Original version in Spanish: La interdependencia de la economía británica: una contribución al debate sobre Brexit

Theme

It is not easy to justify the UK’s exit from the EU on the grounds of economic arguments.

Summary

This paper analyses the interdependence of the British economy, both in terms of trade and direct investment, in order to assess the economic justification of a hypothetical Brexit. It concludes that it is difficult to justify the UK’s leaving the EU on the basis of economic arguments. The British economy has extremely close economic ties with the other countries in the EU, which would be jeopardised if Brexit were to go ahead.

Analysis1

Introduction

The UK’s membership of the EU is up in the air. David Cameron, the British Prime Minister, has promised to renegotiate the terms of Britain’s adhesion to the Union, and will ask the electorate by means of a referendum if it wants the country to continue being a member state.

After several months of hard bargaining, Donald Tusk, the President of the European Council, presented a proposal to the leaders of the 28 countries that make up the EU. It was a proposal that found favour with Cameron, who acknowledged that the four headings under which his requests are grouped (economic governance, competitiveness, sovereignty and social benefits) had all received a response. According to the plan, the agreement reached at European Council meeting will lead to the referendum being held in June 2016.

Aside from the difficulties of the negotiation and the passions surrounding this debate in the UK, there is no doubt that since the country joined what was then the European Economic Community (EEC) in 1973 its economic ties with its European partners have done nothing but grow stronger. Using an interdependence index, the present authors seek to provide an objective measure of the economic relationship –in the broad sense of the term– between the UK and its principal partners (both within and outside the EU), in order to assess the economic advisability of the UK remaining in or abandoning the EU.

As we shall show in what follows, it seems clear that there is a weak economic foundation to justify the UK’s departure from the Union. Although there are variables that have not been included in our analysis, and although the UK could replace its membership of the Union with free-trade treaties and investment (in reality, as Jean-Claude Piris points out in a paper for the CER,2 Brexit could pave the way to a range of scenarios, and nobody really knows what the outcome would be), there can be no doubt that its exit would incur significant costs. The end of the free circulation of assets (goods, services, capital and workers) would entail the emergence of new barriers to economic exchange and the stability of the prevailing legal framework underpinning the internal market would be cast in doubt, which would assuredly restrict the UK’s economic flows with other EU countries, many of which are its principal trade and investment partners.

After setting out the methodology of the index, the article proceeds to analyse the interdependence of the British economy, both in terms of trade and direct investment. The authors’ intention is thus to set out objective data, to which we add certain reflections on the inadvisability of Brexit in the final section.

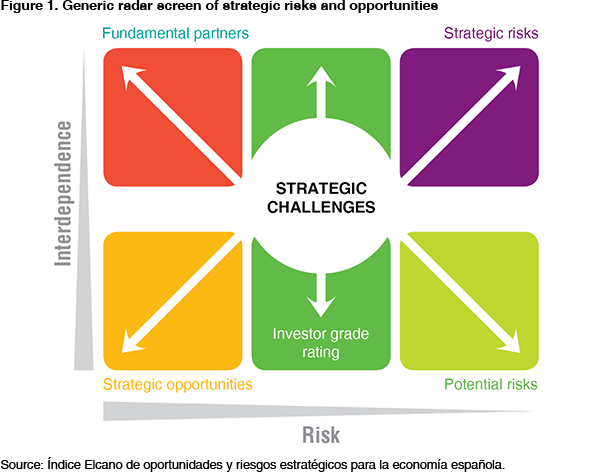

The Elcano Index of Strategic Opportunities and Risks

The Elcano Index of Strategic Opportunities and Risks was drawn up for the first time for the Spanish economy in 2005, and has been updated regularly ever since.3 This article develops it for the British economy. The index is configured on the basis of two elements: an index of economic interdependence (constructed using data for trade in goods and services, direct investment movements and stocks and cross-border banking flows) and an index of economic and political risk for all the other economies in the world. Both indices enable a map –or radar screen– of strategic opportunities and risks to be constructed depicting the importance and risk level of the 35 countries with which the British economy has the strongest relationships. As shown in Figure 1, each country is thus classified into one of the following categories:

- Fundamental partners: countries with which there is high degree of economic interdependence and that exhibit low levels of risk. In the case of these countries it is necessary to maintain the strong latticework of existing economic relations.

- Strategic opportunities: countries with lower levels of interdependence and low levels of risk. In the case of these countries it is necessary to strengthen economic relations.

