduce tariffs to zero, which is likely to be more difficult for products that have high peak tariffs, such as dairy produce, sugar and cereals. Secondly, an unprecedented exercise in mutual trust will be indispensable to move forwards through mutual recognition, by which each party accepts as appropriate the control the other has over goods to protect the consumer. Only in that way will it be possible to liberalise sectors with complex safety rules such as the automotive and food industries. Additionally, in areas which still require regulations to be established (especially high value-added services, which will grow exponentially in future), it is vital for regulators to cooperate in forging new common –or at least compatible– rules. And, finally, the political commitment to reach an accord should be maintained at the highest level, although it might waver if incidents like the espionage case undermine the trust between the two parties and poison the bilateral relation.

But even if the TTIP is completed, nothing guarantees that the accord will open up a new era of globalisation under Western leadership. The emerging powers, especially China, India and the Latin American countries, have refused for years to accept rules at the WTO that restricted their scope for manoeuvre as regards industrial policies, which are precisely those that the TTIP will try to establish. Therefore, if by the time the TTIP is signed and up and running, their own markets are a major and growing portion of the world market, they may decide not to adopt the TTIP’s standards in order not to relinquish regulatory sovereignty, trusting that the opportunity cost of such a decision is not too high because their potential export growth in the transatlantic market is on the decrease. If such were the case, the TTIP would not become the model for new rules in world trade and would not be multilateralised through the WTO, but would be the beginning of a scenario of fragmentation in the international markets between large-scale rival trade blocs that would condemn the WTO –the institution that has so far best functioned tpo regulate globalisation– to irrelevance.

Conclusion: Closing an ambitious trade and investment accord could provide the EU and the US with a double dividend. On the one hand, and this matches the official discourse of both powers, the treaty could boost economic growth on both sides of the Atlantic. And, furthermore, at zero cost, which is especially important in the current scenario budgetary cuts. For this reason alone, the TTIP is a good idea. However, as shown in this paper, there is an unspoken reason why the transatlantic authorities have decided to launch the initiative at this moment: to restore economic and geopolitical leadership to a Western World that is increasingly concerned by the prevailing narrative in international relations according to which the future belongs to the emerging nations. And this can furthermore be achieved without a direct confrontation with the emerging powers but rather by re-writing the rules of international trade and investment, which are the infrastructure on which globalisation is built.

Thus, in as far as the TTIP manages to set the regulatory standards for the areas of trade and investment with the greatest potential for growth and only weakly regulated by the WTO, such as services, the protection of investments and technical and health standards, the emerging nations will be pressured to adopt them also in order to ensure their access to the transatlantic market. This would additionally allow a weather-beaten WTO to be revitalised but with a clear Western regulatory dominance.

The going, however, will not be easy. First, it will be necessary to overcome domestic transatlantic resistance to an ambitious accord and ensure all goes according to plan in 2015, before the US presidential elections. Secondly, once the agreement starts coming into force, it remains to be seen what the relative strengths of the advanced and emerging countries will be in the world economy, which will reveal how much elbow room the emerging nations will have to be able to turn their backs on the TTIP if they consider they can go it alone.

Federico Steinberg

Senior Analyst for the Economy at the Elcano Royal Institute and Lecturer at the Universidad Autónoma de Madrid