Key messages

- Vaca Muerta already produces more than half of Argentina’s oil and natural gas, being the most important case of non-conventional hydrocarbon extraction using hydraulic fracturing and horizontal drilling (fracking) outside the US.

- The Vaca Muerta project challenges various myths exclusively linking the success of fracking to the US context. If the Argentine case could serve as a benchmark and fracking could spread internationally, it would have geopolitical, environmental and climate implications of the highest order.

- However, replicating the Argentine experience in other geographical settings faces major barriers linked to the political environment, the business structure and the social licence to operate, all of which tend to suggest that the Argentine case may be more of an exception than a benchmark.

Analysis

Vaca Muerta is now a reality and currently produces more than half of Argentina’s oil and natural gas, being the most prominent case of non-conventional hydrocarbon extraction using hydraulic fracturing and horizontal perforation (fracking)[1] outside the US. The future of Vaca Muerta is especially promising: it is predicted that, towards the end of the decade, it will enable Argentina to become a net exporter of oil and gas, with the potential to generate income of up to US$25.4 billion a year, a figure comparable to the amount generated by the country’s agricultural exports.

How has Argentina managed to replicate the US’s success in shale? To put it differently, what are the variables that account for Argentina’s success, in contrast to the failure of other countries that have previously tried fracking?

Understanding the Argentine case is important for two reasons. First, non-conventional reserves are a ‘frontier extractive industry’ with a significant potential for bolstering the security of supplies for producer countries, increasing access to energy in developing countries and changing the balances of power in the geopolitics of energy. Secondly, their extraction incurs major environmental and social risks. Shale[2] is often described as a ‘carbon bomb’ for two fundamental reasons: because of the volume of greenhouse gas emissions associated with the hydrocarbon deposits capable of being extracted through fracking; and because of the emissions, especially methane, that are created over the whole course of the production process. Moreover, in the absence of a proper regulatory framework, hydraulic fracturing also has a major environmental impact linked to the contamination of groundwater[3] and management of the waste generated by the activity.

This analysis starts by considering the factors that account for the success of Vaca Muerta in Argentina: propitious geology, a favourable political narrative, consistent regulatory support and, most importantly, the existence of a well-established social licence to operate. The paper concludes by considering the possibility of replicating the experience elsewhere, by means of three case studies in Colombia, Mexico and Algeria, where the debate around fracking is highly contentious and the hydrocarbon industry is similar to Argentina’s: century-old oil industries, but a decline in conventional output, concern about the security of supplies and proved reserves of non-conventional oil and gas.

From the exceptional nature of the US to the success of Vaca Muerta

The development of Vaca Muerta challenges various myths associated with the supposedly exceptional nature of the US, according to which it was practically impossible to replicate without its business ecosystem, a decentralised, liberalised and deregulated oil industry as well as political stability and, above all, a bedrock ownership regime in which a landowner is also the owner of the underground mineral resources.

The success of fracking in Argentina is particularly significant because it has succeeded in establishing a capital-intensive sector in an adverse macroeconomic environment, beset by recurring exchange-rate crises, high inflation, price controls and restrictions on the free movement of capital. Nor has the political environment been conducive to investment, especially following the 2012 nationalisation of the largest company operating in the sector, Repsol-YPF, and an alternating succession of governments from diametrically opposed wings of the political spectrum: Fernández de Kirchner, Macri, Fernández and now Milei. Moreover, while Argentina is a country with a long tradition of mining and to a lesser extent oil production, such activities have not been immune from vocal public opposition. For instance, the 2018 tendering process for offshore hydrocarbon exploration and production unleashed vociferous campaigns, known as the Atlanticazo, in various coastal cities.

Paradoxically, despite the fact that in other countries fracking is viewed as an extreme extractive technique that has generated intense opposition among environmentalists, opposition has been extremely muted in Argentina. This has helped the supporters of the oil industry, including the state-owned YPF, to secure the invariably difficult social licence to operate. As shown in Figure 1, the output of non-conventional oil and gas (shale andtight oil) has risen steadily in recent years, reversing the natural decline of conventional production. Forecasts for 2030, based on YPF projections, envisage in excess of a million barrels of crude oil a day and 7 billion cubic metres (bcm) of gas per month.