- Strategic challenges: countries with various degrees of interdependence and greater levels of risk. Opportunities exist to strengthen economic relations with these countries, but they also require more attention, since they have the potential for developing both greater and lower levels of risk.

- Potential risks: countries with medium and low levels of interdependence and very high levels of risk. It would be preferable to reduce existing economic relations with these countries unless they generate an extremely high level of income that offsets the risk.

- Strategic risks: countries with high levels of interdependence and also high levels of risk. In the case of these less favourable economic partners it is imperative for economic relations to be reduced.

Deconstructing the interdependence of the British economy

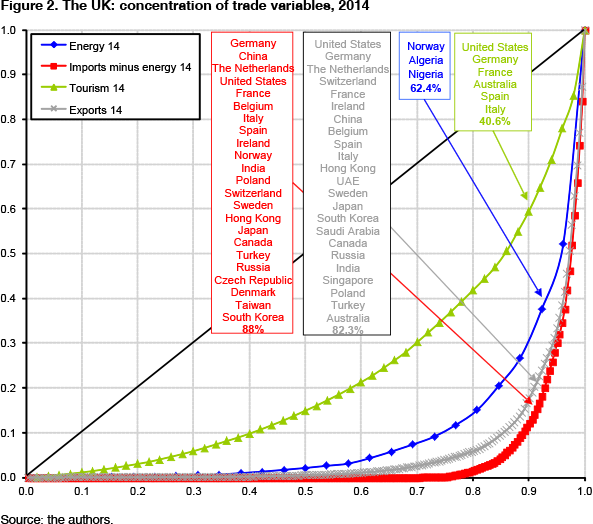

A limited number of countries dominate both the trade and the investment relations of the British economy, in particular the main EU countries and the US. In 2014, 23 countries received 82.3% of the UK’s exports in goods, while 23 countries accounted for 88% of its imports, 79% of energy purchases were made from five countries and 50% of tourism originated from five countries (see Figure 2). Both in terms of trade and in terms of energy imports it is thus evident that there is a high degree of concentration.

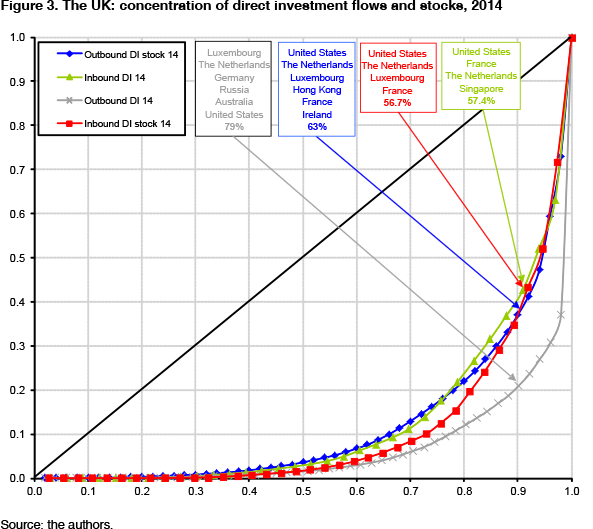

A similar picture emerges in the area of direct investments. Eleven countries received almost 88% of the outflows of foreign direct investment, while almost 82% of the direct investment received by the UK originated from just seven countries. This high degree of concentration in the flows of direct investment, both outgoing and incoming, is replicated in the case of stocks.

Up to 81% of the stock of inbound direct investment received by the UK originates from eight countries. There is a lower degree of concentration in the UK’s stock of outbound direct investment however: 78% is accounted for by 11 countries (see Figure 3).

