Theme: This ARI examines the impact of the global financial crisis on the Brazilian economy and the ways in which the country has managed to react positively to the ensuing challenges, without overlooking the new challenges that it will have to face in the future.

Summary: The global balance indicates that Brazil has managed to weather the international financial crisis reasonably well, despite having been severely hit initially. Brazil felt the financial crisis most strongly at the end of 2008 and industry was particularly affected. Yet the situation began to improve in the second quarter of 2009. When it comes to the whys and wherefores, the strong institutional framework and a cautious monetary policy have been key to managing the crisis, which has led to inflation being kept under control and on a downward trend.

Analysis: Brazil has managed to weather the international financial crisis reasonably well, despite having been severely hit initially. In fact, its GDP fell by 2.9% in the last quarter of 2008 and by 0.9% in the first quarter of 2009. From then onwards, the economy returned to growth. This is better than in the developed countries and much better than in countries such as Russia and Mexico (see Table 1). Even so, there are some questions marks about the sustainability of long-term growth. This could mean that Mexico achieves higher growth than Brazil in 2010, which would be a surprise.

Table 1. GDP growth (quarter-on-quarter variation, with seasonal adjustment)

(%) | Brazil | US | Europe | Mexico | Russia |

| 1Q08 | 1.80 | -0.20 | 0.80 | 1.06 | 1.90 |

| 2Q08 | 1.00 | 0.40 | -0.20 | -0.36 | 0.80 |

| 3Q08 | 1.10 | -0.70 | -0.40 | 0.05 | 0.20 |

| 4Q08 | -2.90 | -1.40 | -1.90 | -2.42 | -1.80 |

| 1Q09 | -0.90 | -1.60 | -2.40 | -6.45 | -9.00 |

| 2Q09 | 1.10 | -0.30 | -0.20 | -0.27 | -0.20 |

Source: OECD.

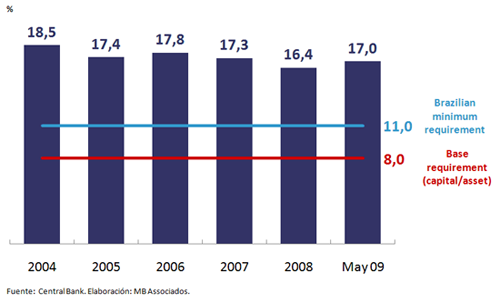

This may partly be explained by the economic conditions existing at the start of the crisis. In 2006 Brazil had just entered into a more vigorous growth cycle. There were idle capacity and financially-sound companies in many sectors. Consumer debt was low and, in general, consumer liabilities were short term. Unlike the case of Europe and the US, the home mortgage debt was very low. In fact, property loans only accounted for 2.3% of the GDP in December 2008. At the same time, the Central Bank of Brazil had implemented strong prudential regulation since the banking crisis in the 1990s. The minimum leverage requirement of the banks is still 11%, higher than the 8% ratio usually recommended by the Basel agreements. However, even greater caution was applied, as a 16% capital/asset ratio was the effective position of the banking system (see Graph 1).

Graph 1. Capital/asset ratio of the 50 largest Brazil banks (%)

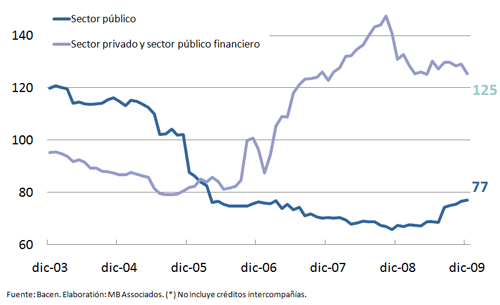

The country had recently obtained an investment grade, which consolidated the capital inflow and foreign exchange reserves, reaching US$197 billion in October 2008. Foreign debt continued to fall, standing at US$214 billion by the end of 2008. Public debt was down to just US$67 billion and the National Treasury, after many decades, was no longer a foreign debtor and had become a creditor (see Graph 2).

Graph 2. Evolution of foreign debt (US$ billion)

Therefore, the devaluation of the Brazilian real would not lead, as was later seen, to any type of fiscal pressure on the government. On the contrary, the resulting foreign exchange gains led to a reduction of the debt initially.