Figure 1. Output of oil and gas in Argentina, 2009-24

Geology matters, but is not sufficient

Although geological reserves of shale gas and oil are more evenly distributed than those of conventional hydrocarbons, the Argentine deposit located at Vaca Muerta is considered one of the best in the world both in quantitative and qualitative terms. Notable among its chief assets are its significant thickness (150-300 metres), optimal depth for non-conventional exploitation (2,500-3,500 metres) and a vast surface area of approximately 30,000 km², equivalent to the size of Belgium.

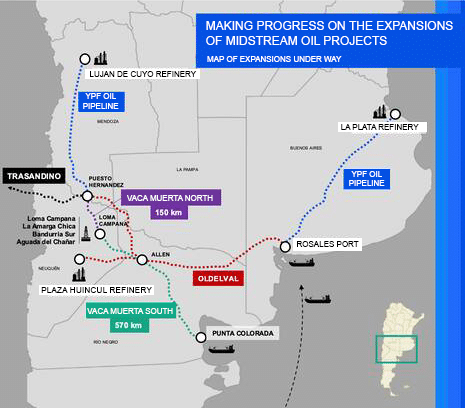

The conditions at the site are not perfect, however. Apart from anything else, Vaca Muerta is a logistical challenge. It is located in a relatively remote part of Neuquén province, a long way from the main clusters of energy consumption, devoid of a nearby port and with limited infrastructure for transporting hydrocarbons. The region’s arid climate hinders access to the water resources needed for hydraulic fracturing and its use of water puts it at odds with other consumers, such as irrigation for fruit growing.

Figure 2. Map of Vaca Muerta and the associated infrastructure under construction: gas and oil pipelines and ports

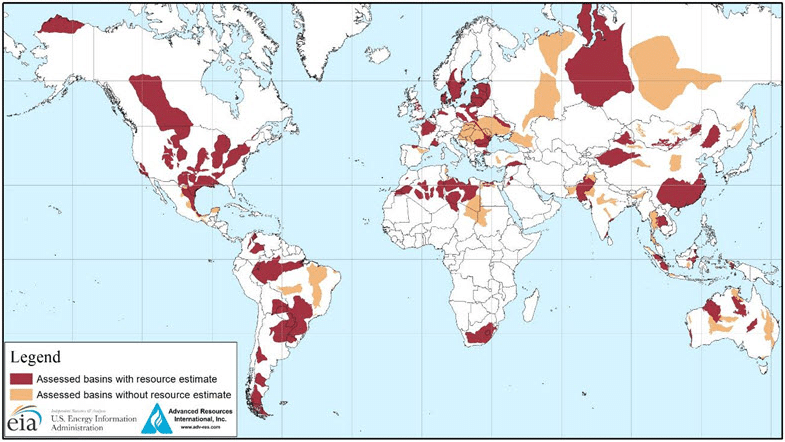

Although geology is a necessary condition for the exploitation of shale, it is not sufficient to guarantee success. The specialist literature is unanimous in viewing the above-ground risks –in other words, the risks related to the political, regulatory and economic context– as being much more decisive than the below-ground risks, related to the geological quality of the deposit. The variable that accounts for the success or failure of the shale thus resides more in the institutional, social and economic conditions than in the characteristics to be found underground. As shown in Figure 3, shalegas resources are relatively evenly distributed in geographical terms; the bulk of production, however, takes place in the US, Canada and, more recently, Argentina and China. One of the most instructive cases is the Eagle Ford basin, running from Texas to north-eastern Mexico, where it is known as the Cuenca de Burgos; whereas on the US side the basin produces non-conventional oil and gas using fracking, on the Mexican side of the border it remains virtually inactive.