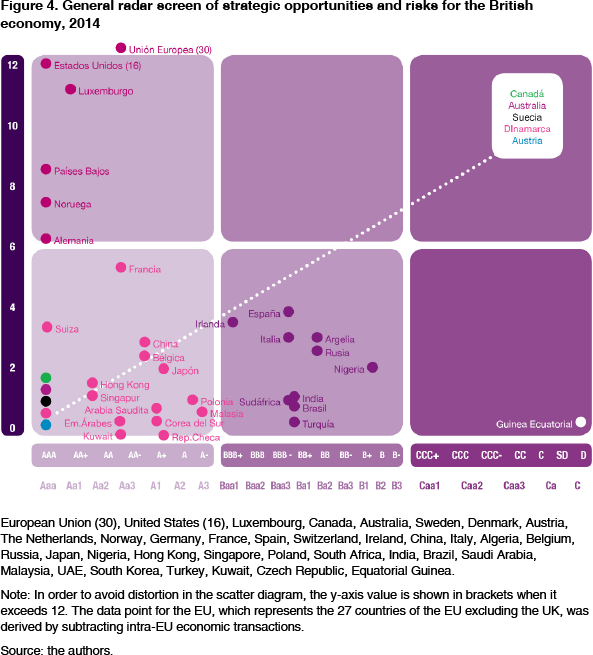

The general radar screen of strategic opportunities and risks for 2014 shows that the UK’s main economic partner, by a wide margin, consists of the other members of the EU. Whereas the 27 EU countries (28 minus the UK) have a value of 30 on the interdependence index, the UK’s second-largest economic partner, the US, only registers a figure of 16. According to the authors’ calculations therefore, the UK has almost double the economic activity with other EU countries when compared to the US, which is its main partner if the EU countries are counted separately and not as a bloc.

Located in the ‘fundamental partners’ section of the radar screen, in the north-west quadrant, are countries with which the UK has a high degree of interdependence and reduced levels of risk. In 2014 five countries constituted the UK’s fundamental partners: the US, Luxembourg, the Netherlands, Norway and Germany (see Figure 4). The US and Germany are fundamental partners for the British economy because they are the two main recipients of its exports; they are respectively the first and fourth most important sources of British imports and the main sources of tourist income. At the same time they are the main source countries for inbound direct investment, while being the most prominent recipients of the UK’s outbound direct investment. They therefore play a highly important role as recipient countries for the stock of direct investment undertaken by British companies, as well as being the source of inbound investments.

The high degree of interdependence with Norway reflects the considerable trade in oil, and to a lesser extent the existence of mutual direct investment. Interdependence with the Netherlands reaches very high levels due to the fact that the countries have important trading relationships. It also accounts for a significant share of income from tourism and above all a remarkable level of direct investment, both in terms of movements and stocks. Relations with Luxembourg, however, are an exclusive reflection of the high degree of interdependence in the field of direct investments, where Luxembourg provides a major financial platform for channelling international investment towards the UK and from the UK towards other final destination countries.

Located in the ‘strategic opportunities’ section are countries with which the British economy has established lower levels of interdependence compared with the ‘fundamental partners’, but which also have the attraction of exhibiting relatively low levels of risk; there is potential here for strengthening economic relations, whether in terms of trade or direct investment. An especially prominent country in this section is France, given that it is the fourth most interdependent country for UK trade while occupying the same position in terms of direct investment. In the middle part of ‘strategic opportunities’ one finds:

- From Europe: Switzerland and Belgium.

- From the Asia-Pacific basin: China, Hong Kong, Japan, Australia and Singapore.

- From North America: Canada.

It should be pointed out that Spain (with a level of interdependence exceeding China’s and the same as Switzerland’s), Ireland (ranking slightly below China) and Italy (with a level of interdependence with the UK exceeding Japan) would also be located in this part of the strategic opportunities region were it not for the deterioration in their risk ratings, stemming from the intensity of the eurozone crisis in recent years.

In Europe, the UK has established stable trade, tourism and direct investment links with Switzerland and Belgium. In the Asia-Pacific basin, interdependence with China is characterised by greater volumes of trade and to a lesser extent by direct investment; with Hong Kong, Japan, Australia and Singapore, however, the interdependence is mainly due to the greater volume of direct investment, with trading relations playing a secondary role, a pattern that is virtually replicated in the case of Canada.

This characteristic pattern of interdependence with Hong Kong, Japan, Australia and Canada is repeated in the case of interdependence with Spain but with an interesting variation. While there is a high degree of direct investment –with a level similar to that of Japan and Singapore and slightly lower than Canada– Spain also occupies a notable position in the ranking of trading partners, where Spain is the ninth most important country for the UK. In the case of Ireland and Italy the UK has a degree of interdependence similar to that of Spain in terms of both trading relations and direct investment. Ireland is the UK’s eighth-largest trading partner after Algeria and ranks slightly below China in direct investment; for its part, Italy is the UK’s 10th-largest trading partner, just behind Spain and at the same level as Nigeria, and in terms of direct investment it lies at the same level as Hong Kong and Russia and a long way behind Spain and Ireland.

In the lower part of ‘strategic opportunities’ there are three categories of country:

- A large group of EU countries: Sweden, Poland, Denmark, Austria and the Czech Republic.

- Saudi Arabia, the United Arab Emirates and Kuwait in the Middle East.

- South Korea and Malaysia in the Asia-Pacific basin.