Brazil felt the financial crisis most strongly at the end of 2008 and industry was particularly affected as it was hit in three ways. First of all, exports of manufactured goods fell significantly during the last quarter of that year, by approximately 37%. The greatest problem that the Brazilian exporter faced was a sharp drop in sales to emerging countries, ie, the main customers of its industrial sector that mainly specialised in medium-technology products. For example, Argentina and Mexico were the best markets in terms of national car sales. In fact, this market shrinkage for Brazilian products has continued to the present to a great extent. Secondly, in addition to the shrinkage, as in the rest of the world, US$ funding for exports was severely hit. We are currently in the first credit crunch of modern history. The credit squeeze likewise affected domestic market operations. During the months leading up to the crisis, many companies had obtained credit through operations in Brazilian reals, but using exchange rate derivatives. As the Brazilian real was devalued by more than 30% over the last months of 2008, these companies were badly hit and many went into bankruptcy. As in other markets and countries, the majority of companies had not imagined the extent of the risk involved in the use of derivatives. Hence, the drop in exports and the credit squeeze meant that companies had to cut back their operations and implement a particularly aggressive policy to reduce stocks, even at the cost of financial losses. In many cases, particularly when it came to raw materials such as fertilisers, purchases made prior to the downturn arrived in Brazil when the prices had already fallen significantly. In those cases, the liquidation of stock resulted in huge losses. Due to the very negative cash flow position, many companies slashed their production levels and cancelled or postponed investment projects. The orders for capital goods shrunk sharply, resulting in a 21% drop in industrial production between October and December 2008, which only began to recover some months later. In order to assess the extent of the downturn, it is noteworthy that, even though the Brazilian economy overall began to recover in the second quarter of 2009, the forecast for industry remained negative for the year as a whole and its performance was estimated to be -7.7%.

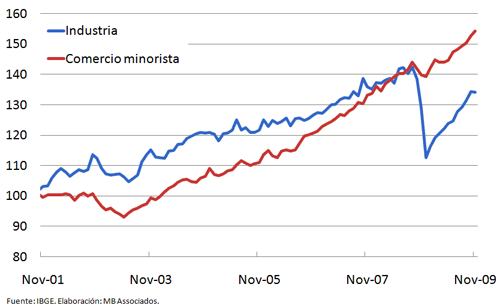

Nonetheless, in other sectors of the economy, particularly in the service sector, the situation was very different from the start, mainly as a result of the strong expansion of public expenditure, particularly in terms of paying employees. Throughout the year, the increased number of civil servants and rise in the real salary in the public sector was already injecting purchasing power into the system. The minimum salary increasing over the inflation rate and the rise in social security and social welfare spending, such as the so-called Bolsa Familia (Family Allowance), were likewise significant. Therefore, wages overall were maintained and the performance of the retail trade sector remained steady. Despite the crisis, the real personal income overall grew by 2.2% between October 2008 and January 2009. Retail trade continued its positive trend and ended the year with an estimated growth of 5.6% (see Graph 3).

Graph 3. Retail Trade and Industry Production Index (base: January 2000 = 100)

Other activities, such as telecommunications and the real estate and financial sectors, also performed well as the result of increased personal spending.

This trend was consolidated by different fiscal and monetary measures. The Central Bank of Brazil quickly provided smaller banks with a strong liquidity cushion. This put them in a stronger position and they could adjust their portfolio without any banks failing. Commercial lines of credit in US dollars were simultaneously set up, using foreign reserves, in order to provide liquidity for exporters. The Banco do Brasil played a key role in the operation. In fact, the main public banks (Banco do Brasil, Caixa Econômica Federal and Banco Nacional de Desenvolvimento Econômico e Social) expanded their loan portfolios dramatically. Only the future will tell if the quality of this portfolio has remained high or if the number of defaulters will increase. Finally, interest began to be reduced more systematically and the year ended down by 500 points, which obviously helped to turn credit around.

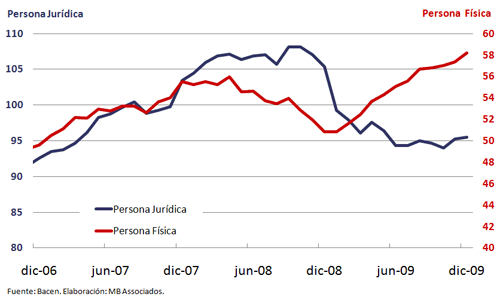

The Treasury also reacted by speeding up revenue expenditure and it did so in two ways: (1) by again increasing the public sector payroll; and (2) by increasing social security spending and transfers to the private sector. We estimate, for example, that the total payroll of the public sector for 2009 was up by more than R$17 billion, which represents nearly 40% of the estimated growth for total personal income in Brazil. Thanks to the higher salaries, civil servants and pensioners were granted loans that they spent on purchasing goods to the tune of nearly R$22 billion. At the same time, taxes were lowered for a series of products, the lowering of the car tax being the most significant. In fact, this sector became a special case as its sales recovered dramatically. At the end of 2009, the sales of cars and vans stood at 3,207,000 units, up 11.9% over 2008. The domestic market performed so strongly that it offset the huge drop in vehicle exports, which was even so 473,000 units (-36%) in 2009. Based on the tax stimulus, the banks, particularly those in the private sector, began to grant consumer loans again, which laid the foundations for a sharp upturn in the demand for consumer durables. The total credit to consumers ended 2009 with higher levels than during the period leading up to the crisis. The great willingness of people to ask for consumer credit contrasts dramatically with the difficulties faced in Europe and America to raise the lending level, even after the whole liquidity stimulus process backed by the European Central Bank and by the FED (see Graph 4).