Figure 3. Map of basins with the potential to produce shale oil and gas

The importance of narratives and the political discourse around shale

Around the time that Repsol-YPF announced the discovery of enormous oil and natural gas reserves at Loma La Lata, in Vaca Muerta, on 7 November 2011, Argentina was embroiled in an unprecedented energy crisis. The decline in output since 2004 (see Figure 4) had obliged the country to unilaterally suspend its exports to Chile, in breach of existing contracts. Halting supplies to its neighbour unleashed a diplomatic crisis and was a watershed moment in the energy integration of the Southern Cone. To satisfy the country’s energy needs, Argentina initially resorted to importing gas from Bolivia and later liquefied natural gas (LNG). The precariousness of supplies was such that, between 2004 and 2011, during the coldest winter months, Néstor Kirchner’s government was forced to prioritise household consumption of natural gas, rationing its use by industry and transport, thereby incurring major economic and political costs.

Repsol-YPF’s discovery of Vaca Muerta was presented as a transformative opportunity, described as a new ‘El Dorado’ for Argentina.[4] Given that Neuquén was already well-established as a hub for extracting conventional oil and gas, the national government and provincial authorities gave an enthusiastic welcome to Vaca Muerta as a means of restoring energy self-sufficiency, recovering waning tax revenues and reversing the deficit in Argentina’s energy balance of trade.

The discovery was made amid a context of pronounced regional nationalism related to natural resources. This was especially evident in Bolivia with the nationalisation of hydrocarbons in 2006 overseen by Evo Morales; that same year in Venezuela, with the renegotiation of oil contracts under the government of Hugo Chávez; and in Ecuador, with the reform of oil contracts in 2010 during Rafael Correa’s presidency.

Argentina joined this regional movement in 2012 with the approval of Law 26,741, which expropriated 51% of YPF SA and Repsol YPF Gas SA from the Spanish-Argentine multinational Repsol-YPF. Cristina Fernández de Kirchner’s government justified this measure by alleging a lack of investment and the prioritisation of foreign shareholders’ interests, particularly in the payment of dividends, to the detriment of the country’s energy needs. A majority of legislators (including the opposition parties)[5] voted in favour of the bill, which as well as the nationalisation sought to impose regulations on fracking. This chronology of discovery and subsequent nationalisation created an unusual political consensus in Argentina, a country that the Edelman Trust Barometer consistently classifies as one of the most politically polarised in the world.

An open and competitive oil market

Despite the nationalist rhetoric and renationalisation of 2012, YPF retained the operating structure of a private business, preserving its autonomy, its corporate governance arrangements and its stock exchange listing as a limited company. This independence enabled it to retain a good deal of its technical know-how and the corporate culture that had been nurtured under Repsol ownership, thereby avoiding the drift that regional counterparts such as PDVSA underwent. Cristina Fernández de Kirchner’s government, despite its political orientation, chose to maintain the involvement of private actors in Argentina’s energy sector, including the minority stakeholders in YPF.

Acknowledging the technical and financial challenges implicit in non-conventional extraction, the government encouraged partnerships between YPF and foreign oil companies. The relative openness of Argentina’s energy sector to foreign capital, in contrast to the wave of nationalisations and contract renegotiations that swept through other countries in the region, enabled the striking of key agreements, such as the one signed between YPF and Chevron.[6] This partnership constituted a milestone in the restoration of foreign investment in the sector just a few months after the expropriation of Repsol. It also triggered vociferous political opposition, however, not only because of the secrecy that shrouded its contents but also the fact that Chevron was embroiled in a lawsuit with Rafael Correa’s government in Ecuador, one of Argentina’s main regional allies at the time.[7]

YPF’s role as a state actor was accompanied by the presence of oil multinationals with capital and experience in US shale (Chevron, ExxonMobil, Shell and TotalEnergies), and by a flourishing ecosystem of Argentine companies (Vista, Pan American Energy, Pluspetrol and Tecpetrol) that started to operate in all stages of the upstream[8] process, demonstrating remarkable technical expertise.

This configuration of the oil sector gave rise to a market that soon started to replicate the decentralisation, dynamism and atomisation characteristic of US enterprise, where innovation and expertise are inducive to an ongoing process of learning about the geological resources. Such a type of ecosystem has a relatively low prevalence in oil-producing countries, which tend to exhibit rigid and highly centralised structures, whether revolving around a state enterprise that operates as a monopoly or by means of joint ventures with the state holding a majority stake.