The British economy’s interdependence with Sweden, Poland, Denmark and Austria has a twofold foundation based upon both trade and direct investment. The trade aspect is decisive in the case of relations with the Czech Republic. Interdependence with the three Middle East countries –Saudi Arabia, the United Arab Emirates and Kuwait–essentially rests on trade. Interdependence with South Korea has a twofold quality, resting both on trade and direct investment, while in the case of Malaysia it rests exclusively on trade.

The central section of the radar screen is where countries regarded as ‘strategic challenges’ are located; countries in this area exhibit levels of interdependence with the British economy similar to those of countries in the ‘strategic opportunities’ section but have higher levels of risk than the countries in the latter group. Located in this section are:

- Spain, Ireland and Italy, which, as explained above, are situated here owing to the deterioration in their risk ratings in the wake of the eurozone sovereign debt crisis. Little by little they are set to return to the ‘strategic opportunities’ region, however.

- Russia, Algeria and Nigeria, which exhibit a notable degree of interdependence owing mainly to trade links –by virtue of being energy exporters– but in the case of Russia, and to a lesser extent Nigeria, owing also to the direct investment undertaken by the UK.

- South Africa, India, Brazil and Turkey. The UK’s interdependence with South Africa, India and Brazil rests both on trade and direct investment, whereas in the case of Turkey it rests fundamentally on trade.

The area in the north-east quadrant of the radar screen is occupied by ‘strategic risks’. No countries are likely to be found in this section, because any country located here would exhibit both a high degree of interdependence with the British economy and a high level of risk.

Lastly, in the area occupying the south-east quadrant of the radar screen, consisting of ‘potential risks’, the only country to appear is Equatorial Guinea. In this case the interdependence rests on oil imports.

Implications for the Brexit debate

It is evident from this analysis of the interdependence of the British economy that the UK’s major trade and investment ties, apart from those with the US, are those with other EU economies, especially Germany, France and the Netherlands (the investment links with Luxembourg shown in these data are a reflection more of the latter’s role as a financial stepping-stone rather than actual direct investment). Indeed, the interdependence with Germany today is very similar to that described by Keynes in The Economic Consequences of the Peace regarding the relationship existing prior to World War I when he wrote that, ‘in our own case we sent more exports to Germany than any other country in the world except India, and we bought more from her than any other country in the world except the United States’. This is exactly the same scenario as exists today.

It is true that the US is the main economic partner of the UK and that the trade in oil with Norway (a non-EU country) is significant. The EU in its entirety, however, plays a far greater role in the UK’s economic flows than the US, and in many areas the relationship is characterised by positive feedback owing to the structure of the world’s supply chains. As indicated above, if the EU (excluding the UK) is taken as a whole, the volume of economic relations with the UK is almost twice that of the US.

As far as direct investment is concerned, the fact that EU members and non-member European countries (Switzerland and Norway) have constructed a significant degree of interdependence with the UK is undeniable, and taken as a whole they have achieved a level of interdependence approaching that of the US and Canada. But it is worth pointing out that the EU countries exhibit a degree of interdependence with the UK far exceeding that shown by the Asia-Pacific countries in their entirety.

Furthermore, there is no evidence whatsoever that Britain’s membership of the EU represents any barrier to British companies wishing to break into Asian markets, which are the most buoyant in the world. Indeed the UK can use its membership of the EU in a strategic manner to increase its exports and investments in these countries.

Conclusions

The importance of trading and investment relations, and the range of EU countries providing both fundamental partners and strategic opportunities for the UK, added to the fact that London is today the main financial trading centre for the euro (which would be difficult to preserve were the UK to leave the Union), undermine the economic justification for the British deciding to abandon the EU.

Alfredo Arahuetes

Professor at the ICADE Faculty of Economic and Business Sciences (Comillas Pontifical University) and Senior Research Fellow at the Elcano Royal Institute

Federico Steinberg

Senior Analyst at the Elcano Royal Institute and Professor at the Department of Economic Analysis, Autonomous University of Madrid | @SteinbergF

1 The authors would like to thank Robert Robinson, Aurora García Domonte and Carlos Martínez Ibarreta, from the Faculty of Economic and Business Sciences (ICADE) at the Universidad Pontificia Comillas for their valuable help in completing this pasper.

2 Jean Claude Piris (2016), “If the UK votes to leave”, Centre for European Reform, London, January.

3 See Federico Steinberg & Alfonso Arahuetes (2014), V Índice Elcano de oportunidades y riesgos estratégicos para la economía española, Elcano Royal Institute, Madrid.