Graphe 4. Credit granted to individuals and companies (three-month moving average; data not seasonally adjusted in R$ billions)

The Brazilian economy began to improve in the second quarter of 2009. One of the most important factors was the perception that inflation, the eternal enemy during recessions, would continue to fall. The soundness of the institutions and the cautious monetary policy was consolidated by the revaluation of the Brazilian real. The system thus began to accept the idea that the cost of living would remain within the 4.5% target, which in fact occurred, as the final numbers showed that the IPCA (Official Consumer Price Index) increased by 4.3%. It is perhaps useful to remember that in Brazil, unlike Argentina, the official price indexes are perceived to be totally credible and are always compared with indexes calculated by non-governmental institutions, such as the Universidade de São Paulo and the Fundação Getulio Vargas. Naturally, keeping inflation low strengthened the desire to obtain more credit, which accelerated throughout the year.

Parallel to consumer demand, Brazilian exports began to enjoy a positive knock-on effect from the strong recovery of the Chinese economy. After its GDP growth fell to 6% at the beginning of the year, the economy of the Asian giant, stimulated by its spectacular investment package, grew from 7.9% to 8.95% in the second and third quarter, respectively. Therefore, the exports of commodities recovered. In 2009 China became the largest trade partner of Brazil and was the destination for 13% of national exports. At the same time, US participation fell to approximately 10% and was in second place.

Many analysts regretted that industrial exports did not follow the growth rate of commodities exports and claimed it was due to the low technological component in the natural resources chains. However, two points should be made: first of all, the technological component in the agribusiness and offshore oil chains is much greater than commonly believed. For a major international consultant, bio-technology and offshore oil are two of the four areas of currently greatest technological progress (along with IT and aeronautics/astronautics). Secondly, one of the advantages of being a global trader, as is Brazil, is to be able to use the fact that there is always a type of client with expanding markets. The commercial policy is that it must be dynamic, always looking to open new markets and fighting against protectionism.

Apart from the consumer sector and commodities exports, the housing market also recovered quickly from the second quarter onwards. As shown in Graph 5, there was an upturn in the construction of new buildings in São Paulo (which also occurred in the rest of the country). Demand rose very strongly as the loans to the sector were up by approximately 40% in 2009.

Graph 5. Construction of new buildings in São Paulo (units)

After two quarters with a downturn, growth began to recover in the second quarter of 2009 and has continued ever since. Nonetheless, GDP for the year as a whole should have remained stagnant, based on our forecast of -0.1%. However, strong growth of around 6% is forecast for 2010, which will consolidate recovery.

The country has come out of the crisis relatively quickly and has been rewarded for this. The country risk, measured by the CDS, is just over 100 points. The São Paulo Stock Exchange index is the one with the greatest increase in value, in US dollars, among emerging countries. The Stock Exchange itself, which is a public company, is worth over US$15 billion, the third largest in value worldwide, just behind Chicago and Hong Kong. The launch of Banco Santander (Brazil) shares was the most important in the emerging world in 2009.

In the short term, special mention should be made of the increase of the nominal public deficit to approximately 4.5% in November 2009 from under 2% in December 2008. On the other hand, gross public debt (without discounting foreign reserves) rose from 53% in 2007 to nearly 65%. These are not particularly high figures compared to the developed world.

In the medium term, the cost will be relatively heavy. The extraordinary rise in the cost of public employment (a policy that could never be considered to be Keynesian) has led to a lack of flexibility for public accounts and, to a certain extent, ensures that federal investment should continue to be around a ridiculous 2% of GDP, for a country where tax revenue is 36% of GDP. At the same time, the Social Security deficit (both for the private and public sectors) increased dramatically. There is an obvious intertemporal inconsistency on this point which will have to be resolved in the future.

Conclusion: In short, after two quarters on a downward trend, the Brazilian economy bottomed out in the second quarter of 2009 and returned to growth. The country has come out of the crisis relatively quickly and has been rewarded for this. There are still two important questions left unanswered: what is the cost of the stimulus and support programmes? And will the return to growth be sustainable?

Even though the answer is not simple, we believe the costs have been relatively modest in the short-term, but quite significant in the medium term. Ideological and electoral reasons (the desire to expand the role of the State in the economy) are responsible to a great extent for the decisions taken. The Brazilian economy has recently become less competitive, as a result of the poor quality of education, the worsening of the ports and transport infrastructure, high taxes, high electricity prices, etc. Furthermore, we still have to see how the international markets and the domestic economy react to the 2% tax on the inflow of speculative capital that the government introduced in October to prevent the Brazilian real appreciating and a bubble being created.

The uncertainties that still exist regarding the pattern of recovery of the world economy and the costs mentioned above suggest that, unfortunately, the sustainability of Brazilian growth at high rates is still not guaranteed. Even so, Brazil has shown that it is, along with China and India, in the group of countries that has best weathered the economic crisis. Moreover, from the international point of view, its influence has continued to grow during the crisis, as can be seen from its active role in the G-20 and its budding regional leadership.

José Roberto Mendonça de Barros

Economist and partner of MB Associados, São Paulo, Brazil