Indeed, according to Rystad Energy, thanks to the positive features of the geological resource, access to cheap labour and the expertise acquired by Vaca Muerta operators, the average cost of production in Argentina is less than that of the main US shalebasins. The departure of major foreign investors, especially Total Energies and ExxonMobil since 2024, has given rise to an ‘Argentinification’ process of Vaca Muerta operators, proof of the expertise acquired by the local ecosystem and its emancipation from the US experience.

Constant and broad political consensus built on pragmatism

After the take-over of YPF in 2012, a range of measures were implemented to encourage the development of Vaca Muerta. These included Decree 929/2013, which offered incentives to major investors in non-conventional hydrocarbons, including fiscal stability for 15 years and, in the context of the so-called cepo cambiario, or foreign exchange clamp, unrestricted access to 20% of the currency obtained from exports related to the project. At the same time, minimum gas production prices were established at the wellhead, higher than those of the domestic market, with the aim of incentivising investment. YPF signed various key agreements with foreign companies, such as Chevron (in 2013), Petronas, Wintershall and Shell, which participated in various blocks by means of technical and financial partnership arrangements.

Under the presidency of Mauricio Macri (2015-19), and despite a more pro-market approach to energy affairs, the political support for Vaca Muerta remained constant. His administration retained the production subsidies, guaranteeing attractive prices at the wellhead, while gradually reducing those geared towards demand. During his term in office, gas exports to Chile were reinstated, more than a decade after supplies were suspended, and the tariffs levied on imports of the machinery required for oil production were substantially reduced.

The government of Alberto Fernández (2019-23) continued support for Vaca Muerta as a strategic cornerstone of the sector, albeit influenced by macroeconomic instability, exchange rate restrictions and fluctuations in the price of hydrocarbons on the international markets. Despite a more interventionist rhetoric, the executive preserved agreements with foreign companies and the public-private partnership approach. It also maintained the production stimulation programmes for natural gas and oil, such as the Plan Gas.Ar, which guaranteed producers minimum prices in exchange for investment commitments. Fernández inaugurated the first phase of the Néstor Kirchner gas pipeline,[9] a key project for increasing the ability to transport gas away from Vaca Muerta, and made progress on extending the Oldelval and Trasandino oil pipelines.

Lastly, Milei’s government (in office since 2023) enacted the Major Investments Incentive Regime (RIGI), which offers regulatory stability for 30 years, tax breaks, currency benefits and other stimuli to attract investments into infrastructure and energy. Moreover, it gives producers freedom to export provided that they first satisfy local demand, thereby opening up the Argentine oil industry to the international market after years of restrictions.

Under the auspices of the RIGI, work has started on building the Vaca Muerta South oil pipeline and the final investment decision has been taken to construct two floating liquefaction plants to export LNG from 2027. Under Milei’s presidency, and having abandoned its initial privatisation plans, YPF has set out its 2025-29 strategic plan with three key objectives: focusing investments on Vaca Muerta, becoming the largest shale producer in the world outside the US and leading the development of the infrastructure needed to export Argentina’s hydrocarbons.

At one of the moments of greatest political polarisation, support for Vaca Muerta has remained constant for more than 15 years and has rested on three pillars: private investment complemented by the state-owned YPF; production subsidies with wellhead prices above the domestic market price; and construction of infrastructure, including international interconnections, using public-private partnership schemes.

A social licence to operate based on local support

Unlike large-scale mining, which has faced vociferous resistance from civil society organisations, such as the Union of Citizen Assemblies, the extraction of hydrocarbons from Neuquén province, the epicentre of Vaca Muerta, has long enjoyed remarkable social legitimacy, having been part of the local economic fabric since the advent of the 20th century. One of the decisive factors in this widespread acceptance of shale has been the role played by YPF, which ever since it was founded has played a key part in the development of the territory, as a symbol of national pride, as an instrument of population settlement and in extending the state’s presence to particularly remote parts of Argentina.[10] The renationalisation of the company in 2012 coincided with the expansion of fracking and both processes were framed within a narrative of energy sovereignty and economic revival in the region.

The institutional framework has been decisive in the consolidation of this consensus. The 1994 constitutional reform granted the provinces ownership of below-ground resources, enabling them to make a direct claim on the royalties generated by production. Such fiscal decentralisation aligned provisional governments’ interests with fracking, given that the income emanating from oil and gas is essential to sustaining their budgets, funding public services and investing in infrastructure. The Short Law of 2006 expanded this autonomy even further by granting provinces powers to negotiate and extend exploration and operating contracts. Such an institutional configuration has created a clear incentive for provincial governments to operate as active promotors of Vaca Muerta, and they have even put pressure on the national executive to maintain policies that aid hydrocarbon production, sometimes turning a blind eye to environmental warnings and concerns regarding the cost-benefit ratio.

This decentralised model has also facilitated the building of the infrastructure needed to transport the Vaca Muerta output, construction of which is as socially sensitive as the production activity itself. The province of Río Negro, from where a large part of the crude oil produced in Neuquén will be exported once the Vaca Muerta South oil pipeline and the Punta Colorada terminal have been constructed, is a good case in point. In 1999 Río Negro passed a pioneering law that banned hydrocarbon-related activities in the Gulf of San Matías. In 2022, however, by an overwhelming majority the province approved a law that included exceptions for the development of infrastructure related to the transport and storage of hydrocarbons. The change of heart can be attributed mainly to an offer made by the consortium in charge of constructing the pipeline: more than US$1 billion by way of taxes and royalties over 13 years which will end up directly funding a province of 750,000 inhabitants.

Case studies: Mexico, Colombia and Algeria

Analysis of the cases of Mexico, Colombia and Algeria enables a deeper understanding of the variables that have made Argentina an international exception in the successful exploitation of non-conventional oil and gas resources. To address this question, it is first worth turning attention to Mexico, a country with a longstanding record of oil production and promising geological prospects, which approved an ambitious constitutional reform aimed at liberalising its energy sector and emulating, among other things, US success with fracking. Colombia illustrates the difficulties of making headway in shale development without obtaining a social licence to operate, despite having proved reserves, an approving political elite (until Petro was elected) and a technically competent business sector. Lastly, there is the case of Algeria, another longstanding producer of hydrocarbons, highly dependent on its energy-derived income and with vast reserves of non-conventional gas, extraction of which is viewed as a strategic necessity given the gradual depletion of its conventional reserves.

Mexico: energy policy reform but no social licence or political consensus

The development of fracking in Mexico was structured around the 2013 Energy Reform instigated by Peña Nieto’s government. This reform, which required a constitutional change, put an end to the PEMEX monopoly and opened the sector up to private investment, both domestic and foreign, in oil and gas exploration and production activities. One of the justifications of the reform was the need to revive a declining sector by dint of private capital in order to tap into, among others, the non-conventional resources that its northern neighbour was producing with such success. The development of shalein Mexico was justified on the grounds of energy security, amid growing dependency on US gas, as well as on fiscal grounds, given that PEMEX’s oil output was undergoing rapid decline due to its ageing wells, jeopardising its annual contribution to state coffers.

The 2013 Energy Reform put an end to almost a century of oil-centred nationalism and unleashed a vociferous social movement. In particular, the response to the government’s commitment to shale was the creation of the Mexican Anti-Fracking Alliance, a platform made up of more than 40 national and regional organisations. Over time, this coalition managed to transform fracking from a technical and peripheral issue into a symbol of environmental and political discontent with the unpopular Peña Nieto administration. Specifically, the Mexican Anti-Fracking Alliance managed to consolidate itself in those Mexican states where fracking had the greatest potential. Unlike in Argentina, where the provinces exercise control over their underground resources and stand to benefit directly from their extraction, the states and municipalities in Mexico barely receive any income from the production of hydrocarbons, given that it is the federal government that manages and redistributes oil income through fiscal transfers. This arrangement creates an imbalance in the distribution of costs and benefits: local communities are on the receiving end of environmental and social impacts, whereas the economic gains are funnelled into the federal level.

The election of Andrés Manuel López Obrador in 2018 represented a U-turn in energy policy and, aided by his majority in Congress, he reversed most of the energy reforms, including those aimed at attracting private investment and galvanising the energy sector. Although López Obrador had repeatedly expressed his support for fossil fuels, he took a firm stance against fracking, which he linked directly with his predecessor and attempts by private capital to undermine Mexico’s ‘energy sovereignty’. While López Obrador did not carry out his promise and never banned fracking, he did polarise public perception of the technique and paralyse its development.

The election of Claudia Sheinbaum heralded an unexpected shift in the policy on fracking. PEMEX avoids using the term ‘fracking’ in its 2025-2035 Strategic Plan, and replaces it with expressions such as ‘sites of complex geology’, ‘new extraction systems’ and ‘non-conventional plays’. It also includes references to the experiences of the US and Argentina, to the development of technologies aimed at reducing fresh water consumption and the need for private participation to offset financial risks. These elements hint at an eventual attempt to return to aspirations expressed during Enrique Peña Nieto’s term in office. The irony of López Obrador’s successor, an academic specialising in climate science, promulgating the revival of fracking has not gone unnoticed within the environmentalist movement, which has already announced its intention to oppose the measure.

Mexico’s case is paradigmatic for understanding the barriers to the development of fracking. It is not sufficient to have good geological prospects, nor a history of producing oil. Nor is it enough to adduce arguments regarding energy or fiscal security, or carry out the necessary reforms; it is fundamental to secure a widespread consensus that will enable resistance to its development to be overcome when political power changes hands.

Colombia: a well-prepared industry, but lacking political and legal consensus

Although Colombia is not normally classified as a petrostate, its economy significantly depends on the income derived from crude oil exports, which in 2023 accounted for 25% of the total. This is not counting the production of other fossil fuels such as coal and natural gas, the latter going mainly into domestic consumption. Unlike other Latin American countries, Colombia has not experienced any major waves of energy nationalism, owing to its limited reserves and its dependence on foreign investment. The Colombian approach has been pragmatic: attracting investment without renouncing national interests, which has led to it being classed as a ‘free-market rarity’ in the region.

Following the liberalisation of the sector in 2003, Colombia doubled its output thanks to competitive tendering processes, establishing itself as an attractive destination for investors, and Ecopetrol was heralded as one of the most efficient companies in the region. This growth ran its brief course amid the natural depletion of conventional reserves, which ended up threatening both oil-derived income and the security of natural gas supplies. Specifically, the forecast decline in gas output has been the cause of particular concern given that it functions as a back-up source on the occasion of the frequent droughts that affect the generation of hydro-electricity, responsible for more than 65% of the country’s electricity, and the high cost of resorting to LNG imports as an alternative. Amid the decline in conventional reserves and given the oil industry’s record of openness to foreign investment, as well as its acknowledged institutional pedigree, the development of fracking was seen as a promising option for sustaining output and safeguarding energy security.

In this context, in 2014 the government of Juan Manuel Santos (2010-18) published technical and environmental guidelines for regulating fracking after two years of consultations. Nonetheless, the social and academic opposition surrounding the Fracking-Free Colombia Alliance led to a moratorium imposed in 2018 by the Council of State, which suspended the commercial development of fracking as a precaution. As an alternative, Iván Duque’s administration (2018-22), despite promising not to pursue fracking in its campaign, set up Integrated Research Pilot Projects (PPII) to conduct a scientific study of its viability and awarded contracts to Ecopetrol and ExxonMobil in the Middle Magdalena Basin. Meanwhile, Ecopetrol invested US$1.5 billion in the Permian Basin in the US, with the goal of acquiring experience and transferring it to Colombia.

Amid pressure from civil society, however, in 2020 the Council of State announced the commercial suspension of fracking-related activities, although it allowed the pilot projects to continue under strict supervision. In that same year, Duque signed Decree 328, which established the regulatory framework for these pilot projects, but this was subject to fresh lawsuits owing to the lack of public participation and ambiguity with regard to how and by whom they were supposed to be executed. This delayed their implementation until, with Gustavo Petro elected to office in 2022, the government adopted an explicitly anti-fracking stance, which halted all fracking-related activities. In 2023, under the influence of its new Director General, Ecopetrol definitively abandoned its fracking plans in Colombia, and although it has decided to maintain its operations in the US (given that they account for more than 10% of the company’s crude output), it set out a new strategic plan focused on decarbonisation and the maintenance of the country’s conventional output. Meanwhile, the government tried unsuccessfully to promulgate Law 150 of 2024 with the goal of formally banning this technique. Somewhat surprisingly, support for fracking seems to have risen in recent years and has returned to the agenda for the 2026 presidential campaign. According to the Oil Barometer, support among Colombiansfor fracking in their municipality has doubled from a low point of 14% in 2019 to 28% in 2025.

Despite enjoying the political support of two consecutive governments under Santos and Duque, the backing of Ecopetrol and the interest of investors with experience in the industry, such as ExxonMobil, Colombia provides evidence of how civil society has succeeded in paralysing the development of fracking, including pilot projects, using judicial means. Energy security considerations, the existence of a well-established oil industry and political support have once again proved insufficient in the absence of an authentic social licence to operate.

Algeria: an oil industry in need of reform and a social licence that remains pending

Algeria is an oil and gas producer whose economy meets the classic definition of a petrostate: high dependency on revenue from hydrocarbon exports and the minimal diversification of its productive economy. Its energy policy has traditionally been characterised by a pronounced degree of oil nationalism that prioritises national sovereignty exercised through control of the state-owned Sonatrach company.

The rapid increase in domestic consumption of natural gas and oil, stimulated by generous consumer subsidies, together with the gradual depletion of the country’s main gas field, Hassi R’Mel, have reduced the forecasts for energy-derived income in the future. Aware that the stability of the regime to a large extent rests on the continuity of this income, the Algerian leadership saw its abundant reserves of shale gas (the third largest in the world) as a possible means of reviving hydrocarbon production. In 2013 the government embarked on an initial reform of the restrictive Algerian legal framework, introducing specific fiscal incentives for exploring non-conventional resources. This regulatory easing enabled the first shale gas well to be drilled in the Ahnet basin in 2014, although the initiative triggered a vocal public response, with unusual protests in Ain Salah, which spread to other regions. The fall in international oil prices shortly after the launch of the exploration campaign, combined with the regime’s caution regarding social discontent in the post-Arab Spring context, paralysed the development of fracking for almost a decade.

In order to overturn this situation, a new hydrocarbons law was enacted in 2019, a relatively ambitious reform that, while preserving Sonatrach’s majority stake, significantly reduced the fiscal burden on investors and established a more flexible contractual framework for non-conventional resources. Since then, interest in fracking has revived, with efforts to attract US companies such as Chevron and ExxonMobil, and promises being made for a specific tendering round for non-conventional resources.[11]

Despite the reform, Algeria continues to offer a relatively unattractive environment for foreign investment, characterised by a complex bureaucracy that hinders imports of equipment and the admission of technical personnel. The compulsory majority stake held by Sonatrach, which lacks experience of shale, impedes the operational agility required for this type of project. This is combined with a lack of legal certainty, characterised by an erratic and opaque energy policy, which prevents investors from anticipating the key decisions emanating from political power.

Moreover, the expected costs of producing from Algerian shaleare substantially higher than those of conventional oil and gas, which raises the need either to have an in-depth reform of the domestic energy pricing system or to implement a subsidy scheme on the price at the wellhead, as in the Argentine model. Both alternatives incur major political problems in the current context, characterised by latent social discontent and a dependency on subsidies as a means of lending legitimacy to the regime. Added to this is the risk of fresh protests in those parts of the south where the fracking is likely to take place, such as those that broke out in 2014, and the uncertainty surrounding the social licence to operate in the area.

In the case of Algeria, despite its hugely promising geology and firm support for the pursuit of fracking, the absence of a flourishing oil industry and doubts surrounding the social acceptance of fracking at the local level constitute enormous barriers to its successful development.

Conclusions

The success of Vaca Muerta makes it necessary to consider whether fracking could be generalised to other developing countries. If this were possible, it would have major geopolitical and climate implications. The map of hydrocarbon producers would be transformed, allowing countries to emulate, albeit on a smaller scale, what has taken place over the last 10 years with the US’s rise as a fossil fuel superpower. The emergence of new non-conventional hydrocarbon producers, whether Argentina, Colombia or Algeria, to name a few cases with enormous geological potential, would transform the balances of power among oil producers, to the detriment of the large traditional producers and the ability of the Organisation of Petroleum Exporting Countries plus (OPEC+) to set international prices.

From the climate-change perspective, the widespread use of fracking could substantially raise greenhouse gas emissions, since it is an extractive technique that involves considerable quantities of carbon dioxide and methane, the production of which could, as has occurred in the US, delay the uptake of renewable energies. Meanwhile the environmental impact of this technique is an important consideration, and without a proper regulatory framework wherever it is pursued its effects on groundwater and ecosystems could be irreversible.

However, as is evident from the Argentine case and the cases of Mexico, Algeria and Colombia, geological resources are a necessary condition to undertake fracking but not sufficient to enjoy its benefits. Argentina is striking as an exception among developing countries because it has managed to maintain a favourable narrative over time, significant political support across the political spectrum, an oil industry that is open to foreign investment and to consolidate its social licence to operate. It is not impossible to replicate the Argentine experience in other locations, but recent history suggests that the success of Vaca Muerta should be interpreted with caution, and more as an exception than as a benchmark.

[1] Hydraulic fracturing is a technique that involves breaking up bedrock with pressurised water to release gas or oil. Horizontal drilling enables a larger part of the oilfield to be reached by extending the well laterally underground. Both of these technologies have enabled fracking to be deployed in the US over the last 20 years.

[2] The terms ‘shale’ and ‘fracking’ are used interchangeably in this article to refer to the extraction of non-conventional hydrocarbons. ‘Fracking’ refers to the hydraulic fracturing technique used in their extraction, while ‘shale’ refers to the sedimentary rock that contains the resource. Non-conventional resources are generally those that cannot be extracted using traditional methods owing to their technical or geological characteristics.

[3] Groundwater refers to the water that accumulates naturally below the surface, forming underground layers or deposits that supply wells, springs and rivers.

[4] The characterisation of Vaca Muerta as Argentina’s ‘El Dorado’ appears in Maristella Svampa (2018), Chacra 51: regreso a la Patagonia en los tiempos del fracking.

[5] Law 26,741 was approved in the Chamber of Deputies on 3 May 2012 by 208 votes in favour to 32 against.

[6] One of the great paradoxes of the Vaca Muerta operation is that only a few months after the nationalisation of Repsol-YPF there was a major influx of foreign investors. This may be attributable to a perception of reduced risk of expropriation among shale sector investors as argued by G. Collins, M.P. Jones, J. Krane, K. Medlock & F. Monaldi (2021), ‘Shale renders the “obsolescing bargain” obsolete: political risk and foreign investment in Argentina’sVaca Muerta’, Resources Policy, nr 74, 102269.

[7] In 2011 an Ecuadorean court sentenced Chevron to pay US$9.5 billion for environmental damage to Amazonia, leading to a failed attempt to sequester the assets of its Argentine subsidiary in 2013.

[8] ‘Upstream’ in the energy industry refers to the initial phase in the oil and gas production chain, which includes the exploration, drilling and extraction of the underground resources before they are transported and refined.

[9] The Milei government decided to change its name to the Perito Francisco Pascasio Moreno gas pipeline in 2024.

[10] For the legitimacy of YPF in Patagonia, see H.M. Palermo & A.M. García (2007), ‘El rol del Estado en la construcción de sentidos. El caso YPF’, Theomai, nr 16, p. 7-15.

[11] For an in-depth study of the Algerian case, regarding both its conventional and non-conventional resources, see G. Escribano (2025), ‘Otra ronda de gas argelino para Europa’, ARI, nr 37/2025, Elcano Royal Institute.